UNOFFICIAL TRANSLATION

The Grand Ducal Regulation of 18 December 2015 determining the form and content of the layouts of balance sheet and of profit and loss account1 for financial years beginning on or after 1st January 2016 has deleted – in application of the accounting directive 2013/34/EU2 – the category of extraordinary income and expenses. At the same time, the content and presentation of the Standard chart of accounts (PCN) remain – at this stage – those determined by the Grand Ducal Regulation of 10 June 20093 which includes in class 6 relating to expenses a section 66 “Extraordinary expenses” and in class 7 relating to income a section 76 “Extraordinary income”.

The disconnection between the profit and loss account layout (including the abridged profit and loss account layout) and the PCN raises a number of issues, in particular:

No, there is no obligation.

Pursuant to article 2 of the Grand Ducal Regulation of 10 June 20094, undertakings are authorised not to fill in certain sections of the Standard chart of accounts (PCN) if alternative accounting methods exist or if their activity does not require the use of these sections.

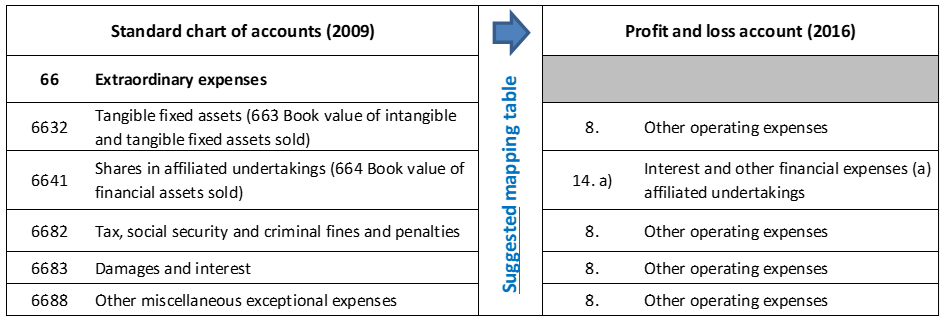

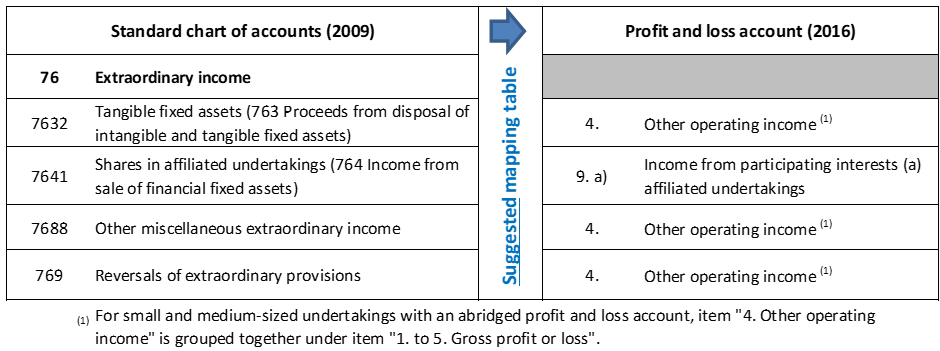

Data collected by the Central Balance Sheet Data Office (Centrale des bilans) tend to confirm that Luxembourgish undertakings make little use of the accounts under section 66 “Extraordinary expenses” and section 76 “Extraordinary income”, with only 9 of the 44 accounts under these two sections being used by more than 500 undertakings (see diagram below):

| 66 Extraordinary charges |

| 6632 Tangible fixed assets (663 Book value of yielded intangible and tangible fixed assets) |

| 6641 Shares in affiliated undertakings (664 Book value of yielded financial assets) |

| 6682 Tax fines and penalties in relation with tax, social and criminal matters |

| 6683 Indemnities for damage claims |

| 6688 Other miscellaneous extraordinary charges |

| 76 Extraordinary income |

| 7632 Tangible fixed assets (763 Income of yielded intangible and tangible fixed assets) |

| 7641 Shares in affiliated undertakings (764 Income of yielded financial fixed assets) |

| 7688 Other miscellaneous extraordinary income |

| 769 Reversal of extraordinary provisions |

Yes, this is possible.

