UNOFFICIAL TRANSLATION

The Grand Ducal Regulation of 18 December 2015 determining the form and content of the balance sheet and profit and loss account layouts1 applicable to financial years starting on or after 1stJanuary 2016 introduced – in accordance with the accounting directive 2013/34/EU2 – new profit and loss account layouts in implementation of articles 46 and 47 of the amended law of 20023 (art. 46 LRCS, art. 47 LRCS). These new profit and loss account layouts (2016) differ in several respects from the old layouts (2015), particularly with regard to the presentation of financial income and expenses, which are now classified and grouped according to a new approach.

At the same time, the content and presentation of the Standard chart of accounts (PCN) remain – at this stage – those determined by the Grand Ducal regulation of 10 June 20094, the structure of which has not – for the time being – been adapted to the new layouts (2016).

As a result of the above, there is a partial disconnection between the accounts under section 65 “Financial expenses” and 75 “Financial income” in the PCN (2009) and the captions and sub-captions for financial expenses and income in the new profit and loss account and abridged profit and loss account (2016).

The changes in the presentation of financial expenses and income within the new profit and loss account layouts (2016), the differences with the old layouts (2015) previously in force and their partial disconnection with the captions for financial expenses and income in the PCN (2009) raise a number of practical questions, in particular:

Directive 2013/34/EU, which repeals and replaces the 4th and 7th Directives of 19785 and 19836, modernised the profit and loss account layout7 (renamed in the French version of the directive8).

Furthermore, as part of the work to transpose into Luxembourg law the provisions of directive 2013/34/EU relating to balance sheet and profit and loss account layouts9, it was noted that during the legislative reforms of 200210 then 2009 -201011/12 and 201313, Luxembourg layouts had deviated from European layouts at various points. In view of the objective of European accounting harmonisation underlying directive 2013/34/EU, it was decided to limit as far as possible the deviations of Luxembourg layouts from European layouts.

In this context, the Grand Ducal Regulation of 18 December 2015 has, on the one hand, introduced certain new features provided for by directive 2013/34/EU (e.g.: elimination of the category of extraordinary income and expenses14 within which certain financial income and expenses were presented) and, on the other hand, proceeded to eliminate a certain number of differences between the financial income and expense captions included within the European profit and loss account layouts and the financial income and expense captions included within the Luxembourg profit and loss account layout.

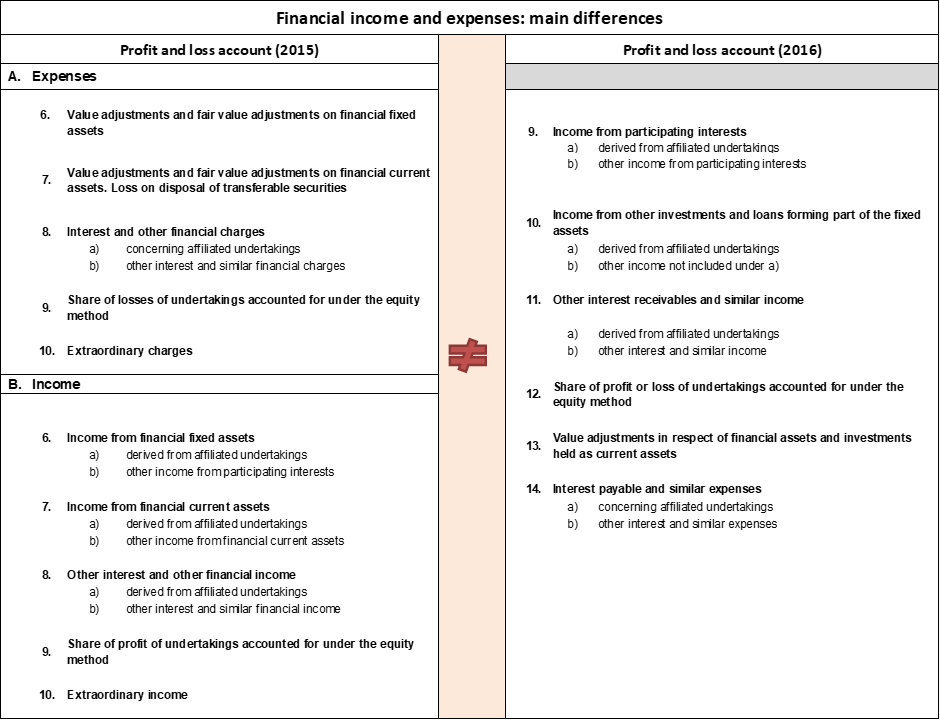

The main differences between the new and old financial income and expense captions are presented below (point 2.).

