UNOFFICIAL TRANSLATION

Pursuant to Article 15 of the Commercial code, “Any undertaking shall draw up once a year a complete inventory of its assets and rights of any kind and of its liabilities, obligations and commitments of any kind. After their reconciliation with the inventory, the accounting books shall be summarised in a descriptive document which shall form the annual accounts”.

It is generally accepted in Luxembourg that the financial year of an undertaking normally lasts 12 months1, which may or may not correspond to the calendar year2, with the exception of extraordinary situations such as the financial year following incorporation, the financial year of transition when the closing date of the financial year is changed during the existence of the undertaking and the final financial year of liquidation at the end of which the undertaking definitively ceases to exist.

If the majority practice in Luxembourg is to close a financial year on a fixed date – for example: 30 June each year – and therefore to have financial years lasting 365 days in non-leap years and 366 days in leap years, the question arises as to whether it is permissible for a Luxembourg undertaking to have a financial year ending on a variable date – for example: each year, on the last Saturday in June (Saturday 30 June 2012, Saturday 29 June 2013, Saturday 28 June 2014, Saturday 27 June 2015, Saturday 25 June 2016, etc.) – a practice known as floating financial year3.

Although it has to be said that the practice of the floating financial year is little known in the Grand Duchy of Luxembourg, nothing seems to prohibit this practice as long as it does not undermine the principle of annuality of the inventory and of the annual accounts – particularly with regard to the obligation to inform and protect shareholders and third party creditors – as well as the objective of comparability of the undertaking’s performance and results over time.

In view of the above, the Accounting Standards Board (CNC) considers that it is important – if the practice of the floating financial year is to be accepted – that the floating financial year should have a duration close to that of a calendar year and a duration that is comparable from one financial year to the next. In addition, the opening date and closing date of the floating financial year must meet the criteria of predictability and determinability in order to prevent the floating financial year from being a financial year with random dates and of an arbitrary duration, a practice which would be prohibited.

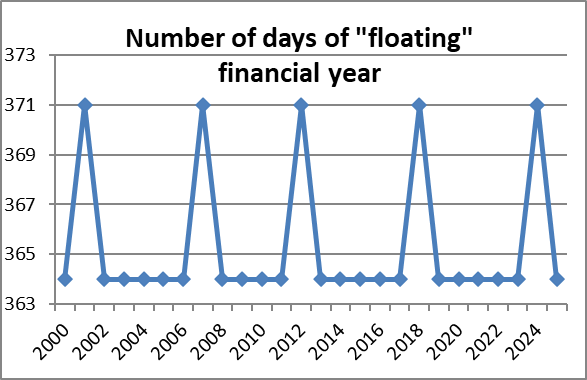

In this respect, the Accounting Standards Board (CNC) notes that the practice of the floating financial year known across the Atlantic seems to make it possible to achieve these objectives of annuality, comparability in terms of duration and predictability and determinability of the opening and closing dates of the financial years. In practice, a floating financial year has a “usual” duration of 52 weeks (i.e. 364 days) with a catch-up effect approximately every 5 to 6 years, when the floating financial year has an “extended” duration of 53 weeks (i.e. 371 days) (see Appendix 1).

The Accounting Standards Board (CNC) also points out that the practice of floating financial year is expressly recognised by international accounting standard IAS 1 “Presentation of financial statements” as adopted by the European Union and which provides in its paragraph 37 that:

“Normally, an entity consistently prepares financial statements for a one-year period. However, for practical reasons, some entities prefer to report, for example, for a 52-week period. This Standard does not preclude this practice.”

Considering that in Luxembourg, undertakings are authorised to draw up their annual accounts using international financial reporting standards (IFRS) as adopted by the European Union4, the Accounting Standards Board (CNC) considers that it would obviously not be fair to prohibit the practice of floating financial year for undertakings presenting their annual accounts in accordance with national accounting provisions (LUX GAAP), while those presenting their annual accounts in accordance with IFRS could be authorised to use this practice.

Consequently, and subject to compliance with the aforementioned conditions, the Accounting Standards Board (CNC) is of the opinion that all Luxembourg undertakings should be allowed to use the practice of floating financial year without distinction based on the accounting framework used (IFRS or LUX GAAP).

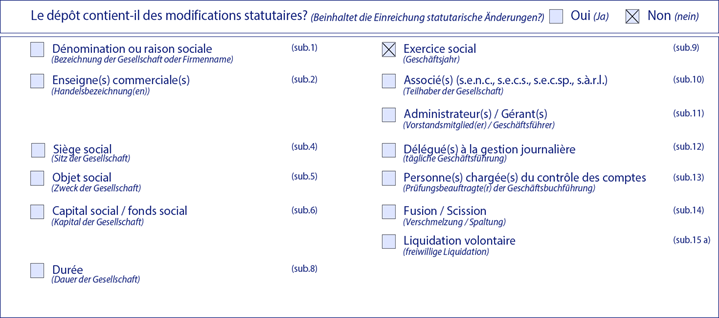

Without prejudice to the above, the Accounting Standards Board (CNC) notes that, as the system for collecting information relating to undertakings currently stands, the specific dates of the calendar days on which the financial year begins (e.g.: [Sunday] 30 June 2013) and ends (e.g.: [Saturday] 28 June 2014) must be provided to the Trade and companies register (RCS). In this context, undertakings wishing to take advantage of the floating financial year are therefore obliged to submit an amending requisition form to the RCS each year in order to adjust the start and end dates of their financial year (Cf.: appendix 2).

