UNOFFICIAL TRANSLATION

The law and the grand-ducal regulation of 18 December 20151,2 transposing the accounting directive 2013/34/EU has removed – as from financial years beginning on 1stJanuary 2016 – the option to capitalise research costs while maintaining the option to capitalise development costs.

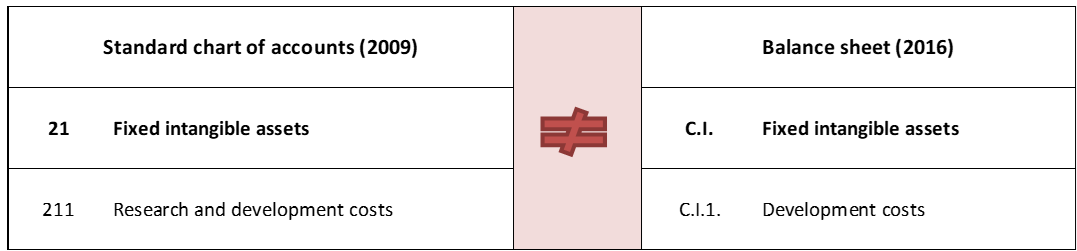

At the same time, the content and presentation of the Standard chart of accounts (PCN) have remained – at this stage – those determined by the Grand Ducal regulation of 10 June 20093 which includes in its section 22 “Intangible fixed assets” an account 211 entitled “Research and development costs”.

The elimination of the option to capitalise research costs, the continuation of the option to capitalise development costs, the resulting change in the balance sheet presentation layout and its disconnect from the content and presentation of the PCN currently in force raise a number of practical issues:

The purpose of Directive 2013/34/EU, which repeals and replaces the 4th and 7th Directives of 19784 and 19835, is to modernise certain accounting provisions by bringing them in line with modern accounting terminology and practices.

In this context, it was noted that IFRS as adopted by the European Union do not allow research costs to be capitalised. IAS 386 stipulates that research costs must be expensed directly in the period in which they are incurred. It has also been pointed out that this accounting treatment of research costs – as adopted by IFRS – contributes to a more prudent representation of the assets recognised in the undertaking’s balance sheet.

Therefore, considering that the principle of prudence is a founding pillar of the accounting directives contributing to the objective of third-party creditors’ protection, the Accounting Directive 2013/34/EU has brought about convergence on this point with IFRS accounting standards by removing the option of capitalising research costs.

As a result, the option to capitalise research costs has been removed from Luxembourg accounting law as part of the transposition of Directive 2013/34/EU and the coordination of national accounting law with European accounting law.

As a result of bringing the balance sheet layout (2016) in line with Directive 2013/34/EU, the balance sheet caption C.I.1. previously entitled “C.I.1. Research and development costs” (2015) has now been renamed “C.I.1. Development costs” (2016) following the removal of the option to capitalise research costs.

The Standard chart of accounts (2009) remains unchanged until the completion of the revision project initiated in 2015, which should be concluded shortly. Consequently, the title of account 211 remains – at this stage – “Research and development costs”.

In this context, the question naturally arises of how to manage this disconnect between the title of the balance sheet caption “C.I.1. Development costs” and of the PCN account “211 Research and development costs”.

In this respect, two distinct approaches appear possible, one based on the connection (point 2.1.) between the PCN 211 account and the balance sheet caption C.I.1. and the other based on the disconnection (point 2.2.).

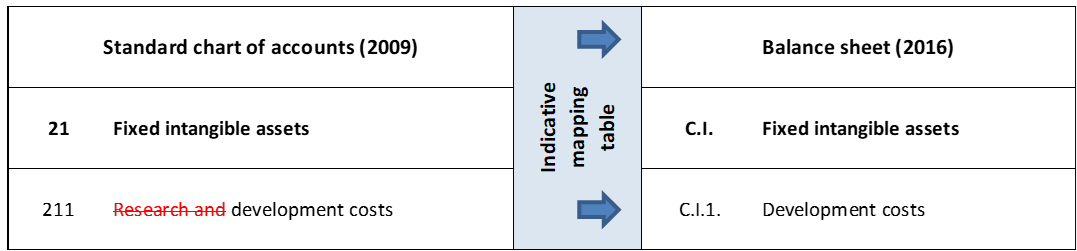

A first possible approach is to align the content of the PCN 211 account with that of the C.I.1 balance sheet caption.

This approach has the advantage of facilitating the mapping between the trial balance presented in accordance with the PCN and the balance sheet drawn up in accordance with a layout that complies with Directive 2013/34/EU.

In practice, this approach consists – if the capitalisation option under article 59 of the LRCS is exercised, which is an option and not an obligation – of recognising only development costs in the PCN 211 account, while research costs are recognised as expenses of the financial year.

