UNOFFICIAL TRANSLATION

The going concern assumption is the founding pillar of international, European and national accounting standards. Certain general accounting principles, such as the principle of separation or independence of financial periods, derive directly from the assumption that the undertaking has the capacity to continue operations for the foreseeable future.

If the undertaking does not have the capacity to continue as a going concern, or if the management or administrative body intends to liquidate the undertaking or cease operations, the undertaking is then in a situation of discontinuity of operations. In principle, the annual accounts of the undertaking can no longer be prepared on a going concern basis. Consequently, an alternative basis of accounting must be used. In this context, reference is generally made to the notion of “liquidation basis of accounting”, a concept that is well known to accounting professionals, but whose contours are vague and whose geometry is variable.

It has to be said that neither Luxembourg accounting legislation, nor European accounting legislation, nor the IFRS international accounting standards, satisfactorily characterise the principles and methods of accounting on a liquidation basis. The result is a wide variety of practices, which is a source of legal uncertainty for stakeholders in the accounting arena: preparers (including liquidators), auditors and users (shareholders, third-party creditors, public users).

In this context, this Q&A aims at contributing to the harmonisation of accounting practices for undertakings in a situation of discontinuity of operations or in liquidation by specifying the procedures for implementing the liquidation basis of accounting as well as the simplification measures that – depending on the circumstances – are available or even appropriate.

*

Disclaimer:

This Q&A applies to undertakings covered by general accounting legislation (Title II LRCS) and proposes methods and principles for implementing the liquidation basis of accounting. As 97% to 98%1 of the undertakings covered by Title II LRCS are “small undertakings” within the meaning of Article 35 LRCS2, simplification measures are sometimes available and even appropriate. However, the use of these simplification measures is not limited to small undertakings but rather targets situations where the discontinuity or the liquidation is not expected to generate losses for third-party creditors and for shareholders. These simplification measures are generally not available or appropriate for public interest entities or for undertakings covered by Title II LRCS that are subject to prudential supervision. In the case of such undertakings, it is up to the supervisory authority to specify the procedures for implementing the liquidation basis of accounting.

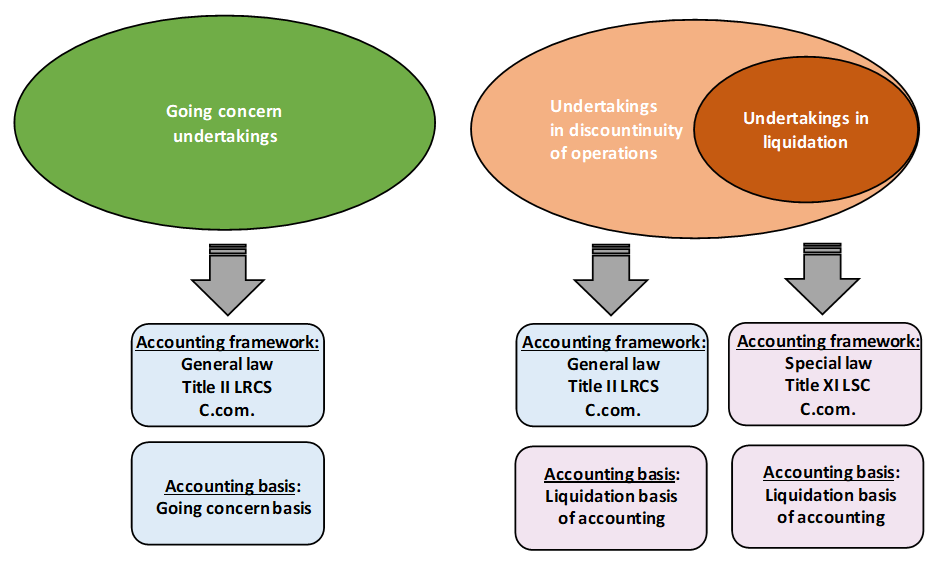

As the law currently stands, it is accepted in practice that general accounting legislation (Title II LRCS) ceases to apply as from the date on which the undertaking goes into liquidation. The fragmented accounting provisions of Title XI LSC (special accounting legislation) then apply. A change of accounting basis is generally made with a transition from a going concern basis of accounting to a liquidation basis of accounting. When an undertaking goes into liquidation, liquidation accounts are generally drawn up by the outgoing administrative or management body. Then, on an annual basis, the liquidator reports on the progress of the liquidation procedures by drawing up annual / interim liquidation accounts. When the liquidation is complete, closing liquidation accounts covering the entire liquidation period – often several years – are drawn up and controlled by a specially appointed supervisory auditor (“commissaire”)3. These accounts are submitted to the general meeting for approval, which then decides whether to grant discharge to the liquidator in respect of the performance of his duties. It should be noted that during the liquidation procedure, the accounts drawn up by the liquidator are subject to a system of preparation, control, filing and publication that differs significantly from that provided for under general accounting legislation. During the transitional period between the determination that the undertaking is no longer a going concern and its formal liquidation, it is generally accepted that the general accounting legislation (Title II LRCS) continues to apply, subject to adjustments required by the change in the basis of accounting.

General accounting law applicable to undertakings (Title II LRCS) is based on the central assumption of going concern (art. 51 (1) a) LRCS) from which other accounting conventions derive, including the principle of independence or separation of financial years and, more generally, the principle of accrual basis of income and expenses (art. 51 (1) d) LRCS) or the principle of prudence and its asymmetrical treatment of expenses and income (art. 51 (1) c) aa), bb) LRCS).

The preparatory work of the accounting law thus states that “[b]y virtue of this principle, the annual accounts of a company are those of an undertaking which will continue its operations in the foreseeable future. The valuation / measurement of assets and their depreciation according to their useful economic life are based on this principle. The annual accounts are therefore not those of an undertaking in liquidation“4.

In view of the above, standard practice is to consider that general accounting law ceases to apply when an undertaking goes into liquidation, as the central assumption of going concern can no longer be applied.

As a result, the undertaking in liquidation falls outside the scope of general accounting law. The general framework provided by Title II LRCS (general law) is replaced by the specific framework provided by Title XI LSC5 (special law). Although fragmented and even incomplete, Title XI LSC (formerly Section VIII LSC) sets out specific accounting obligations for undertakings in liquidation. Article 1100-14 LSC (formerly art. 150 LSC) provides that “[e]ach year, the results of the liquidation shall be submitted to the general meeting of the company, together with a statement as to the reasons which have prevented completion of the liquidation. In the case of sociétés anonymes, the balance sheet shall also be published.”

It may usefully be noted that the wording of Article 1100-14 LSC has not changed in substance since its publication in 19156. This explains in particular why the obligation to publish accounts – historically restricted to limited companies by shares – remains limited (in the absence of subsequent changes) to companies in liquidation organised in the form of a “société anonyme” as well as – by extension – of a “société en commandite par actions”7 and of a “société européenne”8. As the legislation currently stands, other forms of limited liability companies or similar, including the “société à responsabilité limitée” (S.à r.l.)9/10, are therefore excluded from the obligation to publish their accounts when they are in liquidation, even though general accounting law requires them to publish their accounts when they are a going concern, in application of the axiom “publicity of the accounts as a counterpart to the limited liability of shareholders“. CNC notes an inconsistency in Luxembourg accounting law, as there is no a priori justification for a separate scope of application for the publicity of accounts. Undertakings subject to publication of their annual accounts when they are a going concern should also be subject to publication when they are in liquidation, as the objective of protecting third parties through accounting information justifies such publicity in both cases.

Whilst it is accepted – under current legislation and practice – that Title II LRCS (general accounting law) applies to companies operating on a going-concern basis and that Title XI LSC (special accounting law) applies to companies in liquidation, the question naturally arises as to the framework applicable to companies in a situation of discontinuity of operations prior to their being placed in liquidation.

In this respect, it should first be clarified that the accounting concept of a going concern refers to a de facto situation where the undertaking does not have the capacity to continue its operations or where the management or administrative body intends to liquidate the undertaking or cease its activity. In practice, an undertaking often finds itself in a situation of discontinuity of operations without legally being in liquidation11. For these undertakings, the usual practice is to conclude that general accounting law continues to apply during this period. However, because of the discontinuity of operations, adjustments are generally necessary and a transition is made from a “going concern basis of accounting” to a “liquidation basis of accounting” – known in practice as a “change of accounting basis”. From a legal point of view, these adjustments are made on the basis of Articles 26(5) LRCS12 and 51(2) LRCS13, which require departures from general accounting principles in order to achieve the overriding objective of a true and fair view (art. 26(3) LRCS).

The diagram below (see Fig. A) summarises the accounting framework and basis of accounting applicable to undertakings, depending on whether they are operating as a going concern or they are in a situation of discontinuity of operations, before or after going into liquidation.