This guidance concludes that the floating financial year is acceptable for all Luxembourg undertakings, regardless of the accounting framework used (IFRS or LUX GAAP). In order for the practice of the floating financial year to be acceptable without undermining the principle of annuality of the inventory and of the annual accounts, it is important that the floating financial year has a duration close to that of a calendar year and a duration that is comparable from one financial year to the next, i.e. in practice a duration of between 52 and 53 weeks. In addition, the opening and closing dates of the floating financial year must meet the criteria of predictability and determinability, to ensure that the floating financial year is not a financial year with random dates and an arbitrary duration.

As the system for collecting information on undertakings currently stands, it will be up to undertakings using a floating financial year to notify the RCS each year of the specific start and end dates of their current financial year by means of an amending requisition.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Notion comptable d’exercice flottant”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible under general law for any decision taken on the basis of this document.

——

Financial year with a floating date: illustrative example

The purpose of this appendix is to provide a practical example of the floating financial year.

For the purposes of this illustration, the example of a financial year ending each year on the last Saturday in June is used (e.g.: Saturday 29 June 2013, Saturday 28 June 2014, Saturday 27 June 2015, Saturday 25 June 2016, etc.). As a result, each year the financial year begins on the day following the last Saturday in June, which is generally the last Sunday in June (e.g. Sunday 30 June 2013, Sunday 29 June 2014, Sunday 28 June 2015, Sunday 26 June 2016, etc.). However, there is an exception to this rule once every 5 to 6 years, when the last Saturday in June corresponds to the last day of June (e.g. Saturday 30 June 2001, 2007, 2012, 2018, etc.), with the result that the next financial year begins on the first Sunday in July (e.g. Sunday 1st July 2001, 2007, 2012, 2018, etc.).

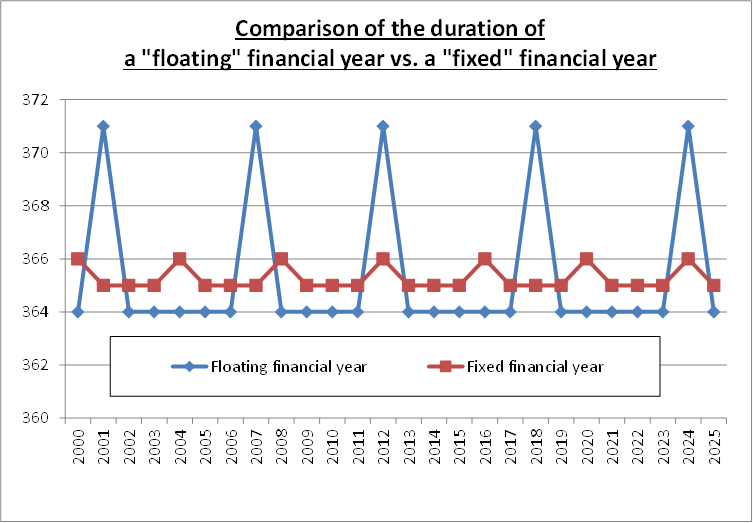

This illustration (see diagrams below) shows that, over an extended period5, a floating financial year generally lasts 52 weeks, or 364 days, with the exception of approximately once every 5 to 6 years, when the financial year is then “extended” to 53 weeks, or 371 days. This exception has the effect of catching up by realigning the closing date of the floating financial year with that of a financial year with a fixed closing date (in this case, 30 June).

This illustrative example confirms that the floating financial year, understood as having a “usual” duration of 52 weeks and an “extended” duration of 53 weeks once every 5 to 6 years, makes it possible to achieve the objectives of annuality of the inventory and of the annual accounts, comparability in terms of duration as well as in terms of predictability and determinability of the opening and closing dates of the financial years.

Compared with a financial year ending on a fixed date (e.g. calendar year), a floating financial year certainly has greater variability, but this variability in the duration of the financial year of less than 2% remains reasonable in view of the principle of annuality and the objective of comparability (see diagram below).

——

Practical aspects of using a floating financial year: annual obligation to file an amending requisition for the undertaking’s financial year with the Trade and companies register (RCS)

As the system for collecting information on undertakings currently stands, the specific dates of the calendar days on which the undertaking’s financial year begins (e.g. [Sunday] 30 June 2013) and ends (e.g. [Saturday] 28 June 2014) must be provided to the manager of the Trade and companies register (RCS).

In this context, undertakings wishing to avail themselves of the practice of a floating financial year are therefore obliged to submit an amending requisition form to the RCS each year in order to adjust the start and end dates of their financial year (see illustrative example below).

1 See: Article 13, third indent of the Commercial code covers the extraordinary situation where the financial year lasts more than 12 months:

“In case the financial year has a duration of less or more than 12 months, the amount referred to in the first indent is multiplied by a fraction, the denominator of which is 12 and the numerator of which is the number of months included in the relevant financial year, any incomplete month being counted as a full month”

2 See Article 75, first indent:

“Undertakings referred to in Article 25 shall deposit with the trade and companies register their annual accounts, duly approved in the case of legal entities, and the trial balance of the accounts featured in the standard chart of accounts defined in Article 12 paragraph 2 of the Commercial Code, within a month of their approval and at the latest seven months after the end of the calendar year, in the case of individual business persons or the financial year end, in case of legal entities”

3 The French concept of “exercice flottant” is the literal translation of the North American concept of “floating financial year”. This practice is well known in the United States, where it seems to be guided essentially by operational considerations (e.g. alignment with weekly internal reporting, planning of annual physical inventory, etc.). In this context, undertakings which are European subsidiaries of US groups may seek to align their financial year with the floating financial year of their parent company for reasons relating in particular to intra-group reporting and consolidation.

4 In application of Article 72bis of the law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings.

5 For the purposes of this illustrative example, a period of 25 years has been considered.