A second possible approach is based on the disconnection between the content of PCN account 211 entitled “Research and development costs” and that of balance sheet caption C.I.1. entitled “Development costs”.

Under this approach, undertakings may continue – in view of the title of the 211 PCN account – to post research costs incurred after 1 January 2016 to the 211 PCN account. However, these research costs booked to the 211 PCN account may not – in accordance with European accounting law – appear on the assets side of the balance sheet, which means that – when the balance sheet is drawn up – the research costs booked to the 211 PCN account must be reclassified as expenses of the financial year.

This approach has the disadvantage of requiring a reconciliation between the trial balance of accounts presented in accordance with the PCN and the balance sheet drawn up in accordance with the layout that complies with Directive 2013/34/EU.

In view of the above, CNC notes that two approaches appear possible based on the texts as they currently stand: an approach based on connection (point 2.1.) and an approach based on disconnection (point 2.2.).

Without prejudice to the choices made by the administrative or management bodies of undertakings, the Accounting standards board (CNC) notes that the connection-based approach (point 2.1.) appears preferable both for preparers of accounts (e.g. natural mapping between the PCN and the balance sheet, absence of reconciliation between the trial balance of accounts and the balance sheet) and for public-sector users (e.g. better intelligibility, easier traceability).

Consequently, CNC recommends that the connection-based approach (point 2.1.) be favored, i.e. an approach in which the content of the PCN 211 account is aligned with that of the balance sheet caption C.I.1. (2016).

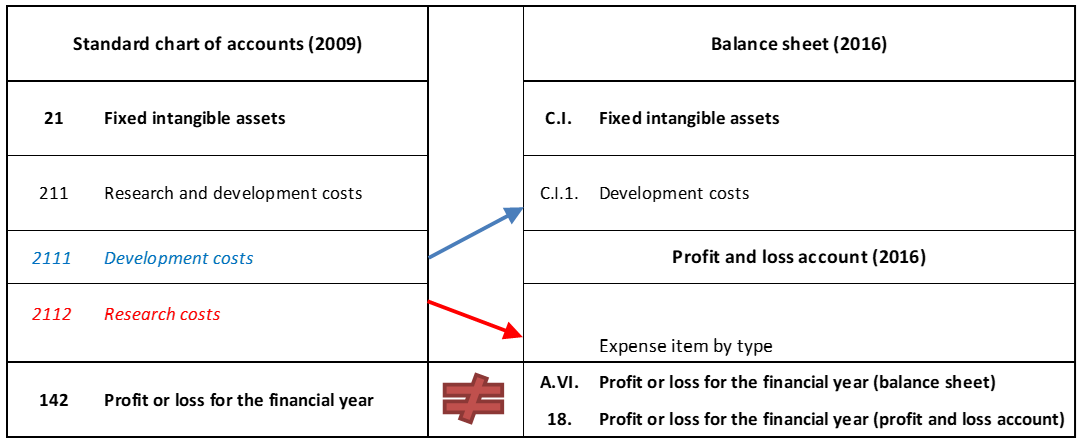

As part of its work on the revision of the PCN, and without prejudging the outcome of the regulatory procedure, CNC has questioned the evolution of the PCN accounts for research and development costs.

Following this reflection, CNC proposes that account 211, currently entitled “Research and development costs”, be changed to account 211 “Development costs”. CNC considers that, wherever possible, an intuitive connection should be made between the PCN accounts and the captions and headings of the balance sheet and profit and loss account.

Other changes should be made, particularly to class 6 accounts, to allow undertakings that do not use the option of capitalising development costs to recognise development costs directly as expenses.

Considering that Luxembourg accounting law now provides a separate regime for research costs on one hand and development costs on the other, the definition of these terms takes on new importance.

However, neither research costs nor development costs have been defined by the Accounting Directive 2013/34/EU. In accordance with the approach generally adopted in Luxembourg for the transposition of directives, research and development costs have not been defined in the general accounting law applicable to Luxembourg undertakings.

Considering the silence of general accounting law, it seems possible to refer to special accounting law, i.e. the IFRS international accounting standards adopted by the European Union, which apply – in Luxembourg – either on a mandatory basis to the consolidated accounts of companies whose securities are admitted to trading on a regulated market of the European Union, or on an optional basis to the annual and consolidated accounts of all undertakings.

In this respect, it should be noted that IAS 38 “Intangible Assets”, as adopted by the European Union, provides useful clarifications for characterising and distinguishing between research and development and the phases and activities related thereto.

IAS 38 provides a definition of research (IAS 38 para. 8) and examples of research activities (IAS 38 para. 56), which are set out below:

IAS 38.8 Research is original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding.

IAS 38.56 Examples of research activities:

(a) activities aimed at obtaining new knowledge;

(b) the search for, evaluation and final selection of, applications of research findings or other knowledge;

(c) the search for alternatives for materials, devices, products, processes, systems or services; and

(d) the formulation, design, evaluation and final selection of possible alternatives for new or improved materials, devices, products, processes, systems or services.

