UNOFFICIAL TRANSLATION

Categorising undertakings and groups: size and repetition criteria

Luxembourg accounting law (DCL) has been built on – since 19841 and the transposition of the 4th Directive 78/660/EEC2 – an approach based on categories3 where the nature and extent of accounting obligations are proportional to the size of undertakings. This approach has been maintained by Directive 2013/34/EU4.

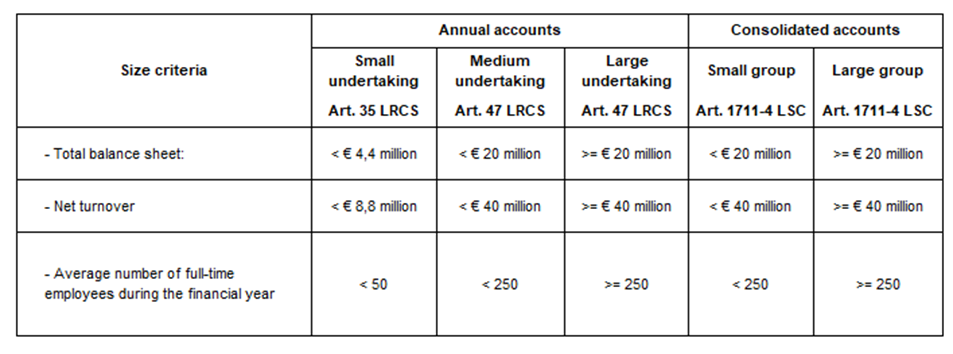

Undertakings are categorised as “small undertakings” (art. 35 LRCS), “medium-sized undertakings” (art. 47 LRCS) and “large undertakings” on the basis of three size criteria, namely “balance sheet total“, “net turnover” and “number of employees”. Similarly, categorisation as a “small group” or as a “large group” (art. 1711-4 LSC) is also based on these three size criteria (considered on a consolidated or an aggregated basis) in order to determine the existence of the legal obligation to draw up and publish consolidated accounts.

For each of these three criteria, specific numerical thresholds are set for each category (see Fig. A below). If at least two of the three criteria are exceeded or not exceeded, the undertaking or group is placed in the higher or lower category.

In addition, in order to “prevent temporary crossings of the thresholds (…) from influencing the preparation of the annual accounts”, it has been stipulated that “if the thresholds (…) are crossed in either direction, this will only have an effect if the crossing occurs during two consecutive financial years“5.

Article 36 paragraph 1 LRCS provides that:

“Where on its balance sheet date an undertaking either exceeds or ceases to exceed the limits of two of the three criteria indicated in Article 35, that fact shall affect the application of the derogation provided for in that Article only if it occurs in two consecutive financial years“.

Effects of exceeding or not exceeding the categorisation criteria

Exceeding or failing to exceed at least two of the three criteria for two consecutive financial years has a direct impact on a number of accounting obligations, including:

Determining the category to which the undertaking or group belongs is therefore of significant importance.

Issue: the interpretation of the repetition criterion and how it takes effect

Since its introduction in Luxembourg 35 years ago, the categorisation system based on three size criteria (balance sheet total, net turnover, number of employees) and a two-year repetition criterion has given rise to a number of problems of an interpretative nature.

Among the most pressing issues are the interpretation to be given to the repetition criterion referred to in Article 36 LRCS and, more specifically, the question of the effective date of exceeding or not exceeding at least two of the three size criteria. The consultations carried out tend to indicate that several practices coexist in Luxembourg today.

Considering that a doctrinal clarification would be useful to stakeholders in the financial reporting arena by providing legal certainty to preparers of accounts while enabling governmental users to monitor application, CNC has taken up this interpretative issue by proposing a doctrinal response in the form of a Q&A.

The interpretation adopted in this Q&A is intended to promote consistent and harmonised application of the provisions of Article 36 LRCS by undertakings and groups in the future. However, this interpretation does not call into question the analyses used in the past, which the consultations carried out revealed were not uniform.

What are the interpretations that should be given to the repetition criterion referred to in Article 36 LRCS and to the question of the effective date of exceeding or not exceeding at least two of the three size criteria in the following cases?