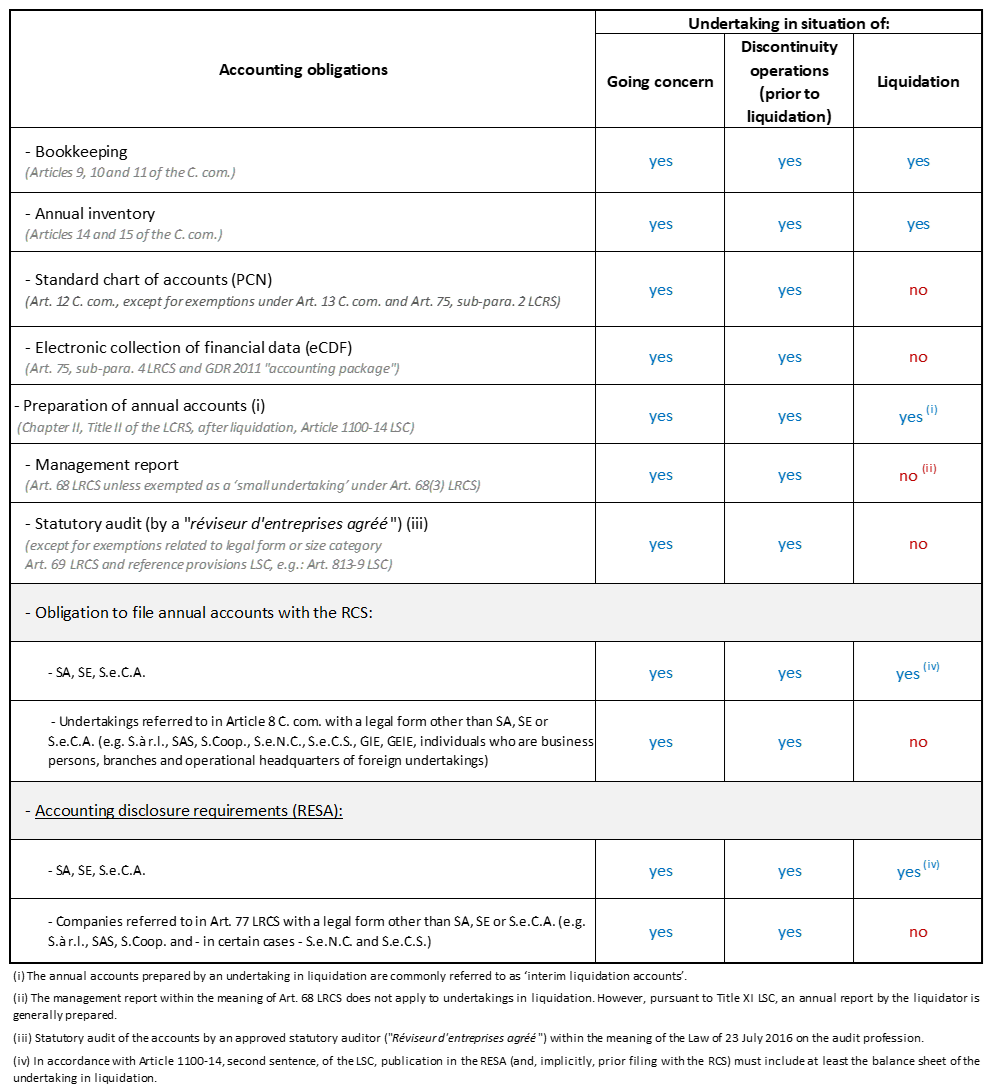

The table below (see Fig. B) sets out the accounting obligations applicable to these undertakings.

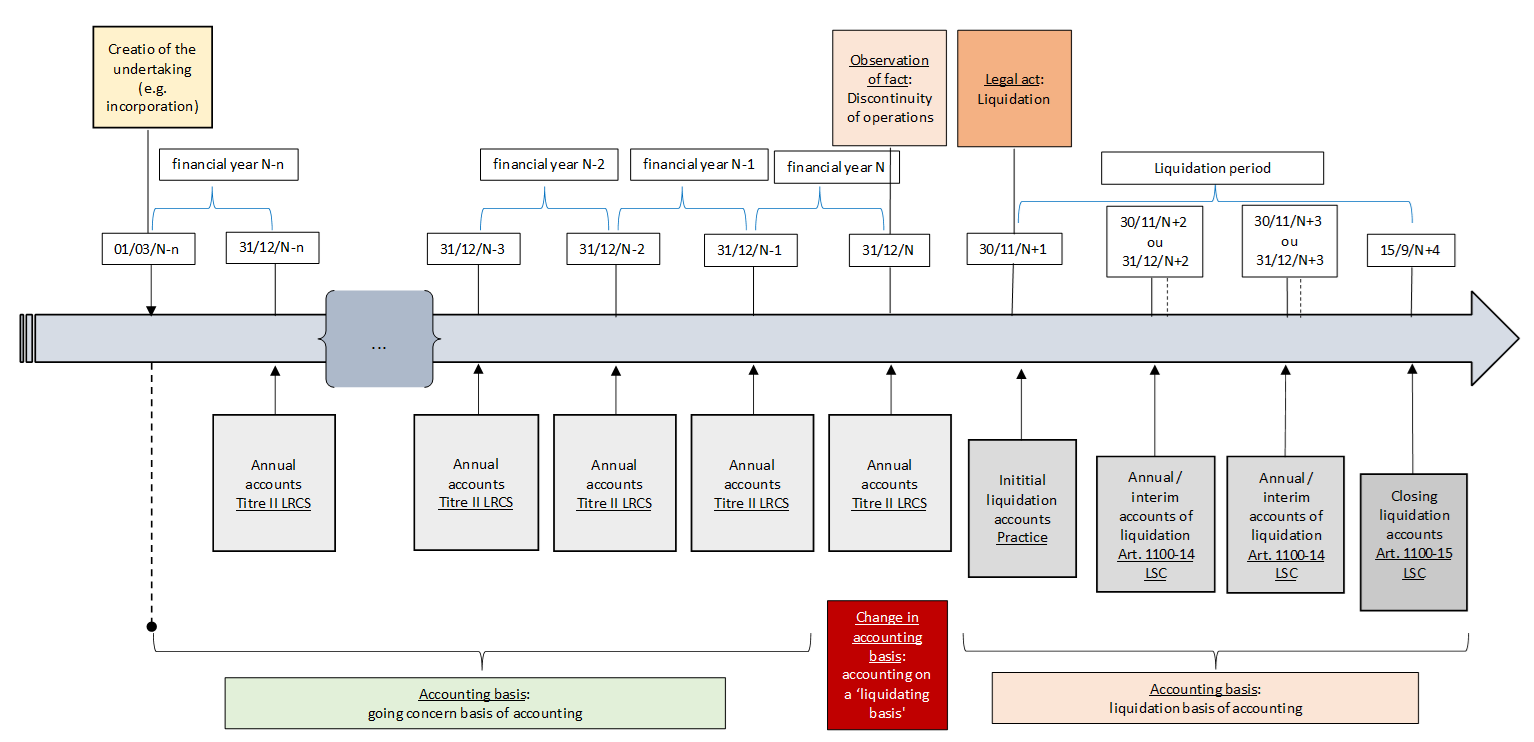

The illustrative diagram below (Fig. C) shows, in the form of a timeline, the key stages in the life of an undertaking from its creation / incorporation to its liquidation, with the accounting implications associated with each of these key stages.

The key concepts used – implicitly or explicitly – in the above illustrative diagram, (see Fig. C) can be defined as follows:

Undertakings within the meaning of Article 8 of the Commercial code, i.e.:

While the majority of undertakings are organised in corporate or similar form, some are sole proprietorships which may be in a situation of discontinuity of operations but which are not legally subject to the liquidation procedure as referred to in this Q&A (e.g. individual business persons, branches and head of operations of undertakings governed by foreign law).

It should be noted that this Q&A does not apply to undertakings that are not subject to general accounting law (Title II LRCS), such as credit institutions and insurance and reinsurance companies. Public interest entities and undertakings subject to prudential supervision, covered by Title II LRCS, are in the scope of this Q&A to the extent and subject to the adjustments provided for by the sector-specific provisions or required by their supervisory authority.

For the purposes of this Q&A, the term “liquidation” refers essentially to the “voluntary liquidation” mentioned in Title XI LSC and understood as the process which follows a decision to voluntarily dissolve the undertaking as taken by the shareholders of a commercial company, following which a liquidator is appointed with the task of realising / selling the assets and settling / reimbursing the liabilities and with the obligation to report periodically on the results of this liquidation to the general meeting of shareholders.

Although this Q&A has not been developed specifically with this in mind, there is nothing a priori to prevent the principles and methods of the “liquidation basis of accounting” as described in part 2 from being used – for example – by receivers (“curateurs”) in charge of administering a bankruptcy (Book III C. com.14), by liquidators in charge of a judicial liquidation (Title XII LSC15) or by “commissaires” in charge of a controlled management regime or “régime de gestion contrôlée” (Grand Ducal Decree of 24 May 1935 )16.

However, this Q&A does not generally cover so-called voluntary dissolutions without liquidation (also known in practice as “dissolution by transfer of all shares to a single shareholder” or “simplified dissolutions”)17.

Under general accounting law and company law, the annual accounts are drawn up each year at the end of the financial year. For legal entities, the financial year generally corresponds to the calendar year, although other dates may be used (known as the “divergent financial year”). Explicit reference to this financial year is generally made in the articles of association.

Although the “statutory” financial year is the reference period at the end of which the annual accounts of an undertaking subject to general accounting law are drawn up, the question arises as to the date on which the annual accounts of an undertaking are closed after it has gone into liquidation. In this respect, and in accordance with usual practice, the date on which the annual accounts of a company in liquidation are closed may correspond either to the date on which its “statutory” financial year ends (e.g. 31 December of each year in the illustrative example – Fig. C) or to the “anniversary date” on which it has gone into liquidation (e.g. 30 November of each year in the illustrative example – Fig. C).

Although there is currently no legal requirement to do so, it is generally useful or even necessary for the administrative or management body to draw up an accounting statement for the undertaking at the time of going into liquidation. In practice, this accounting statement is usually referred to as “initial liquidation accounts”. The purpose of these initial liquidation accounts is to highlight the financial situation of the undertaking at that date (assets to be realised / sold, liabilities to be settled / reimbursed and net asset position) and to some extent constitute the inventory of the “outgoing” administrative or management body, whose term of office comes to an end when the undertaking is put into liquidation and on the basis of which a discharge is requested. For the “incoming” liquidator, these liquidation accounts constitute the opening situation, the starting point for a mandate aiming at realising / selling the assets and at settling / reimbursing the liabilities.

It should be noted that these initial liquidation accounts do not constitute annual accounts within the meaning of Title II LRCS and are therefore not drawn up, audited18, filed and published in accordance with general accounting law. It should be noted, however, that undertakings organised in the form of a “société anonyme”, a “société européenne” or a “société en commandite par actions” have the option (and not the obligation) of requesting that these be filed with the Trade and companies register (RCS) for publication in the Electronic compendium of companies and associations (RESA).

According to the prevailing interpretation, once the undertaking has been put into liquidation, it is exempt from drawing up annual accounts under general accounting law (Title II LRCS). However, special accounting law (Title XI LSC) requires the liquidator to submit the results of the liquidation to the general meeting each year.

In practice, it seems to be accepted that, in order to report on the results of the liquidation over the past year, the liquidator presents a balance sheet showing the assets still to be realized / sold, the liabilities still to be settled / reimbursed and the net asset position, a profit and loss account showing the expenses and income recognised during the financial year, and notes to the accounts showing, in particular, the accounting principles, policies and methods used. In other words, the liquidator prepares annual accounts on an annual basis for the duration of the liquidation, on the understanding, however, that these annual accounts may dispense with the formal aspects specific to general accounting law (Title II LRCS).