IAS 38 provides a definition of development (IAS 38 para. 8) and examples of development activities (IAS 38 para. 59), which are set out below:

IAS 38.8 Development is the application of research findings or other knowledge to a plan or design for the production of new or substantially improved materials, devices, products, processes, systems or services, before the start of commercial production or use.

IAS 38.59 Examples of development activities:

(a) the design, construction and testing of pre-production or pre-use prototypes and models;

(b) the design of tools, jigs, moulds and dies involving new technology;

(c) the design, construction and operation of a pilot plant that is not of a scale economically feasible for commercial production; and

(d) the design, construction and testing of a chosen alternative for new or improved materials, devices, products, processes, systems or services.

Despite the clarification of the concepts of research and development and the related research and development activities, it should be noted that it is sometimes difficult for an undertaking to distinguish – for a given project7 – between the research phase and the development phase.

In such cases, IAS 38 states that “if an entity cannot distinguish the research phase from the development phase (…), the entity treats the expenditure (…) as if it were incurred in the research phase only” (IAS 38.53). As a result, under IFRS, these expenses are charged directly to the profit and loss account in the period in which they are incurred (IAS 38.54)8.

Following the entry into force of the law and regulation of 18 December 2015 transposing Directive 2013/34/EU, the LUX GAAP regime applicable to research and development costs now has the following characteristics:

5.1. Removal of the capitalisation option for research costs;

5.2. Continuation of the option to capitalise development costs and related valuation / measurement rules;

5.3. The principle of amortisation over the useful life with – by way of exception – amortisation over a maximum fixed period of 10 years;

5.4. The prohibition on profit distribution where development costs have been capitalised but not yet fully amortised unless the amount of available reserves and retained earnings is at least equal to the amount of the unamortised costs;

5.5. Information on development costs in the notes to the accounts.

In accordance with the terms of Directive 2013/34/EU and its transposition into Luxembourg accounting law, undertakings preparing their annual or consolidated accounts under LUX GAAP may no longer capitalise research costs incurred from 1 January 2016, as the option to do so has been removed (see point 1).

As a result, research costs incurred from that date must be expensed directly.

The Luxembourg legislator has maintained the option allowing Member States to authorise the capitalisation of development costs.

As a result, undertakings retain the option – after 1 January 2016 – of capitalising development costs. As this is an option and not an obligation, undertakings are of course free not to capitalise development costs incurred and to recognise them as expenses for the financial year.

With regard to the valuation / measurement rules applicable to development costs, the general accounting law applies as set out in article 52 LRCS9 and article 55 (1) a) LRCS10, i.e. a valuation / measurement based on the purchase price or the production cost.

In addition, insofar as development costs are fixed assets with a limited useful life, they are subject to a systematic amortisation in accordance with article 55 (1) b) LRCS11 (see point 5.3.).

Prior to the entry into force of the law of 18 December 2015, development costs had to be amortised – as a general rule – over a maximum period of 5 years.

As an exception, development costs could be amortised over a longer period if it could be demonstrated that the useful economic life of the development costs was longer. In such cases, the undertaking had to disclose this in the notes to the accounts and justify the period of use in excess of 5 years.

As regards the amortisation period for development costs, the general rule and the exception are now reversed.

Thus, following the entry into force of the law of 18 December 2015, development costs must – in the same way as other intangible assets (art. 59 (1) LRCS)12 – be amortised over their useful economic life.

By way of exception, when the useful life of development costs cannot be reliably estimated, the undertaking amortises development costs over a fixed period which may not exceed 10 years (art. 59 (2) LRCS)13. In this context, the undertaking is free to choose a fixed period of use of less than 10 years14.

In accordance with Directive 2013/34/EU, the Luxembourg legislator has maintained the principle that as long as development costs “have not been completely written off, no distribution of profits shall take place unless the amount of the reserves available for distribution and profits brought forward is at least equal to that of expenses not written off ” (art. 59(3) LRCS)15.

In other words, an undertaking with development costs on the assets side of its balance sheet can only distribute profits if it has reserves in excess of the unamortised amount of the development costs.

As a result, whether or not development costs are capitalised has no effect on the amount of distributable reserves. The main purpose of this provision is to protect third-party creditors against the risks of premature distribution of profits.

Pursuant to Article 65 (1) 1° LRCS, undertakings of all sizes are required to disclose their accounting policies and valuation / measurement methods in the notes to the accounts. In the case of development costs, undertakings must disclose whether the option to capitalise development costs has been exercised and – if so – the useful economic life applied to amortise said development costs.