Although undertakings are authorised not to fill in certain sections in the Standard chart of accounts (PCN), there is no legal or regulatory provision preventing them from using the PCN accounts, the content and presentation of which have been determined by the Grand Ducal Regulation of 10 June 2009.

As a result, undertakings are still free to use all the accounts included in the Standard chart of accounts (PCN), pending revision of the PCN.

It should be noted that the Grand Ducal Regulation of 10 June 2009 did not introduce a mapping table5 governing the articulation between the trial balance accounts in PCN format and the captions / headings of the balance sheet and of the profit and loss account.

In this context, the assignment or grouping of PCN accounts within the sections of the balance sheet and of the profit and loss account is at the discretion of the undertaking’s administrative or management bodies in accordance with general accounting principles and the true and fair view objective.

Without prejudice to the foregoing, it seems useful to provide undertakings with a suggested mapping table for the PCN accounts in section 66 “Extraordinary expenses” and in section 76 “Extraordinary income”.

For the accounts in sections 66 and 76 that are most commonly used by undertakings, the following suggested mapping table is proposed:

For all purposes, a suggested mapping table covering all PCN accounts under sections 66 “Extraordinary expenses” and 76 “Extraordinary income” is provided in the appendix (appendix 1).

As part of its work on the revision of the PCN, CNC questioned the usefulness of maintaining the categories of extraordinary income and of extraordinary expenses within the PCN despite the deletion of the corresponding captions / headings in the profit and loss account.

After careful consideration and review, CNC is considering – as part of the revision of the PCN – proposing the deletion of sections 66 “Extraordinary expenses” and 76 “Extraordinary income” in order to promote – in particular – a more intuitive correspondence between the trial balance accounts in PCN format and the profit and loss account.

This deletion of the accounts under sections 66 and 76 of the PCN would be accompanied – in part – by the creation of new PCN accounts similar to the deleted PCN accounts within other existing sections (e.g.: other operating expenses, other operating income). On the other hand, other PCN accounts would not be replaced following the removal of the underlying concepts (e.g.: allocations to extraordinary value adjustments) by the law of 18 December 20156.

Under this approach, undertakings wishing to do so will still be able to create – for internal management purposes – sub-accounts to meet their needs, for example in order to distinguishbetween normal value adjustments and extraordinary value adjustments. As part of the collection of financial data on the eCDF platform, these sub-accounts will be grouped together – as is currently the case – within existing PCN accounts.

For reasons of readability, the tables presented in the appendices of the above Q&A have not been included here (HTML version). Please refer to the Q&A in PDF format to take note of said appendices.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “eCDF / PCN – Suppression de la catégorie des charges et des produits exceptionnels : conséquences pratiques”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible in accordance with general law for any decisions taken on the basis of this document.

1 Grand Ducal Regulation of 18 December 2015 determining the form and content of the layouts of the balance sheet and of the profit and loss account implementing articles 34, 35, 46 and 47 of the amended law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings, Mem. A – N°258 of 28 December 2015.

2 Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, OJ L 182, 29.6.2013.

3 Grand Ducal Regulation of 10 June 2009 determining the content and presentation of a standard chart of accounts, Mem. A – N°145 of 22 June 2009.

4 Article 2 of the Grand Ducal Regulation of 10 June 2009:

“Within the framework of generally accepted accounting methods that comply with general accounting principles, undertakings are authorised not to fill in certain sections of the Standard chart of accounts (PCN) if there are alternative accounting methods that do not require the use of these sections or if their activity does not justify the use of certain sections”.

5 Also known as the correspondence table, concordance table between the trial balance accounts in PCN format and the sections of the balance sheet and of the profit and loss account.

6 Law of 18 December 2015 amending, with a view to the transposition of Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC: 1) the amended law of 10 August 1915 on commercial companies; 2) Title II of the amended law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings; 3) Title II of Book I of the Commercial code, Mem. A – N°258 of 28 December 2015.