UNOFFICIAL TRANSLATION

The Grand Ducal Regulation of 25 October 20241 has implemented into domestic law Commission Delegated Directive (EU) 2023/2775 of 17 October 20232 increasing the size criteria in relation with the categorisation of undertakings and groups.

As a reminder, this increase in the thresholds relating to total balance sheet and net turnover follows the high inflation experienced in 2021 and 2022 and, more generally, inflation over the period between 2013 (date of adoption of accounting directive 2013/34/EU) and 2023 (date of the first increase in the thresholds, 10 years after the adoption of the accounting directive).

This significant increase in thresholds – of about 25% – should result in the recategorisation of certain large undertakings as medium-sized undertakings, which will then be exempt from the obligation to publish sustainability information under Directive (EU) 2022/24643, known as the “CSRD”. Similarly, the increase in thresholds should lead to the re-categorisation of certain medium-sized undertakings as small undertakings, which will then be exempt from the obligation to have their annual accounts audited by a “Réviseur d’entreprise agréé” (approved statutory auditor) and from the obligation to prepare a management report. Similarly, some small undertakings will be re-categorised as micro-undertakings4 (exempt from preparing notes to the annual accounts) and some large groups will be recategorised as small groups (exempt from preparing and publishing consolidated accounts). This increase of the thresholds relating to size criteria (total balance sheet and net turnover) therefore constitutes measures aimed at reducing the administrative burden on undertakings and groups.

It should be noted that the new thresholds relating to size criteria introduced by Delegated Directive (EU) 2023/2775 are binding on Member States, which have options only on the following points:

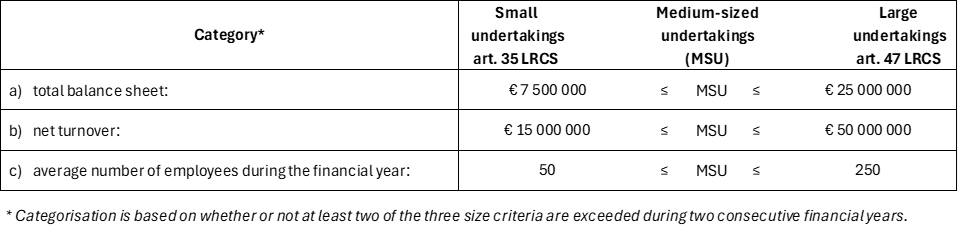

In this regard, it should be noted that Luxembourg has opted to raise the thresholds for small undertakings to their maximum levels, i.e. €7.5 million for total balance sheet and €15 million for net turnover. Similarly, Luxembourg has exercised the option to anticipate the first application of the new thresholds to financial years beginning on or after 1 January 2023.

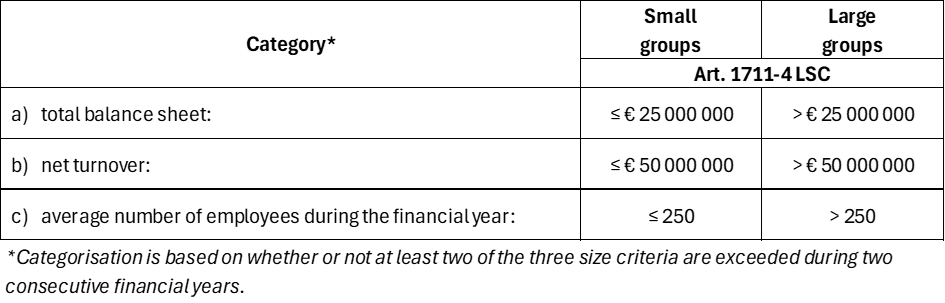

Thus, following the implementation of Delegated Directive (EU) 2023/2775, the thresholds referred to in Articles 35 and 47 LRCS (see: Fig. A) and Article 1711-4 LSC (see: Fig. B) are now as follows:

Fig. B

Considering that the system for categorising undertakings and groups is based on whether or not they exceed at least two of the three size criteria (total balance sheet, net turnover and average number of employees), and on a repetition criterion whereby exceeding or not exceeding the thresholds only takes effect when it occurs in two consecutive financial years, the question arises as to how this increase in thresholds will apply in practice and when any re-categorisation of undertakings and groups will take effect.

