UNOFFICIAL TRANSLATION

The law of 18 December 20151 transposing Directive 2013/34/EU2 – applicable to financial years beginning on or after 1stJanuary 2016 – amended article 48 of the law of 19 December 20023 (art. 48 LRCS) relating to the definition of turnover.

What are the practical implications of the changes to the definition of turnover for Luxembourg undertakings subject to general accounting law?

It is proposed to answer this question by first reminding the origin of the modification of the definition of turnover (point 1.), then by explaining the reasons which led to this modification (point 2.) and finally by identifying its practical implications for Luxembourg undertakings (point 3.).

The change in the definition of turnover in Luxembourg stems from the move to coordinate Luxembourg accounting law with the European accounting directive 2013/34/EU, which repealed and replaced the 4th Directive 78/660/EEC.

Thus, Article 48 LRCS – prior to the amendments introduced by the Law of 18 December 2015 – mirrored the definition of turnover referred to in Article 28 of the former 4thDirective 78/660/EEC4. Now and following the amendments introduced by the Law of 18 December 2015, Article 48 LRCS mirrors the definition of turnover as referred to in Article 2 point 5) of the Accounting Directive 2013/34/EU (see: Fig. (a) below).

In substance, the main change to the notion of turnover consists of the removal of the reference to income “falling within the undertaking’s ordinary activities“.

In other words, whereas turnover as defined by the 4th Directive 78/660/EEC only covered the sales of products and the provision of services corresponding to the undertaking’s ordinary activities, turnover – now defined by the accounting directive 2013/34/EU – is no longer limited to the said ordinary activities.

The removal by the European legislator of this reference to income from ordinary activities must be seen in the context of the suppression of the category of extraordinary income and charges, a removal guided essentially by a desire to modernise the accounting directive as well as a concern to align with international accounting practice (e.g. IFRS, US GAAP) which does not recognise or no longer recognises this category.

Prior to its repeal, Article 29 para. 1 of the 4th Directive 78/660/EEC provided that “[i]ncome and charges that arise otherwise than in the course of the company’s ordinary activities must be shown under ‘Extraordinary income and Extraordinary charges’“. To this end, the profit and loss account layouts included captions dedicated to extraordinary income and extraordinary charges. The provisions of article 29 para. 1 were incorporated into Luxembourg accounting law in article 49 (1) LRCS and the profit and loss account layout provided for in article 46 LRCS included – just like the directive – captions for extraordinary income and extraordinary charges.

The direct consequence of Directive 2013/34/EU’s suppression of the category of extraordinary income and charges is that “income and charges that arise otherwise than in the course of ordinary activities” (art. 29 para. 1 dir. 78/660/EEC and art. 49 (1) LRCS) can no longer be presented in the profit and loss account separately from the income or charges “falling within (…) ordinary activities” (art. 28 dir. 78/660/EEC and art. 48 LRCS) of the undertaking.

In this context, the reference to the undertaking’s ordinary activities has therefore been removed from the notion of turnover.

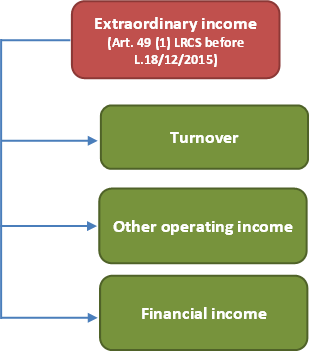

The elimination of the category of extraordinary income and its direct consequence, the removal of the reference to income “falling within (…) ordinary activities” within the definition of the notion of turnover, has a “communicating vessels effect”. In other words, income from sales and services not falling within the undertaking’s ordinary activities (e.g. income from discontinued operations, income from operations in process of being sold) which – prior to the entry into force of the Law of 18 December 2015 – were shown under “extraordinary income” would now be presented under “turnover”.

Income previously presented in the extraordinary income category would also – and in some cases should also – be presented under captions other than “turnover”.

By way of illustration, Q&A CNC 16/0085 suggests that proceeds from the disposal of fixed tangible assets may be assigned to caption “4. Other operating income” and that proceeds from the disposal of certain financial fixed assets, including – for example – shares in affiliated undertakings be assigned to the caption “9. Income from investments”.

In other words, changes introduced by the law of 18 December 2015 in no way imply an automatic transfer of “extraordinary income” to “turnover”, as the undertaking must determine which of the potential allocations is the most appropriate with regards to the objective of true and fair view (see: Fig. (b) below).

It is also noted that the change in the definition of turnover has no impact on the dividing lines that existed – prior to the entry into force of the Law of 18 December 2015 – with the concepts of “other operating income” and “financial income”.

In summary, the change in the definition of turnover (art. 48 LRCS) in Luxembourg accounting law is the result of the modernisation carried out at European level (Directive 2013/34/EU), which has had the effect of:

and

These eliminations mean that undertakings must now present income arising otherwise than in the course of ordinary activities within one of the other existing captions of the profit and loss account, for example within “turnover”, “other operating income” or “financial income”.

For Luxembourg undertakings, this change in the definition of turnover does not imply an automatic repatriation to turnover. Moreover, the change in the definition of turnover has no impact on the dividing lines that existed – prior to the entry into force of the law of 18 December 2015 – with the notions of “other operating income” and “financial income”.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Notion de chiffre d’affaires (art. 48 LRCS) : incidence des modifications introduites par la loi du 18 décembre 2015 ”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible under ordinary law for any decision taken on the basis of this document.

1 Law of 18 December, 2015 amending, with a view to the transposition of Directive 2013/34/EU of the European Parliament and of the Council of 26th June, 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC: 1) the amended law of 10 August 1915 on commercial companies; 2) Title II of the amended law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings; 3) Title II of Book I of the Commercial Code.

2 Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC.

3 Law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings, as amended.

4 Fourth Council Directive of 25 July 1978 based on Article 54 (3) (g) of the Treaty on the annual accounts of certain types of companies (78/660/EEC).

5 Q&A CNC 16/008 – eCDF / PCN – Deletion of the extraordinary expenses and income categories: practical consequences.