Thus, the undertaking in liquidation is not obliged to follow the balance sheet layout set out in article 34 LRCS, the profit and loss account layout set out in article 46 LRCS or the content of the notes to the accounts set out in article 65 (1) LRCS.

It should also be noted that, as the legislation currently stands, these annual accounts are not subject to statutory audit by the “réviseur d’entreprises agréé” [approved statutory auditor], regardless of the size category of the undertaking. The liquidator may, of course, on his own initiative or with the agreement of the general meeting, submit the said accounts to a contractual audit by a “réviseur d’entreprises agréé” [approved statutory auditor].

As mentioned above (see: financial year), these annual accounts may be drawn up either on the anniversary date of the liquidation or on the closing date of the “statutory” financial year.

In practice, these annual accounts are often referred to as “interim liquidation accounts”, as they represent an interim statement that only reports on part of the liquidation activities, i.e. those that took place during the past year (see “liquidation closing accounts”). An interim report by the liquidator is usually attached to these annual / interim liquidation accounts.

These annual / interim liquidation accounts are presented annually to the general meeting, which thus takes note of the progress of the liquidation process. In this respect, and despite the silence of the texts, it is important that the annual / interim liquidation accounts are made available to the general meeting within a reasonable time19. The informational value and relevance of the financial data produced depend on this. It should be noted, however, that the general meeting of the undertaking in liquidation does not approve the annual / interim liquidation accounts, nor does it grant discharge to the liquidator on this basis. This process of approving the accounts and granting discharge is deferred until the liquidation is completed (see: liquidation closing accounts).

As regards filing with the RCS for publication in the RESA, a distinction must be made according to the legal form of the undertaking (see point 1.1. above)20. If the undertaking is organised in the form of a “société anonyme”, a “société européenne” or a “société en commandite par actions”, it is required to file at least its balance sheet with the RCS for publication in the RESA (art. 1100-14, 2nd sentence LSC). On the other hand, undertakings in liquidation organised in another legal form (e.g. a “société à responsabilité limitée”) do not have an obligation21 to file their annual / interim liquidation accounts with the RCS and publish them in the RESA.

Article 1100-15 LSC provides that once the liquidation procedure has been completed, the liquidator must draw up closing liquidation accounts. These accounts cover the entire liquidation period from the date on which the liquidation was initiated to the date on which the liquidation was closed (i.e. from 30 November N+1 to 15 September N+4 in the illustrative example – Fig. C). In most cases, therefore, the accounts cover a multi-year period.

Title XI LSC does not provide any details as to the form and content of said closing liquidation accounts. As a result, there is no obligation to draw up said closing liquidation accounts in accordance with the provisions of Title II LRCS, as the undertaking in liquidation is no longer subject to general accounting law in accordance with usual practice. In practice, said closing liquidation accounts include at least a balance sheet, a profit and loss account and explanatory notes. In addition, a final report by the liquidator generally accompanies the closing liquidation accounts.

Without prejudice to more restrictive sector-specific provisions22, the control of closing liquidation accounts is generally entrusted to a “commissaire” specially appointed for this purpose by the general meeting. It should be noted that, although the mandate of “commissaire (à la liquidation)” may be entrusted to a “réviseur d’entreprises”, there is no legal obligation to do so. In addition, as the law currently stands, the assignment entrusted to the “commissaire” does not constitute a statutory audit or an audit of the accounts.

Once they have been controlled by the “commissaire”, the closing liquidation accounts are submitted to the general meeting for approval, which then decides on the discharge to be granted to the liquidator in respect of the performance of his duties. In this respect, and despite the silence of the texts, it is important that the closing liquidation accounts are made available to the general meeting within a reasonable period of time23. The informational value and relevance of the financial data produced are at stake.

As regards the filing and publication of the closing liquidation accounts, it should be noted that Title XI LSC makes no provision for such an obligation. Consequently, companies in liquidation – regardless of their legal form – are not required to file their closing liquidation accounts with the RCS. It should be noted that if an undertaking organised in the form of a “société anonyme”, a “société européenne” or a “société en commandite par actions” wishes to file and publish its closing liquidation accounts on a voluntary basis, the manager of the RCS24 may accept such a request.