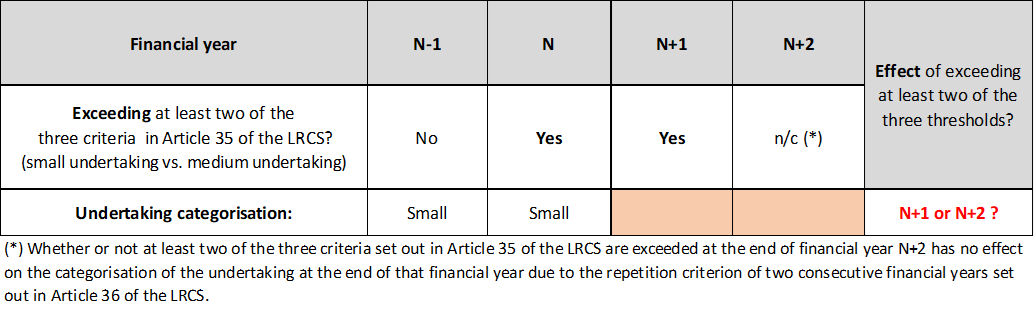

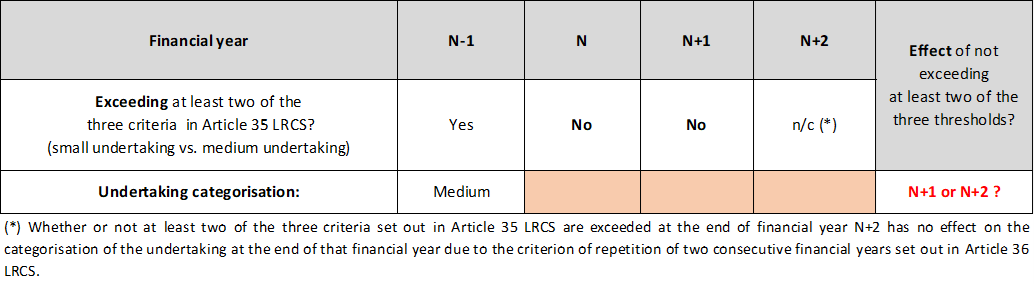

To illustrate this first case, let’s take the situation of undertaking A, categorised as a “small undertaking”, which did not exceed two of the three criteria set out in Article 35 LRCS during the N-1 financial year.

Let’s assume that undertaking A exceeds two of the three criteria in Article 35 LRCS during financial years N and N+1, i.e. for two consecutive financial years.

Would exceeding the size criteria lead to a change of category and, if so, when would this recategorisation take effect?

Firstly, it is clear that exceeding the size criteria would have no effect at the end of financial year N insofar as undertaking A then exceeds two of the three size criteria of Article 35 LRCS for the first time and therefore does not meet the repetition criterion of Article 36 LRCS. Undertaking A would therefore remain a “small undertaking” at the end of financial year N.

On the other hand, at the end of financial year N+1, undertaking A would then exceed two of the three criteria of article 35 LRCS for the second consecutive financial year, resulting in a change of category. While the principle of recategorisation seems to be accepted at the end of financial year N+1, the question however arises as to when the change of category takes effect. In other words, does exceeding the size criteria for two financial years take effect in the financial year in which the second exceeding is noted (N+1) or does it take effect in the financial year following that in which the second exceeding was noted (N+2) (see Fig. 1.1. below).

The consultations carried out suggest that some practitioners consider that the change of category takes effect in the financial year in which the second exceeding is noted (N+1), while others consider that the recategorisation takes effect in the following financial year (N+2).

In this respect, it should be noted that neither the Accounting Directive 2013/34/EU nor Luxembourg accounting law settle the question of the effective date of the double exceeding of the criteria. It should also be noted that the solutions adopted by Luxembourg’s neighboring Member States vary on this point.

Consequently, and in the absence of any legal provisions, the CNC proposes the following doctrinal solution.