In addition, undertakings other than the small undertakings referred to in article 35 LRCS are required – pursuant to article 39 (3) LRCS – to disclose in the notes to the accounts the movements (e.g. additions, disposals, transfers, accumulated value adjustments) of the various fixed asset items, including movements relating to development costs “capitalised” as components of fixed intangible assets.

In addition, and in accordance with general accounting principles, if the application of the legal provisions is not sufficient to give the true and fair view referred to in Article 26 (3) LRCS, additional information must be provided in accordance with Article 26 (4) LRCS.

A negative answer is called for.

The fair value option provided for in article 64sexies LRCS16 applies to certain categories of assets other than financial instruments only to the extent that IFRS accounting standards allow these assets to be measured by reference to fair value.

However, in the case of development costs and, more generally, intangible assets, IAS 38 only provides for the cost model and the revaluation model, but not the fair value model.

The revaluation model is distinct from the fair value model, which is not available under either LUX GAAP or LUX GAAP – FV17.

Consequently, it follows from the above that only the amortised cost model provided for in Articles 52 and 55 LRCS is available under LUX GAAP and LUX GAAP – FV for the valuation / measurement of development costs.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Frais de recherche et de développement : nouveau régime comptable applicable (2016)”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible in accordance with general law for any decisions taken based on this document.

1 Law of 18 December 2015 amending, with a view to the transposition of Directive 2013/34/EU of the European Parliament and of the Council of 26 June, 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC: 1) the amended law of 10 August 1915 on commercial companies; 2) Title II of the amended law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings; 3) Title II of Book l of the Commercial Code, Mém. A – N°258 of 28 December 2015.

2 Grand Ducal Regulation of 18 December 2015 determining the form and content of the balance sheet and profit and loss account layouts and implementing Articles 34, 35, 46 and 47 of the amended law of 19 December 2002 on the trade and companies register as well as the bookkeeping and annual accounts of undertakings, Mém. A – N°258 of 28 December 2015.

3 Grand Ducal Regulation of 10 June 2009 determining the content and presentation of a standard chart of accounts, Mém. A – N°145 of 22 June 2009.

4 Fourth Council Directive 78/660/EEC of 25 July 1978 based on Article 54 (3) (g) of the Treaty on the annual accounts of certain types of companies

5 Seventh Council Directive 83/349/EEC of 13 June 1983 based on Article 54 (3) (g) of the Treaty on consolidated accounts

6 Cf. International Accounting Standard 38 Intangible Assets, paragraph 54:

” 54. No intangible asset arising from research (or from the research phase of an internal project) shall be recognised. Expenditure on research (or on the research phase of an internal project) shall be recognized as an expense when it is incurred”.

7 This includes research and development projects whether generated internally by the undertaking or acquired by it separately or as part of a business combination.

8 IAS 38 paragraph 54 states that:

“No intangible asset arising from research (or from the research phase of an internal project) shall be recognised. Expenditure on research (or on the research phase of an internal project) shall be recognised as an expense when it is incurred”.

9 Article 52 of the amended law of 19 December 2002 provides that:

“The items shown in the annual accounts shall be measured in accordance with Articles 53, 55, 56, 59 to 64, which are based on the principle of purchase price or production cost”.

10 Article 55(1) a) of the amended law of 19 December 2002 provides that:

“Fixed assets must be measured at purchase price or production cost, without prejudice to b) and c) below”.

11 Article 55(1) b) of the amended law of 19 December 2002 provides that:

“The purchase price or production cost of fixed assets with limited useful economic lives must be reduced by value adjustments calculated to write off the value of such assets systemically over their useful economic lives”.

12 Article 59 paragraph (1) of the amended law of 19 December 2002 provides that:

“(1) Intangible assets shall be written off over the useful economic life of intangible asset”.

13 Article 59 paragraph (2) of the amended law of 19 December 2002 provides that:

“(2) In exceptional cases where the useful life of goodwill and development costs cannot be reliably estimated, such assets shall be written off within a maximum period which shall not exceed 10 years. An explanation of the period over which goodwill is written off shall be provided within the notes to the accounts”.

14 The legislator has set a maximum fixed period of 10 years for the amortisation of development costs whose useful economic life cannot be reliably estimated. In this context, the undertaking may decide to amortise such development costs over a shorter period of between 1 and 10 years.

15 Article 59 (3) LRCS extends to development coss the application of Article 53 (1) b) LRCS applicable to formation expenses.

16 Article 64sexies of the amended law of 19 December 2002 provides that:

“By way of derogation from Article 52, undertakings may also measure specified categories of assets other than financial instruments at amounts determined by reference to their fair value, provided that their measurement at fair value is authorised under the international accounting standards adopted in accordance with the Regulation (EC) No 1606/2002 of the European Parliament and of the Council on the application of the international accounting standards”.

17 See: Q&A CNC 14/003 Revaluation of fixed intangible assets (formerly Q&A 03/2014)