*

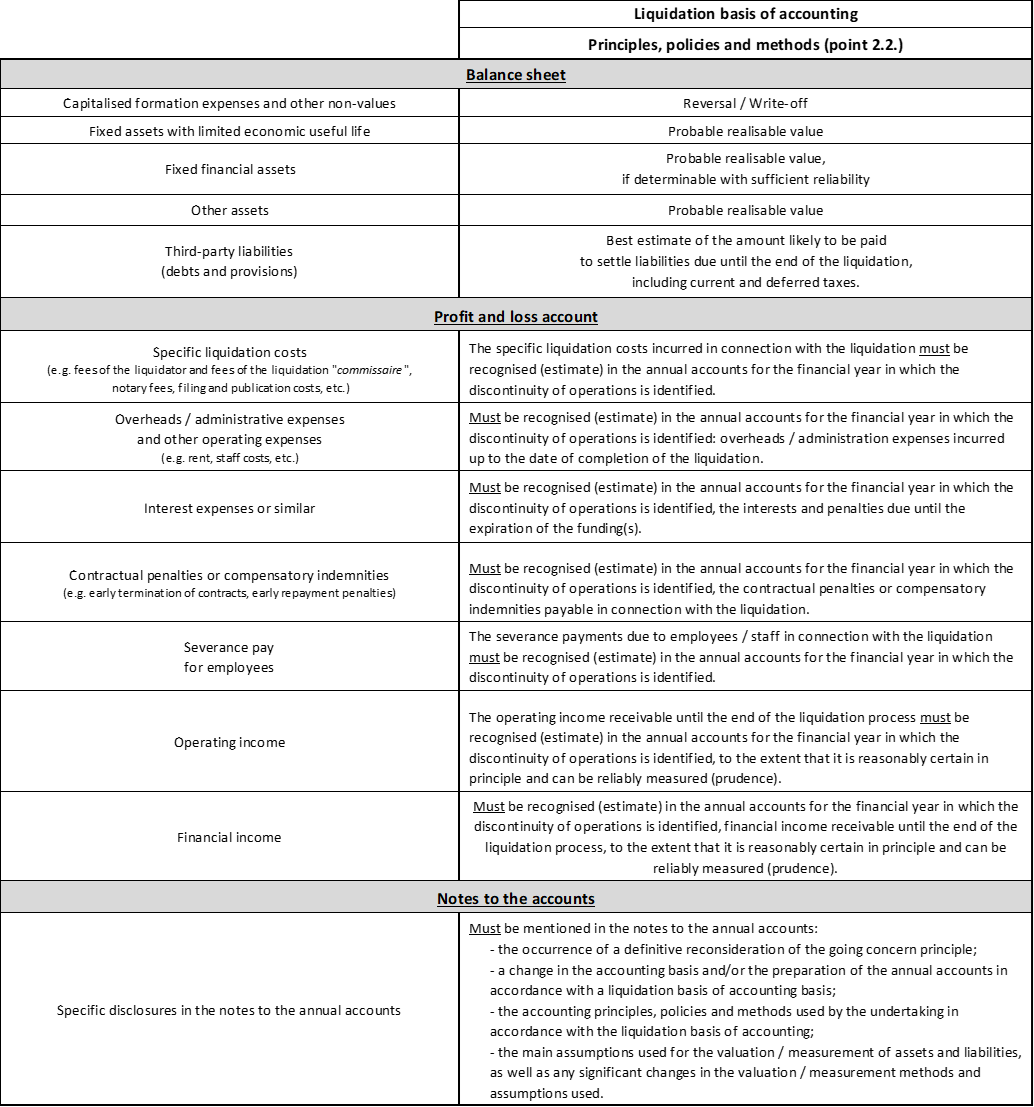

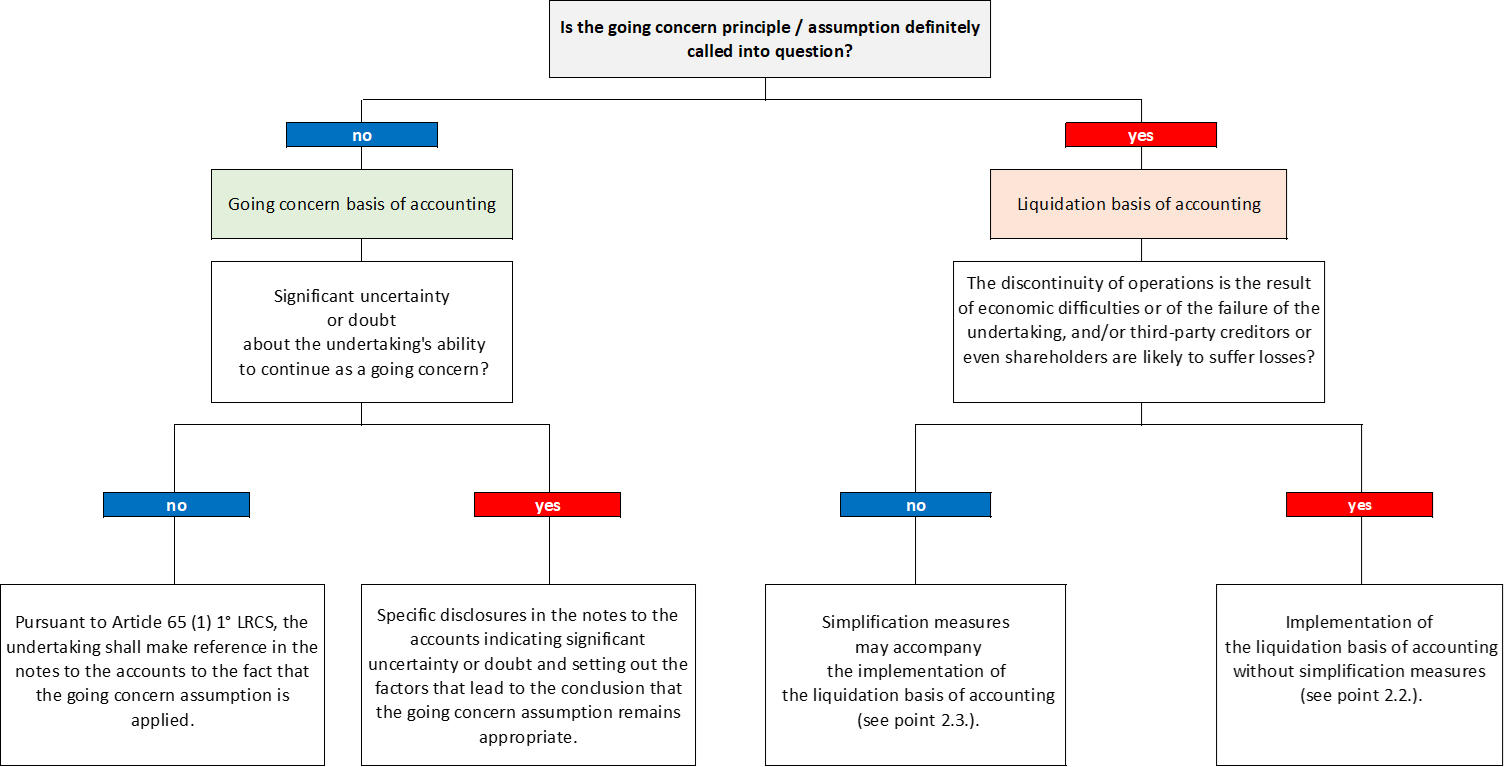

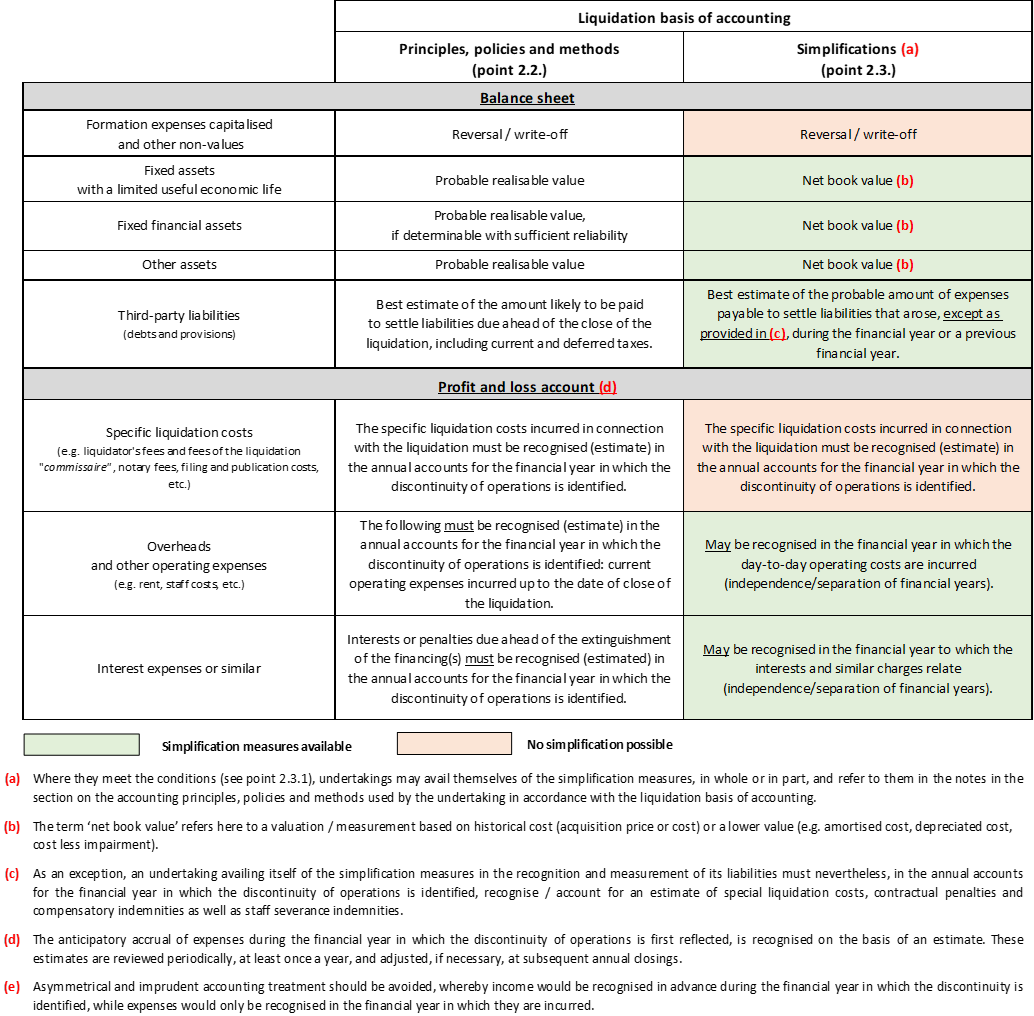

In the absence of specific provisions, CNC considers that it is up to the administrative or management body or to the liquidator to articulate the principles, policies and methods of “liquidation basis of accounting” that depart from those applicable to “going concern basis of accounting”. By departing from the principle of the separation or independence of financial years and from valuation / measurement by reference to “historical cost” (which is generally replaced by valuation / measurement at “probable realisable value”), “liquidation basis of accounting” focuses, as soon as the going concern is discontinued, on the inventory of all the assets to be realised / sold and all the liabilities to be settled / reimbursed prior to the closing of the liquidation. This approach makes it possible to estimate the final net asset position and, where appropriate, to identify any potential losses to be suffered by third-party creditors and shareholders whom accounting law seeks to protect.

These principles and methods of “liquidation basis of accounting” are a general rule. Their application is particularly appropriate in cases of discontinuity of operations or liquidation caused by economic difficulties or failure of the undertaking, which call into question its solvency and liquidity.

However, since not all liquidations are the result of economic failures and do not give rise to losses for third-party creditors or even shareholders, simplification mechanisms – particularly in the valuation / measurement of assets and the recognition of liabilities – can be implemented in certain situations. In practice, these simplifications are essentially aimed at undertakings whose discontinuity of operations is the result of management decisions (e.g. voluntary termination of business, extinction of corporate purpose, intra-group reorganisation) and whose solvency and liquidity are not called into question.

In cases where the undertaking does not have the capacity to continue as a going concern or where the management or administrative body intends to liquidate the undertaking or cease business / trading, the undertaking is in a situation of discontinuity of operations (see point 3.1.). In principle, the annual accounts of the undertaking can no longer be prepared on a going concern basis. Consequently, an alternative basis of accounting must be used. As a general rule, this is referred to as “liquidation basis of accounting”.

However, it should be noted that neither general accounting law (Title II LRCS) applicable to an undertaking in a situation of discontinuity of operations prior to its liquidation, nor special accounting law (Title XI LSC) applicable to an undertaking in a situation of discontinuity of operations after its liquidation, have formulated accounting principles, policies or methods applicable in case of discontinuity of operations.

In this context, it is up to the administrative or management body25 or to the liquidator26 to articulate principles, policies and methods that depart from the “going concern basis of accounting”. CNC considers that this is a direct consequence of the silence of the legislation, since the legislator has not set out the principles, policies and methods of a “liquidation basis of accounting”.

In formulating the principles, policies and methods of a “liquidation basis of accounting” applicable to the undertaking, the management or administrative body or the liquidator is expected to give due consideration to the objectives of accounting information during a period of discontinuity of operations, in particular with regard to the objective of protection of third-party creditors and shareholders.

In this context, prudence will in many cases require the formulation of “liquidation basis of accounting” principles, policies and methods that favour maximum inclusiveness of the assets to be realised / sold and the liabilities to be settled / reimbursed prior to the close of the liquidation (see point 1.1.). This will be the case in particular where the discontinuity of operations is the consequence of economic difficulties or even of the failure of the undertaking and where these circumstances are likely to result in losses for third-party creditors (or even for shareholders) whom accounting law seeks to protect.

On the other hand, there are cases where the discontinuity of operations and the liquidation are not the consequence of economic difficulties but rather the result of management decisions taken at the level of the undertaking (e.g.: voluntary cessation of activity, sale of the business, extinction of the corporate purpose, etc.) or at the level of the group to which the undertaking belongs (e.g.: intra-group reorganisation, transfer and/or relocation of activities, etc.). As a general rule, the undertaking remains, in these circumstances, liquid and solvent, so that the settlement / reimbursement of its liabilities does not appear to be a problem, as no loss is anticipated for third-party creditors or even for shareholders. In such cases, the formulation of proportionate “liquidation basis of accounting” principles, policies and methods, incorporating simplification measures, sometimes seems appropriate in view of the undertaking’s situation vis-à-vis its stakeholders, and even adequate in view of the undertaking’s size (see point 2.2.).

Finally, it has been pointed out that the dissolution and liquidation of an undertaking does not always result in the immediate cessation of its operations and activities, which may continue for several years. In such situations, some people question the merits of an immediate change in the basis of accounting, with a transition from a “going concern basis of accounting” to a “liquidation basis of accounting”. Similarly, in cases where, despite the dissolution of the undertaking, there are serious prospects of its operations and activities being taken over by another undertaking that has the capacity to continue said operations and activities and meet its obligations, some question whether the undertaking in liquidation is entitled to maintain the “going concern basis of accounting”, or at least whether it is possible to avoid making all the adjustments normally required in connection with the implementation of a “liquidation basis of accounting”.

Without taking a specific position on the foregoing, CNC notes that, as the legislation currently stands, the administrative or management body of an undertaking in a situation of discontinuity of operations, or the liquidator of an undertaking in liquidation, have a degree of flexibility in formulating the principles, policies and methods of a “liquidation basis of accounting”. The specific situation of the undertaking may therefore be taken into account in determining the nature and extent of the adjustments made when the basis of accounting is changed. In this respect, it is clearly important that the notes to the annual accounts explicitly present the accounting principles, policies and methods used and that they mention – where applicable – the reasons that led to adapting or even deferring the implementation of a “liquidation basis of accounting”.

When the discontinuity of operations is motivated by economic factors or even by the failure of the undertaking and that this situation is likely to result in losses for third-party creditors or even for shareholders, CNC is of the opinion that the implementation of a “liquidation basis of accounting” as described below is the only option available.