What are the practical arrangements for applying the new thresholds and when will the re-categorisation of undertakings and groups take effect?

CNC notes that raising the thresholds will not, in principle, have an immediate effect on the categorisation of undertakings and groups, but rather a delayed effect due to the repetition criterion, which requires that, in order to take effect, the thresholds must be exceeded or not exceeded during two consecutive financial years. Article 36 paragraph 1 LRCS thus provides that “[w]here on the balance sheet date an undertaking exceeds or ceases to exceed the limits of two of the three criteria indicated in Article 35, that fact affect the application of the derogation provided for in that Article only if it occurs in two consecutive financial years”.

In this regard, CNC points out that, in its Q&A CNC 19/0195, an interpretation of Article 36 LRCS is proposed according to which exceeding or not exceeding at least two of the three size criteria for two consecutive financial years takes effect during the financial year following that in which the exceeding or non-exceeding occurred for the second time. In other words, an undertaking that ceases to exceed at least two of the three size criteria relating to a higher category during financial years N-2 and N-1 is only re-categorised in a lower category undertaking from financial year N onwards.

Therefore, and taking into account the fact that Article 3 of the Grand-Ducal Regulation of 25 October 2024 provides for the application of the new thresholds to financial years beginning on or after 1 January 2023, it is in principle only during the 2025 financial year – after at least two of the three thresholds (as adjusted) have ceased to be exceeded for two consecutive financial years (financial years 2023 and 2024) – that not exceeding the said thresholds will result in the re-categorisation of the undertaking or group from a higher category to a lower category (see example 1).

However, there will be an exception to this principle of taking effect in the 2025 financial year in the case of newly created undertakings or groups (see example 2). In addition, other exceptions to the principle of taking effect in 2025 may also be considered (see example 3).