The main differences between the new (2016) and old (2015) captions of financial expense and income (2016) are summarised below. These differences result from a realignment of the financial income and expense captions in the Luxembourg profit and loss account layout with those included in the European layout. The result is a change in approach which is no longer based on a distinction between income from financial fixed assets and income from financial current assets.

To facilitate the transition for undertakings, mapping tables – indicative in nature[1] – are proposed in the appendices.

In this context, the purpose of appendices 1.a) and 1.b) is to facilitate the transition between the accounts under sections 65 “Financial expenses” and 75 “Financial income” of the PCN (2009) and the financial expense and income captions of the profit and loss account (2016). These appendices may prove particularly useful to preparers, especially when drawing up the profit and loss account (2016) based on a trial balance presented in accordance with the PCN (2009).

In addition, appendices 2.a) and 2.b) are intended to specify the relationship between the captions of financial assets and financial liabilities in the balance sheet and the captions of financial income and expenses in the profit and loss account and the financial income and expense accounts in the standard chart of accounts (PCN). These appendices may prove particularly useful to preparers, auditors and users when analysing and/or reviewing the annual accounts and the trial balance presented in accordance with the standard chart of accounts (PCN).

For reasons of readability, the tables presented in the appendices of the above Q&A have not been included here (HTML version). Please refer to the Q&A in PDF format to take note of said appendices.

*

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “eCDF / PCN – modifications dans la présentation des charges et des produits financiers (2016) : conséquences pratiques ”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible under general law for any decision taken on the basis of this document.

1 Grand Ducal Regulation of 18 December 2015 determining the form and content of the balance sheet and profit and loss account layouts and implementing Articles 34, 35, 46 and 47 of the amended law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings, Mém. A – N°258 of 28 December 2015.

2 Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertaking, OJ L 182, 29.6.2013.

3 Law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings, Mém. A – N°149 of 31 December 2002.

4 Grand Ducal Regulation of 10 June 2009 determining the content and presentation of a standard chart of accounts, Mém. A – N°145 of 22 June 2009.

5 Fourth Council Directive 78/660/EEC of 25 July 1978 based on Article 54 (3) (g) of the Treaty on the annual accounts of certain types of companies

6 Seventh Council Directive 83/349/EEC of 13 June 1983 based on Article 54 (3) (g) of the Treaty on consolidated accounts

7 See: Q&A CNC 16/010 “eCDF / PCN – New balance sheet and profit and loss statement formats (2016)

8 At this stage, it should be noted that the French terms “compte de profits et pertes” has been retained in Luxembourg accounting legislation. International accounting practice, and in particular IAS 1 as adopted by the European Union, allows in practice several synonymous terms for the statement of the undertaking’s performance (e.g. statement of net income, profit and loss account, income statement).

9 See: Explanatory memorandum and comments on the articles accompanying the draft Grand Ducal Regulation determining the form and content of the layout of the balance sheet and profit and loss account and implementing articles 34, 35, 46 and 47 of the amended law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings.

http://www.conseil-etat.public.lu/content/dam/conseil_etat/fr/avis/2015/07/17_07_2015/50_937/50937-Texte.pdf

10 Law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings (parliamentary document 4581)

11 Grand Ducal Regulation of 10 June 2009 determining the content and presentation of a standard chart of accounts

12 Law of 10 December 2010 on the introduction of international accounting standards for undertakings (parliamentary document 5976)

13 Law of 30 July 2013 reforming the Accounting standards board and amending various provisions relating to the bookkeeping and annual accounts of undertakings and the consolidated accounts of certain types of companies (parliamentary document 6376)

14 See: Q&A CNC 16/008 “eCDF / PCN – Deletion of the extraordinary expenses and income categories: practical consequences” (formerly Q&A PCN 01/2016)

15 The Grand Ducal Regulation of 10 June 2009 determining the content and presentation of a standard chart of accounts (Mém. A – N°145 of 22 June 2009) did not introduce a mapping table associating each of the accounts in the trial balance in PCN format with a balance sheet or profit and loss account caption. As a result, the assignment or grouping of PCN accounts within balance sheet and profit and loss account captions is left to the discretion of the undertaking’s administrative or management bodies in accordance with general accounting principles and the objective of a true and fair view.