In view of the information and protection objectives assigned to accounting law, it is important, when an undertaking finds itself in a situation of discontinuity of operations, to be able to estimate as quickly as possible the potential losses to be suffered by third party creditors or even by the shareholders of the failing undertaking.

In this context, it is advisable to anticipate as far as possible the recognition of all expenses that the undertaking will incur up to the close of its liquidation, regardless of the usual principle of independence or separation of financial years. In the context of a “going concern basis of accounting”, this principle would prohibit the recognition of expenses relating to subsequent financial years and their counterpart on the balance sheet (e.g. debts, accrued expenses, provisions).

As a result, the liquidation basis of accounting focuses on estimating the undertaking’s “final” financial position by drawing up an “inclusive” balance sheet that includes all the liabilities owed by the undertaking, regardless of the financial year / accounting period to which they relate27. In this sense, the profit and loss account of the discontinuing or liquidating undertaking is often of lesser importance, as the principle of annuality of charges no longer applies, making it pointless to compare the results or even the performance of the undertaking from one financial year to the next28.

It should also be noted that – in addition to the derogation from the principle of independence or separation of financial years / accounting periods – the implementation of a liquidation basis of accounting also implies an adjusted application of the principle of prudence in its “realisation of profits” (art. 51 (1) c) aa) LRCS), “recognition of liabilities” (art. 51 (1) c) bb) LRCS) and “recognition of depreciation / amortisation” (art. 51 (1) c) cc) LRCS) aspects, as highlighted below.

Under the “going concern basis of accounting” under LUX GAAP and LUX GAAP-FV, not all assets can be recognised in the balance sheet (e.g. goodwill created by the undertaking). Under LUX GAAP, the valuation / measurement of assets is mainly based on the historical cost method (purchase price or production cost) or on a valuation / measurement at a lower value, for example in the case of limited useful economic life (art. 55 (1) b) LRCS) or permanent / durable loss in value (art. 55 (1) c) LRCS). Under the LUX GAAP – FV regime29, the derogatory valuation / measurement of certain eligible assets (e.g. derivative financial instruments, investment property30) by reference to fair value becomes possible (option) pursuant to section 7bis of Chapter II of Title II LRCS.

Under the “liquidation basis of accounting” (LUX GAAP or LUX GAAP-FV regimes), the principle of prudence continues to apply, but with a different meaning and scope from those usually applied under the “going concern basis of accounting”. Thus, certain assets previously recognised by the undertaking on a going concern basis, but which cannot be realised / sold as part of the liquidation process, must be immediately removed / written off from the balance sheet. By way of illustration, this applies to “formation expenses”31 that the undertaking would have chosen to capitalise in application of Article 53 LRCS but which constitute “non-values” i.e. worthless in the context of a liquidation. The same could apply to certain previously capitalised “development costs”. On the other hand, it would appear possible – in a “liquidation basis of accounting” – to present assets on the balance sheet that the undertaking had not previously recognised, provided that their disposal or use to settle / reimburse liabilities is highly probable32. For example, this could be the case for certain intangible assets created by the undertaking itself (e.g. components of goodwill). Similarly, if the principle of the independence or separation of financial years / accounting periods and, more generally, the principle of the annuality of income and expenses (art. 51 (1) d) LRCS) is called into question, an undertaking that is in a situation of discontinuity of operations or is being wound up has to recognise an estimate of accrued income (e.g. operating income, financial income) until the close of the liquidation, even if this income relates to a subsequent financial year. This results in the recognition of receivables on the assets side of the balance sheet in the form of “accrued income”. It should be noted that this accrued income is generally not taxed in the year in which it is recognised, as taxation is generally deferred until the financial year to which the income relates. Consequently, the early recognition of estimated future income will require – where appropriate – the recognition of provisions for deferred tax (liabilities).

With regard to the valuation / measurement of assets recognised in the balance sheet, the need for the liquidator to estimate as accurately as possible the value of realisable assets that are available with a view to settling / reimbursing liabilities generally justifies giving up / moving away from the principle of valuation / measurement at historical acquisition cost and replacing it with valuation at “probable realisable value”. Although not defined under LUX GAAP and LUX GAAP-FV, the concept of probable realisable value, which is well known to accounting professionals, is commonly interpreted as corresponding to the estimated selling price of an asset less the costs necessary to make the sale33.

In estimating the probable realisable value, the undertaking must take into account, where appropriate, the urgent nature of the sale (emergency sale as opposed to a sale in the ordinary course of activity). This use of the probable realisable value will be accompanied, where applicable, by the recognition of unrealised income which – when realised – will generally become subject to taxation. In this context, and by analogy with the recognition of estimated future income (see above), the undertaking will have to recognise provisions for deferred tax liabilities.

The issue of early recognition of estimated future income and unrealised income in connection with the valuation / measurement of realisable assets by reference to their probable realisable value also raises the question of the distributable nature of these unrealised results. In this respect, the principle of prudence in its “realisation of profits” aspect (art. 51 (1) c) aa) LRCS) as well as the principle of non-distribution of unrealised income and gains (art. 72ter) LRCS) seem to prohibit such distribution by undertakings in a situation of discontinuity of operations to which general accounting law continues to apply prior to their liquidation. On the other hand, in the case of undertakings which have already gone into liquidation and to which general accounting law no longer applies in accordance with usual practice (see point 1.1.), it is up to the liquidator to determine – in the absence of any legal provisions – whether or not said income and unrealised gains are distributable. In this context, liquidators are advised to exercise the utmost caution.

In addition, it also follows from the above points (valuation / measurement of assets at probable realisable value) that in “liquidation basis of accounting”, depreciation / amortisation plans for fixed assets with a limited useful economic life are generally discontinued. In principle, fixed assets are also transferred to the current assets category in order to reflect the non-durable nature of their holding (residual life less than or equal to one year). In the case of undertakings in liquidation, which can dispense with the formalities associated with the use of the standard balance sheet layout (art. 34 LRCS), captions and sub-captions may be created specifically for this purpose (e.g. non-current assets held for sale). For undertakings in a situation of discontinuity of operations but not yet formally put into liquidation, the application of the balance sheet layout provided by general accounting law (art. 34 LRCS) may make it difficult to reclassify certain fixed assets as current assets (e.g. tangible fixed assets). In such cases, and in the absence of a reclassification from fixed assets to current assets, appropriate information must be provided in the notes to the annual accounts.

Finally, it should be noted that the probable realisable value of an asset cannot always be determined with a sufficient degree of reliability (e.g. unlisted equity investments). In such cases, and bearing in mind the need for prudence, the asset may be maintained at its net book value34.

In summary, and in view of the objectives associated with an accounting representation in a context of discontinuity of operations or liquidation, it is clearly important to avoid overstating the amount of assets to be realised / sold. Such an overstatement could distort the assessment of the undertaking’s real / actual ability to reimburse / pay off its liabilities. While it is also undesirable to underestimate the amount of assets to be realised / sold, the risks associated with doing so appear to be lower.

Under the “going concern basis of accounting” under LUX GAAP and LUX GAAP-FV, not all liabilities can be recognised; only liabilities that arose during the financial year or a previous financial year can be taken into account (art. 51 (1) c) bb) LRCS and art. 51 (1) bis LRCS). As a result, certain liabilities are relegated to off-balance sheet commitments (e.g. rental payments under a property or equipment leasing contract but relating to a period of occupancy or use subsequent to the balance sheet date).

Liabilities that can be recognised in the balance sheet on a going concern basis of accounting35 are generally valued / measured under LUX GAAP on the basis of the redemption value of the debt, the amount required to settle the debt or the best estimate of the probable amount of the accrued liability. Under the LUX GAAP – FV regime, the derogatory valuation / measurement of certain eligible liabilities (e.g. derivative financial instruments) by reference to fair value becomes possible (option) in application of section 7bis of Chapter II of Title II LRCS.

Under the “liquidation basis of accounting” (LUX GAAP or LUX GAAP-FV regimes), the principle of prudence continues to apply, but with a different meaning and scope from those usually applied under the “going concern basis of accounting”. An inclusive approach is adopted for the recognition of liabilities. All liabilities to be settled / reimbursed by the undertaking prior to the close of liquidation must in principle be recognised in the balance sheet, whether they arose during the financial year or a previous financial year, or whether they relate to a subsequent financial year.

This challenge to the principle of the independence or separation of financial years / accounting periods and, more generally, to the principle of the annuality of income and expenses (art. 51 (1) d) LRCS) leads the undertaking in a situation of discontinuity of operations or liquidation to recognise an estimate of future expenses to be incurred (e.g. staff costs, rent / lease for movable and immovable property, interest on financing, penalties and contractual compensation / indemnities, etc.) until the close of the liquidation, even if these expenses relate to a subsequent financial year. These “future expenses to be paid” may be shown on the balance sheet under “provisions” to distinguish them from “debts / creditors” corresponding to liabilities that arose during the financial year or a previous financial year. It should be noted that these accrued expenses are generally subject to a tax deduction in the year to which they relate, regardless of when they are recognised. The early recognition of estimated future expenses may therefore require the recognition of deferred tax assets.

In view of the fact that an undertaking that is in a situation of discontinuity of its operations or is being liquidated may extinguish debts entered on the liabilities side of its balance sheet, the utmost caution should be exercised. While the extinguishment of liabilities does not raise any particular problems when the undertaking has been legally released from its payment or repayment obligation, the situation is different in other situations. For example, it is important that the undertaking does not imprudently or prematurely anticipate the fact that it may be released from its obligation as principal debtor, for example when a third party has guaranteed its obligation. At the very least, it is important that such a reversal should only take place when it appears highly likely that the undertaking will be released from the settlement / reimbursement of the debt in question.

The valuation / measurement of liabilities recognised in the balance sheet under the “liquidation basis of accounting” is generally based on the best estimate of the probable amount to be paid to settle / reimburse the liabilities. In this respect, the abandonment of the principle of independence or separation of financial years / accounting periods makes it possible to take into account, in the valuation / measurement of liabilities to be settled / reimbursed, the estimated future expenses that will have to be incurred in order to extinguish said liabilities (e.g. interest or penalties due in the event of early termination of financing contracts, damages and compensation due in the event of early termination of service contracts, staff redundancy payments, etc.). In estimating the probable amount to be paid to extinguish the liability, the undertaking may take into account the state of negotiations with its third-party creditors, provided that the outcome of these negotiations is highly probable. In case of doubt, prudence in the valuation / measurement of the related liabilities should be favoured.