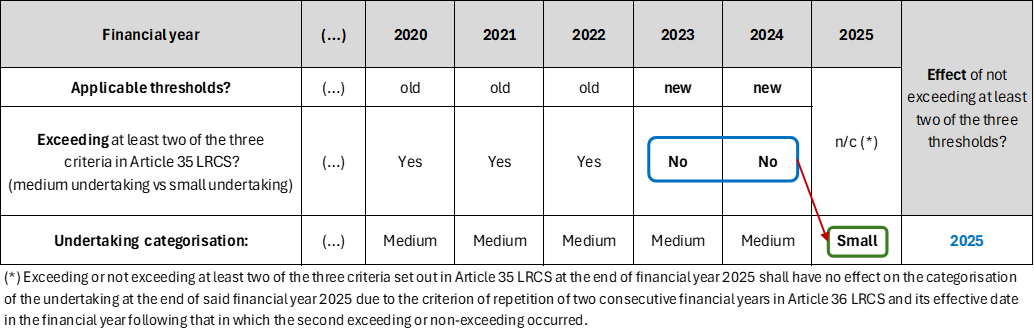

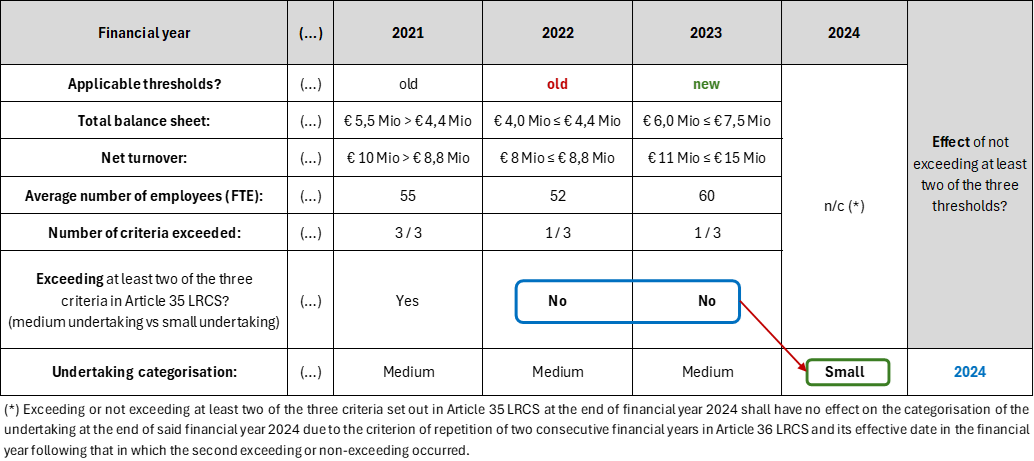

By way of illustration, let us take the situation of an undertaking which, during financial year 2022, was categorised as a “medium-sized undertaking”, with a balance sheet total of €10 million, a net turnover of €13 million and an average number of employees of 25, i.e. a situation in which two of the three (former) size criteria referred to in Article 35 LRCS were exceeded (total balance sheet > €4.4 million and net turnover > €8.8 million) and this, hypothetically, for several financial years (e.g. financial years 2020 and 2021 determining the categorisation for financial year 2022).

In the simplified assumption of a perfect stability of the financial data and employee headcount of the undertaking during financial years 2023 and 2024, the increase in thresholds introduced by the Grand-Ducal Regulation of 25 October 2024 would mean that at least two of the three (new) size criteria would no longer be exceeded during those financial years (net turnover ≤ €15 million and average number of employees ≤ 50). As this double non-exceeding (2023 and 2024) only takes effect during the financial year following that in which, for the second time, at least two of the three criteria have not been exceeded (2024), it is during financial year 2025 that the undertaking would thus be re-categorised as a “small undertaking” (see: Fig. C).

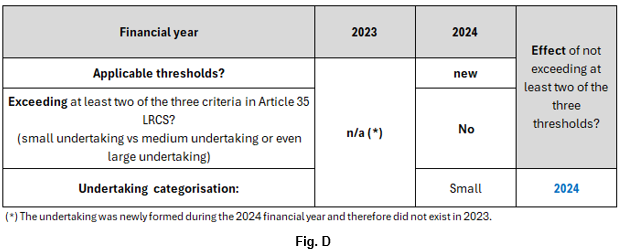

In contrast to example 1, which deals with an existing undertaking, example 2 deals with an undertaking newly formed in 2024 and which therefore has no “history” of exceeding or not exceeding the thresholds for two consecutive financial years.

In such cases, the aforementioned Q&A CNC 19/019 states that it is then up to the undertaking’s governing bodies to make a good faith estimate7 to determine whether or not the undertaking will exceed at least two of the three size criteria at the end of its first financial year. If, on the basis of a good faith estimate, it is not expected that the undertaking will exceed the thresholds (as adjusted by the Grand-Ducal Regulation of 25 October 2024) for at least two of the three size criteria referred to in Article 35 LRCS at the end of its first financial year, it would then be categorised as a “small undertaking” from financial year 2024 onwards (see: Fig. D). Otherwise, the undertaking would obviously be categorised as a “medium-sized undertaking” or even as a “large undertaking”.

It should be noted that if the first financial year of the newly formed undertaking is a shortened financial year (< 12 months) or a long financial year (> 12 months), its net turnover must then be annualised8.

As in example 1, example 3 deals with the situation of a pre-existing undertaking, which has been categorised as a “medium-sized undertaking” for several financial years.

If such an undertaking were to cease – for the first time at the end of financial year 2022 – to exceed at least two of the three “old” thresholds set out in Article 35 LRCS and were to cease – for the second (consecutive) time at the end of financial year 2023 – to exceed at least two of the three “new” thresholds set out in Article 35 LRCS, it would be re-categorised as a “small undertaking” from financial year 2024 onwards (see Fig. E).