Furthermore, in a “liquidation basis of accounting”, all liabilities are in principle reclassified as current liabilities (residual term less than or equal to one year). In the case of undertakings in liquidation, which may dispense with the formalities associated with the use of the general law balance sheet layout (art. 34 LRCS), captions and sub-captions may be created specifically for this purpose. For undertakings in a situation of discontinuity of operations but not yet formally placed in liquidation, the application of the general law balance sheet layout (art. 34 LRCS) allows a reclassification of the items of “C. Creditors” from the “more than one year” captions36 to the “less than one year” captions37. However, the reclassification of certain estimated future liabilities may be more difficult. For example, some undertakings may prefer to keep the estimate of future accrued expenses under “B. Provisions” rather than under one of the captions under “C. Creditors”. In such cases, and in the absence of an explicit reclassification to liabilities with a residual maturity of less than or equal to one year, appropriate information may or even should be provided in the notes to the annual accounts (e.g. details of the contents of caption “B. Provisions” mentioning – as far as possible – the probable disbursement period).

In summary, and in view of the objectives associated with the accounting representation in a context of discontinuity of operations or liquidation, it is clearly important to avoid underestimating the amount of liabilities to be settled / reimbursed. Such an understatement would risk distorting the assessment of the level of losses potentially incurred by third-party creditors and by the shareholders. While an overstatement of the amount of liabilities to be settled / reimbursed is not desirable either, the risks associated with such an overstatement appear to be nonetheless lower.

Undertakings in a situation of discontinuity of operations remain – prior to their liquidation – subject to general accounting law. The obligation to draw up annual accounts within the meaning of article 26 (1) LRCS including at least the balance sheet, the profit and loss account and the notes to the annual accounts therefore remains applicable38.

In this respect, and in the same way as an undertaking in a situation of going concern, the notes are obviously an integral part of the annual accounts drawn up by such an undertaking, as the information included therein is of key importance with regard to the objective of a true and fair view from the perspective of protecting third party creditors and shareholders through accounting information.

With regard to the content of the notes to the annual accounts, the information required under article 65 (1) LRCS and other provisions of Chapter II of Title II LRCS apply, where applicable, within the limits relating to the size category (small, medium-sized, large)39 to which the undertaking belongs. In addition, and in accordance with the general principle, any other significant information contributing to the objective of a true and fair view must be provided (art. 26 (4) LRCS). By way of illustration, this could be the case for the mention of “significant events subsequent to the balance sheet date” (art. 65 (1) 18° LRCS), from which small undertakings are in principle exempt (art. 66 LRCS) but the inclusion of which could be made necessary by the overriding objective of a true and fair view (art. 26 (3) and (4) LRCS)40.

In view of the exceptional situation of an undertaking in discontinuity of operations, the objective of a true and fair view also requires the addition of information that is not explicitly provided for under general accounting law (see below).

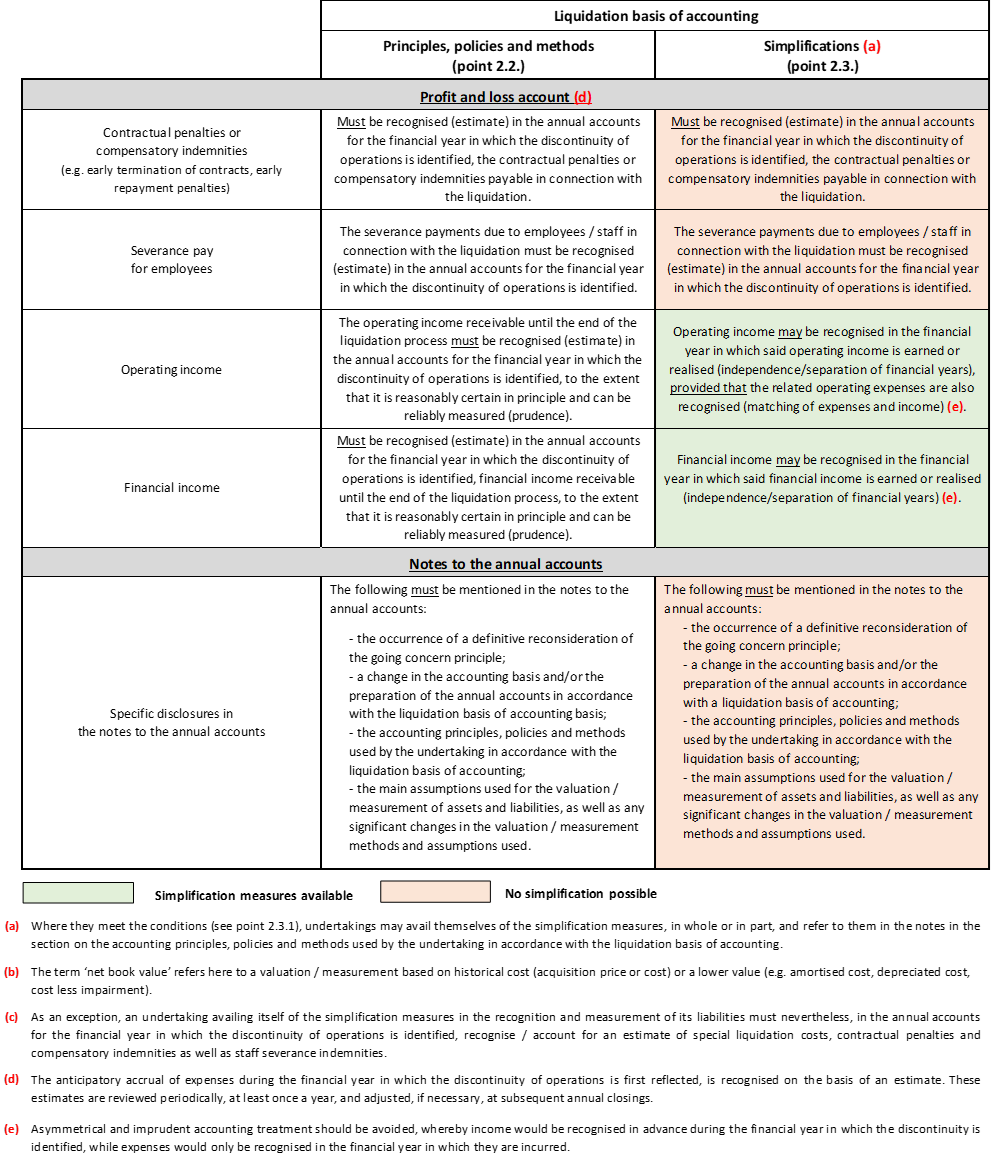

Among the disclosures in the notes that help to achieve the objective of a true and fair view, CNC considers that, at a minimum, specific mention should be made of the following items:

In the case of an undertaking in a situation of discontinuity of operations – after it has been put into liquidation – it has been established that, in accordance with general practice (see point 1.1.), general accounting law (Title II LRCS) ceases to apply to the undertaking in liquidation and is replaced by the accounting provisions of Title XI LSC (special accounting law).

CNC has already indicated that the special accounting law (Title XI LSC) applicable to undertakings in liquidation is fragmentary and even incomplete (see point 1.1.). However, pursuant to Article 1100-14 LSC, an undertaking in liquidation must continue to draw up annual accounts, generally referred to as “annual / interim liquidation accounts”, for the duration of its liquidation (see point 1.2.). However, the content and format of these annual / interim liquidation accounts are not specified by Title XI LSC.

In this respect, it is common practice for annual / interim liquidation accounts to include not only a balance sheet and profit and loss account presenting the results of the liquidation, but also explanatory notes41. Although the undertaking in liquidation may dispense with the formalities associated with the application of general accounting law (see: exemption from the information required by Article 65 (1) LRCS), CNC nevertheless considers that it is important for the undertaking in liquidation to include at least the specific information listed above in its notes. Over and above the objective of a true and fair view42, it is the principle of good information that requires at least the inclusion of such information in the notes to the accounts, as this will help the liquidator to meet his reporting obligations to the general meeting.

The table below (see Fig. D) summarises the principles, policies and methods of “liquidation basis of accounting” for the various balance sheet and profit and loss account captions and for the notes to the accounts.

When the discontinuity of operations is not motivated by economic factors or by the failure of the undertaking and is not likely to result in losses for third-party creditors or shareholders, CNC considers that the implementation of proportionate “liquidation basis of accounting” principles, policies and methods, incorporating simplification measures, is sometimes appropriate43 or even adequate44.

It is proposed to:

CNC is of the opinion that the implementation of simplification measures within the “liquidation basis of accounting” is only conceivable in cases where the discontinuity of operations and liquidation are expected – with reasonable certainty – not to result in losses for the undertaking’s creditors or even for its shareholders and where, consequently, all of the undertaking’s liabilities will be settled / reimbursed and no stakeholders will be adversely impacted. As a general rule, such a situation will only arise in cases where the discontinuity of operations is the result of management decisions taken at the level of the undertaking (e.g.: voluntary cessation of activity, sale of the business / activities, extinction of the corporate purpose, etc.) or at the level of the group to which it belongs (e.g.: intra-group reorganisation, transfer and/or relocation of activities, etc.). In such cases, the undertaking in a situation of discontinuity of operations remains solvent and liquid.

In the situations described above, it can be validly argued that the implementation of a “liquidation basis of accounting” as described above (see point 2.2.) is not fully justified. In fact, the “inclusive” and “anticipatory” approach implemented in the context of the liquidation basis of accounting only makes full sense in a situation where losses are foreseeable and where it is expected that third-party creditors or even shareholders will be adversely impacted.

In view of the foregoing, it may sometimes be possible or even appropriate to adapt the principles, policies and methods of the “liquidation basis of accounting” to reflect the specific conditions and circumstances of undertakings other than those in economic difficulty or in default. In this respect, it should be noted that, as the legislation currently stands and in the absence of a legislative articulation of principles, policies and methods for the “liquidation basis of accounting” (see point 2.1.), it is up to the administrative or management body or to the liquidator to articulate the principles, policies and methods of the “liquidation basis of accounting”. In the absence of legal provisions, the latter clearly have a certain amount of flexibility. However, this flexibility is limited by the responsibility of the administrative or management body or of the liquidator towards the shareholders and other stakeholders of the undertaking. As a result, caution is advisable.

The following decision tree (see Fig. E) is intended to help undertakings determine the appropriate basis of accounting and whether simplification measures should be applied.

In cases where the undertaking can validly rely on simplification measures in the implementation of the “liquidation basis of accounting” (see point 2.3.1.), the question naturally arises as to the nature, scope and extent of these simplification measures.

Firstly, CNC considers that the principles, policies and methods of the “liquidation basis of accounting” as described above (see point 2.2.) are the general rule in the event of discontinuity of operations or of liquidation. Consequently, the implementation of simplification measures constitutes a derogatory and optional regime which the undertaking – when it fulfils the conditions (see point 2.3.1.) – may use in whole or in part.

While it is conceivable that the undertaking may only take advantage of certain simplification measures, it must nevertheless ensure overall consistency and exercise caution. In this respect, asymmetrical accounting treatment, whereby income is recognised in advance in the financial year in which the discontinuity of operations is identified, while expenses are only recognised in the financial year in which they are incurred, should be avoided (see Fig. F).

Valuing / measuring assets by reference to their probable realisable value can be tricky for undertakings that are ceasing operations or going into liquidation. In many cases, there is no market for the asset in question, or only a very limited market. In these situations, assessing the net selling price of the asset involves a significant estimation exercise and requires a high degree of professional judgement.

In order to avoid this delicate exercise, which is of limited use when the solvency and liquidity of the undertaking are not in question, it seems possible to value / measure assets at net book value, generally at historical cost or at a lower value45. However, it is up to the undertaking to ensure that this valuation / measurement of assets remains prudent, i.e. that it does not exceed the price at which the undertaking believes it will be able to realise / sell the assets in question.

In practice, this derogatory valuation / measurement will mainly apply to fixed assets, including fixed tangible and intangible assets with a limited useful economic life and financial fixed assets.

With regard to the recognition of income, the undertaking may continue to apply the principle of independence or separation of financial years and, more generally, the principle of annuality of income and expenses (art. 51 (1) d) LRCS). In such a case, an undertaking that is in a situation of discontinuity of operations or that is going into liquidation does not recognise an estimate of accrued income46 that relates to a subsequent financial year until the close of the liquidation.

The application by the undertaking of these simplification measures also has the effect of eliminating – partially or totally – the need to recognise deferred tax (liabilities) in the absence of recognition of unrealised gains47 or of income relating to subsequent financial years (see point 2.2.2.).

Drawing up an inclusive balance sheet including all liabilities due until the close of liquidation, regardless of the principle of separation or independence of financial years, involves a significant estimation exercise concerning in particular the duration of the liquidation procedure and the outcome of negotiations with third parties (e.g. breach of lease, termination of financing contract, etc.).

While such an estimate is justified when the discontinuity of operations or the liquidation is likely to generate losses for third-party creditors or even for shareholders, the situation is different when the solvency and liquidity of the undertaking are not in question and there is no doubt that the liabilities will be settled / reimbursed in full ahead of the close of the liquidation.

In such cases, the undertaking may be able to maintain the application of the principle of independence or separation of financial years and, more generally, the principle of annuality of income and expenses (art. 51 (1) d) LRCS) by recognising only:

In practice, the main effect of this simplification measure is that the undertaking does not have to recognise overheads and other operating expenses, as well as interest and similar charges relating to future periods. The absence of early recognition of certain accrued expenses relating to future periods also has the effect of limiting the situations in which recognition of deferred tax assets is necessary (see point 2.2.3.).

However, an undertaking that takes advantage of the simplification measures in the recognition and measurement of its liabilities must nevertheless – in the annual accounts for the financial year in which the discontinuity of operations occurs and is reflected accounting-wise – recognise an estimate of the specific liquidation costs, contractual penalties and indemnities and staff redundancy payments.

Finally, it should be noted that if the undertaking continues to apply the principle of independence or separation of financial years / accounting periods, it is important to ensure that expenses are linked to or matched with income. An asymmetrical accounting treatment is therefore prohibited, whereby income is recognised in advance (see point 2.2.2.) while expenses are only recognised in the financial year in which they are incurred. Apart from the lack of overall consistency, such an accounting treatment would not be prudent and would in essence generate fictitious profits.

The table below (see Fig. F) summarises, for the various balance sheet and profit and loss account captions and for the notes to the accounts, the simplification measures available in connection with the implementation of the “liquidation basis of accounting” for those undertakings that can avail themselves of them (see Fig. E.)

The occurrence of a going concern and the implementation of a liquidation basis of accounting refer to various accounting issues that are directly or indirectly associated with them. The following section covers some of these issues with a view to clarifying them.

Despite the silence of the law, CNC is of the opinion that the administrative or management body of the undertaking has an obligation to make an assessment of the undertaking’s ability to continue as a going concern. Far from being just one principle among others, the going concern assumption is in fact the central convention underlying the preparation of annual accounts under LUX GAAP and LUX GAAP-FV and it is therefore necessary to ensure that it is appropriate. In line with international practice, CNC considers that this assessment should cover at least, but not be limited to, a period of twelve months from the balance sheet date. In this context, the administrative or management body may rely on financial, operational or other indicators which, taken individually or as a whole, lead to the conclusion as to whether or not the going concern assumption is appropriate. If the analysis leads to the conclusion that the undertaking does not have the ability to continue as a going concern in the foreseeable future50, the going concern assumption must be abandoned and the liquidation basis of accounting must be implemented. In the interest of prudence, CNC notes that it would seem preferable for the liquidation basis of accounting to be applied as soon as the discontinuity of operations is established, whether the events and conditions that led to this conclusion arose during the financial year or after the end of the financial year but before the annual accounts are closed.

Under the LUX GAAP and LUX GAAP-FV regimes, annual accounts are in principle prepared on a going concern basis pursuant to Article 51 (1) a) LRCS, which states that “an undertaking is presumed to be carrying on its business as a going concern“. The preparatory work specifies in this respect that “[i]n accordance with this principle, the annual accounts of a company are those of an undertaking which will continue its operations in the foreseeable future. The valuation / measurement of assets and their depreciation / amortisation according to their useful economic life are based on this principle. The annual accounts are therefore not those of an undertaking in liquidation“51.

Although there is no explicit provision in Luxembourg accounting law requiring the administrative or management body to make an assessment of the undertaking’s ability to continue as a going concern, it is generally accepted that such an assessment is required52/53.

Since the going concern assumption is the foundation on which the accounting framework is based in order to articulate the general principles and the valuation / measurement bases used to prepare the annual accounts, the application of this assumption necessarily presupposes an analysis of whether or not it is appropriate. Far from being just another principle, the going concern assumption is the central convention underlying the preparation of annual accounts under LUX GAAP and LUX GAAP-FV.

Assessing an undertaking’s ability to continue as a going concern necessarily involves judgement about the outcome of events or situations that are inherently uncertain. Although the LUX GAAP and LUX GAAP-FV accounting regimes are silent as to the time horizon to be taken into consideration, CNC believes that it is appropriate to refer to the solution adopted under the IFRS-EU regime, which corresponds to generally accepted practices in the area of financial reporting and auditing. In this respect, IAS 1 states that “[t]o assess whether the going concern assumption is appropriate, management considers all available information about the future, which is at least, but is not limited to, twelve months from the balance sheet date“54.

With the exception of situations where the decision to liquidate has already been taken by the undertaking’s governing bodies and the discontinuity of operations has been formally noted, the acknowledgement that the going concern principle is being called into question generally requires the exercise of judgement by the administrative or management body. This judgement may be based on financial, operational or other indicators which, taken individually or as a whole, lead to the conclusion that there is no realistic alternative for the administrative or management body other than to liquidate the undertaking or to cease operations.

By way of illustration, but not exhaustively, the following indicators may be considered:

Financial indicators:

Operational indicators:

Other indicators:

If, at the end of its analysis, the administrative or management body concludes that the undertaking does not have the capacity to continue as a going concern in the foreseeable future, the going concern assumption cannot be maintained and the implementation of a liquidation basis of accounting becomes inevitable.

When the events and conditions that led to the going concern assumption being definitively called into question arose during the financial year or a previous financial year, it seems clear that the annual accounts for that financial year must reflect the discontinuity of operations and that the liquidation basis of accounting must then be implemented.

However, the question of the date of implementation of the liquidation basis of accounting has arisen in cases where the events and conditions that led to the definitive questioning of the going concern assumption arose after the year-end but before the annual accounts were closed. It should be noted that different positions have emerged on this issue, depending on the accounting framework under consideration.

In this respect, it should be noted that the IFRS-EU regime provides an unequivocal answer on this point. IAS 10 states that “an entity shall not prepare its financial statements on a going concernbasis if management determines after the balance sheet date that it intends, or has no realistic alternative, to liquidate the entity or to cease operations“55.

On the other hand, national frameworks that have been coordinated with the accounting directive 2013/34/EU may have reached a different conclusion, considering that the preparation of annual accounts on a going concern basis is not called into question by events occurring after the end of the financial year and that, in such a situation, these are post-balance sheet events that require appropriate disclosure in the notes to the accounts but which do not yet allow the liquidation basis of accounting to be implemented.

In the Luxembourg context, it is noted that accounting law does not provide an explicit answer concerning the date of implementation of the liquidation basis of accounting when the events and conditions that led to the discontinuity of operations arose after the end of the financial year but before the closing of the annual accounts. In such cases, CNC is of the opinion that prudence nevertheless encourages the use of the liquidation basis of accounting even when the events and conditions that led to the discontinuity of operations arose after year-end. It could appear inappropriate or even misleading to publish annual accounts prepared on a going concern basis to third parties when, at the time of publication, there is no longer any doubt that this assumption cannot be maintained and that liquidation is the only possible outcome.