It should be noted that such a scenario may seem somewhat theoretical to the extent that it assumes an increase in total balance sheet and/or net turnover between financial year 2022 and financial year 2023, but that – following this increase – the resulting amounts are higher than the “old” thresholds but lower than the “new” thresholds provided for by the Grand-Ducal Regulation of 25 October 2024.

In conclusion, it should be noted that there are other possible situations, similar to the one described in example 3, which would result in the re-categorisation of the undertaking from a higher category to a lower category as of financial year 2024, i.e. one year earlier (financial year 2025) than the standard situation referred to in example 1 above. However, in order not to unduly complicate the content of this Q&A, these hybrid situations will not be presented here.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Q&A CNC 24/034 Rehaussement des critères de taille des articles 35 et 47 LRCS ainsi que de l’article 1711-4 LSC : modalités d’application pratique”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible in accordance with general law for any decisions taken based on this document.

1 Grand-Ducal Regulation of 25 October 2024 amending:

1° Article 1711-4 of the amended Law of 10 August 1915 on commercial companies;

2° Articles 35 and 47 of the amended Law of 19 December 2002 on the trade and companies register, as well as on the bookkeeping and annual accounts of undertakings, with a view to transposing Delegated Directive (EU) 2023/2775 of the Commission of 17 October 2023 amending Directive 2013/34/EU of the European Parliament and of the Council as regards the adjustment of size criteria for micro, small, medium-sized and large undertakings or groups

2 Commission Delegated Directive (EU) 2023/2775 of 17 October 2023 amending Directive 2013/34/EU of the European Parliament and of the Council as regards the adjustment of size criteria for micro, small, medium-sized and large undertakings or for groups

3 Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014 and Directives 2004/109/EC, 2006/43/EC and 2013/34/EU as regards corporate sustainability reporting

4 It should be noted that, for the time being, the category of micro-undertakings has not yet been introduced into Luxembourg accounting law. However, draft bill of law No. 8286 on bookkeeping, annual financial statements and consolidated financial statements of undertakings and related reports, repealing the function of “commissaire” (supervisory auditor), proposes to introduce this category of micro-undertakings into Luxembourg accounting law.

5 Q&A CNC 19/019 entitled “Categorisation of undertakings: interpretation of the repetition criterion referred to in Article 36 LRCS”.”

6 In theory, it could be stated that the situation referred to in example 2 could also apply to an undertaking formed in 2023, as the Grand-Ducal Regulation of 25 October 2024 applies to financial years beginning on or after 1st January 2023.

However, considering that the annual accounts for financial year 2023 (calendar year) had to be filed by 31 July 2024 at the latest and that the Grand-Ducal Regulation of 25 October 2024 had not yet been adopted and published on that date, the case of an undertaking incorporated during 2023 has not been presented in this Q&A, as this would imply that the annual accounts for financial year 2023 have been filed after the legal deadline, in breach of Luxembourg accounting law. It should be noted that the situation may be different for undertakings with a non-calendar financial year.

7 It should be noted that the draft bill of law No. 8286/00 incorporates CNC’s interpretation of the principle of good faith estimate for the purposes of determining the classification of an undertaking or group at the end of its first financial year, in Articles 310-2, paragraph 6, second sub-paragraph (annual financial statements) and 410-2, paragraph 5, second sub-paragraph (consolidated financial statements).

8 Article 310-2, paragraph 6, sub-paragraph 3 of draft law no. 8286/00 provides that:

” Where the financial year is exceptionally shorter or longer than twelve months, the net turnover realised by the undertaking required to prepare annual financial statements shall be annualised. For this purpose, the net turnover realised by the undertaking required to prepare annual financial statements shall be multiplied by a fraction whose numerator is twelve and whose denominator is the number of months in the financial year in question, with any month that has begun being counted as a full month”.