The change in the basis of accounting56 from the “going concern basis of accounting” to the “liquidation basis of accounting” is made prospectively. The liquidation basis of accounting is implemented for the first time when the annual accounts for the financial year in which the events and conditions that led to the acknowledgement of the discontinuity of operations arose, are prepared. By extension (see point 3.1.), the liquidation basis of accounting is applied for the first time to the annual accounts for the financial year currently being closed when the events and conditions which led to the discontinuity being identified, arose after the end of the financial year but before the accounts were closed. The comparative figures appearing in the first annual accounts prepared on the liquidation basis of accounting are unchanged from the annual accounts for the previous financial year as approved by the competent bodies. The comparative figures are therefore based on the going concern assumption. The lack of comparability must therefore be disclosed and commented on in the notes, together with the change in the basis of accounting and the underlying reasons.

When the going concern assumption cannot be maintained, a change of accounting basis57 must be made and the “liquidation basis of accounting” must be implemented.

This liquidation basis of accounting applies for the first time to the annual accounts for the financial year in which the events and conditions that led to the acknowledgement of the discontinuity of operations arose58. By extension, the “liquidation basis of accounting” also applies to annual accounts in the process of being drawn up when the events and conditions that led to the discontinuity of operations being identified arose after the end of the financial year but before the annual accounts were prepared.

If the financial year of an undertaking for which the discontinuity of operations has just been acknowledged is closed before the undertaking goes into liquidation59, the annual accounts shall be drawn up – with adaptations – in accordance with general accounting law (see point 1.1.) and the balance sheet (art. 34 LRCS) and profit and loss account (art. 46 LRCS) layouts will continue to apply60.

In this respect, it should be noted that the change in the basis of accounting is prospective. As a result, the first set of annual accounts prepared on the liquidation basis of accounting show comparative figures which are unchanged from the annual accounts for the previous financial year as approved by the competent body and which are therefore based on the going concern assumption. In accordance with article 29 (2), 2nd sentence LRCS, the lack of comparability of figures from one financial year to the next must be disclosed in the notes to the accounts and duly commented on.

In cases where an undertaking – for which discontinuity of operations has been previously acknowledged – experiences a return to better fortunes prior to its liquidation61, a change in the basis of accounting is necessary. In this context, CNC is of the opinion that the information provided in the notes to the annual accounts is essential. In this respect, the undertaking must mention the return to the “going concern basis of accounting” by providing explanatory information and specifying the procedures for implementing this change in the basis of accounting. In addition, CNC considers that the reverse transition from the “liquidation basis of accounting” to the “going concern basis of accounting” should follow rules similar to those set out in point 3.2, i.e. prospective application of the new basis of accounting without modification of the annual accounts and comparative figures for previous years. With regard in particular to the valuation / measurement of assets, CNC considers that a return to the initial values generally based on purchase price or production cost is required, with potential revaluations made during previous financial years in order to present assets by reference to their probable realisable value then having to be reversed during the current financial year62.

As a general rule, the discontinuity of operations and the implementation of the “liquidation basis of accounting” result from the acknowledgement that the undertaking is definitively unable to continue as a going concern, and that the administrative or management body intends or has no realistic alternative but to put the undertaking into liquidation or cease operations.

In view of the above, the possibility of a return to better fortunes is generally ruled out at this stage.

Although a return to better fortunes is unlikely once a discontinuity of operations has been acknowledged, it should be noted that such a situation may nevertheless arise. This will be the case, for example, in situations where – subsequent to the acknowledgement of discontinuity – new commercial or financial partnerships emerge and suggest a possible turnaround for the undertaking. In such cases, a return to the “going concern basis of accounting” seems justified. The question then arises as to the accounting implications of a reverse transition from the “liquidation basis of accounting” to the “going concern basis of accounting”.

In this context, the information provided in the notes to the annual accounts is of the utmost importance. In this respect, the undertaking should mention the return to the “going concern basis of accounting”, providing explanatory information and specifying the procedures for implementing this change of accounting basis.

In addition, and in accordance with point 3.2, CNC is of the opinion that the return to the “going concern basis of accounting” should in principle be made on a prospective basis. In other words, if the annual accounts for the previous financial year were drawn up based on a liquidation basis of accounting, the annual accounts for the current financial year drawn up based on a going concern basis of accounting will show comparative figures on a liquidation basis of accounting and will include in the profit and loss account for the financial year the adjustments needed to make the transition in the opposite direction.

In this respect, it should be noted that a return to a valuation / measurement of assets according to the principle of historical cost must generally be made and that any revaluations recognised previously in order to present assets by reference to their probable realisable value must be reversed63. It is not permissible to continue to value / measure assets at a higher book value (probable realisable value) than their initial value (purchase price or production cost price), except in cases where the fair value option is applied to certain eligible assets (LUX GAAP-FV regime).

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Discontinuité d’exploitation et comptabilité en base liquidative en régimes LUX GAAP et LUX GAAP-JV”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible in accordance with general law for any decisions taken based on this document.

1 See: « La Centrale des bilans, un état des lieux décennal » – Analyses 4/2020, Institut national de la statistique et des études économiques.

2 See: Q&A CNC 19/019 “Categorisation of undertakings: interpretation of the repetition criterion referred to in Article 36 LRCS”.

3 N.B.: Without prejudice to more restrictive sector-specific provisions where the task of auditing the accounts at the close of the liquidation is entrusted to the “réviseur d’entreprises agréé” [approved statutory auditor] and where the institution of the “commissaire” [supervisory auditor] is then abolished (e.g.: art. 154 (5) sub-para. 2 of the law of 17 December 2010 concerning undertakings for collective investment).

4 Bill n°2657 adapting the amended law of 10 August 1915 on commercial companies to Directive 78/660 of the Council of the European Communities of 25 July 1978, ordinary session 1982-1983, comments on the articles, article 235, p.42.

5 Title XI “The liquidation of companies” of the amended law of 10 August 1915 on commercial companies.

6 The law of 10 August 1915 on commercial companies was published in the Mémorial of 30 October 1915 (Mém. No. 90).

7 Professor Jean Corbiau, author of the preliminary draft bill of law on commercial companies in 1905, states in the commentary on article 119 (then Article 150 of the law of 10 August 1915 on commercial companies and renumbered Article 1100-14 following the modernisation of company law in 2016 / 2017):

“The obligation to publish the annual liquidation balance sheet imposed on sociétés anonymes also applies, by virtue of article 74 [NDA: then article 103 of the law of 10 August 1915 concerning commercial companies and renumbered article 600-2 following the modernisation of company law in 2016 / 2017], to sociétés en commandite par actions”.

8 Pursuant to article 410-1 para. 2 of the amended law of 10 August 1915 on commercial companies “The société européenne (SE) is a société anonyme (…). (…). It shall be governed by the provisions of the present law applicable to sociétés anonymes (…)”.

9 Private limited liability companies / “Sociétés à responsabilité limitée” (S.à r.l.) are the legal form most commonly used by Luxembourg undertakings: 57.6% of structured filings of financial information over the period 2011-2018 were made by S.à r.l.’s.

Source: « La Centrale des bilans, un état des lieux décennal » – Analyses 4/2020, Institut national de la statistique et des études économiques.

10 The obligation to publish accounts also applies to “sociétés par actions simplifiées”, to “sociétés cooperatives” and – in certain cases – to “sociétés en nom collectif” and to “sociétés en commandite simple” (art. 77, 2nd sub-para. point 2° LRCS).

11 On the other hand, all undertakings in liquidation are, by assumption, in a situation of discontinuity of operations. In this sense, undertakings in liquidation are a subset of undertakings which are in a situation of discontinuity of operations.

12 Article 26 (5) LRCS states that “[w]here in exceptional cases the application of a provision of this Chapter is incompatible with the obligation laid down in paragraph (3) above [A/N: the objective of a true and fair view], that provision must be derogated from in order to give a true and fair view within the meaning of paragraph (3). Any such derogation must be disclosed in the notes to the accounts together with an explanation of the reasons for it and a statement of its effect on the assets, liabilities, financial position and results”.

13 Article 51 (2) LRCS provides that “[w]here in exceptional cases the application of a provision of this law is incompatible with the obligation laid down in Article 26, paragraph (3) [A/N: the objective of a true and fair view], that provision shall be disapplied in order to give a true and fair view of the undertaking’s assets, liabilities, financial position and profit or loss. The disapplication of any such a provision shall be disclosed in the notes to the accounts together with an explanation of the reasons for it and of its effect on the undertaking’s assets, liabilities, financial position and profit or loss”.

14 Title I “Bankruptcy” of Book III “Bankruptcy and suspension of payments” of the Commercial code.

15 Title XII “Judicial dissolution and closure of commercial companies” of the amended law of 10 August 1915 on commercial companies.

16 Grand-Ducal Decree of 24 May 1935 supplementing the legislation relating to suspension of payments, composition with creditors to prevent bankruptcy and bankruptcy by introducing a system of controlled management.

17 The immediate and full takeover by the sole shareholder of all the assets and liabilities of the dissolved undertaking does not generally justify the use of the liquidation basis of accounting.

18 On a voluntary basis or at the request of a stakeholder (e.g. notary, supervisory authority), a contractual audit of the initial liquidation accounts is sometimes carried out. In the case of public interest entities and undertakings subject to prudential supervision and covered by general accounting law, the supervisory authority may require the initial liquidation accounts to be audited by a “réviseur d’entreprises agréé” [approved statutory auditor].

19 As an indication, undertakings may refer to the usual deadlines for submitting the annual accounts to the general meeting in a going concern period, i.e. a period of 6 months from the end of the financial year (e.g.: art. 1500-2 point 2° LSC).

20 SA’s, SE’s and S.e.C.A.’s in liquidation may (but are not obliged to) file their annual / interim liquidation accounts (balance sheet, profit and loss account, notes and – where applicable – the liquidator’s report) with the RCS.

21 In current practice, legal forms other than SA, SE and S.e.C.A. – when they are in liquidation – do not have the option of voluntarily filing their annual / interim liquidation accounts, or even their balance sheet, with the RCS.

22 Certain sector-specific laws provide that the task of controlling the closing liquidation accounts must be entrusted to the “réviseur d’entreprises agréé” [approved statutory auditor]. In such cases, the institution of the “commissaire” is abolished. By way of example, this is the case for the following entities:

– undertakings for collective investment (UCI) [art. 154 (5) 2nd sub-para. L. mod. 17/12/2010],

– specialised investment funds (SIF) [art. 55 (5) 2nd sub-para. L. mod. 13/02/2007],