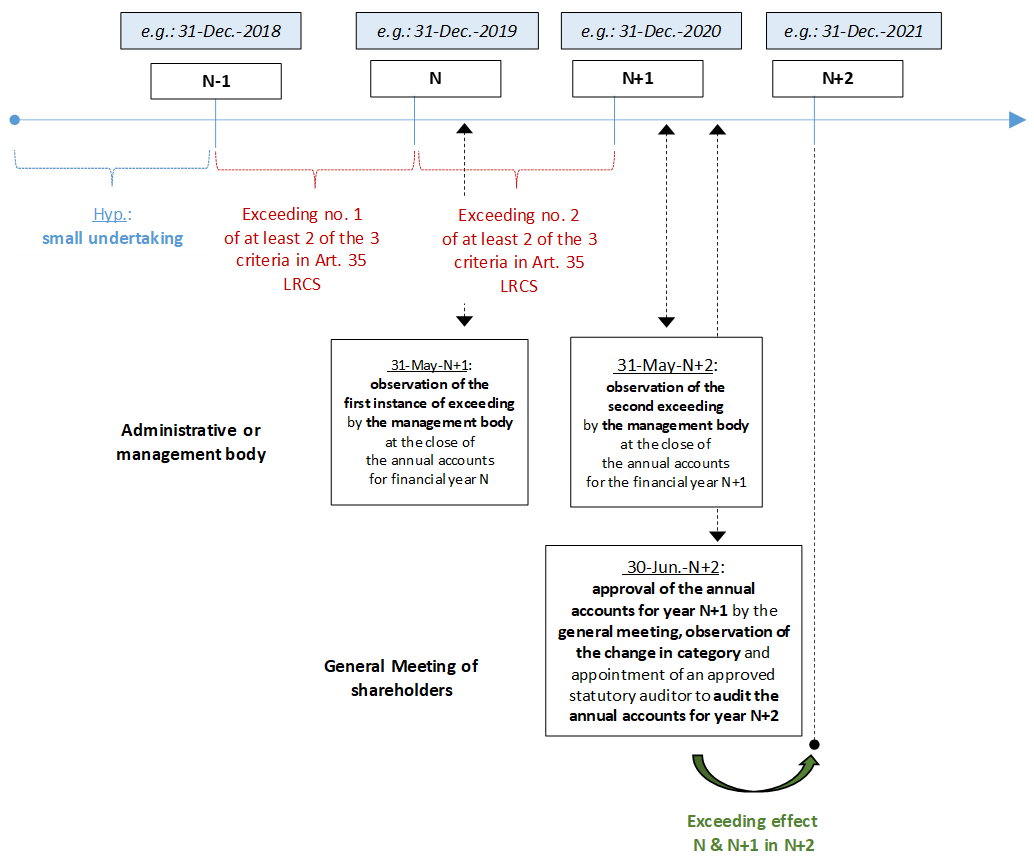

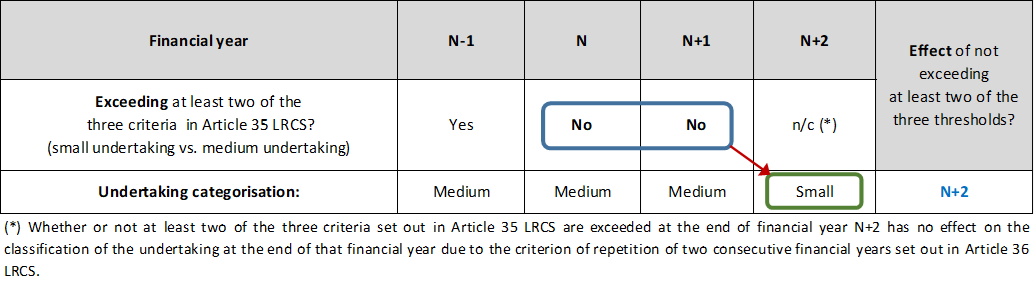

In the case of undertaking A, which is assumed to be organised in the form of a public limited liability company / “société anonyme” (SA), it is expected that the observation that the size criteria have been exceeded in N and N+1 will only be formally made by the administrative or management body when the annual accounts are finalised and submitted to the general meeting of shareholders for approval.

As a result, the second time the size criteria have been exceeded during the financial year N+1, this will only be formally noted at the meeting of the administrative or management body which closes the annual accounts for financial year N+1, held prior to the general meeting of shareholders which approves the said accounts and which the law provides must be held no later than 30 June N+2. Noting that undertaking A has exceeded the size criteria set out in Article 35 LRCS for the second consecutive financial year, the undertaking’s governing bodies must take the necessary measures to change the category of undertaking A from “small undertaking” to “medium-sized undertaking”. Among the measures to be taken are the appointment of a “réviseur d’entreprises agréé” [approved statutory auditor], an appointment which, barring exceptions, falls within the remit of the general meeting of shareholders, and the preparation of a management report and annual accounts in accordance with a more detailed model. However, from a practical point of view, these measures cannot have an effect on financial year N+1, which has been closed and is in the process of being approved by the general meeting of shareholders. As a result, these measures can only be applied in the future, i.e. to the annual accounts for financial year N+2 (see Fig.1.2. below).

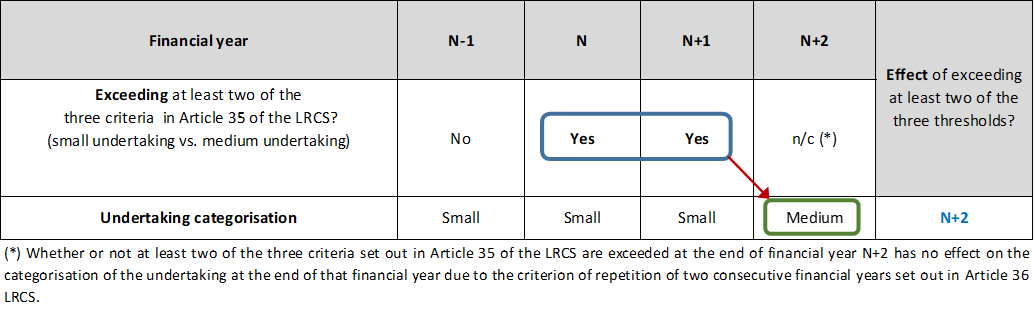

In view of the above, CNC is of the opinion that, as the law currently stands, undertakings cannot be required to conclude that the date on which the second exceeding is identified (N+1) is also the date on which the change of category takes effect. Consequently, CNC considers that it is acceptable for the second exceeding (N+2) to take effect in the financial year following the observation of the second exceeding (N+1).

As a result, in the financial year in which the size criteria are exceeded for the second time (N+1), undertaking A will remain a “small undertaking”. It is only in the following financial year (N+2) that the second exceeding will produce its effects and undertaking A will then become a “medium-sized undertaking” (see Fig. 1.3. below).

The second case describes the opposite situation to the first.

It is assumed that undertaking B is an undertaking categorised as a “medium-sized undertaking” and that in the financial year N-1 it exceeded two of the three criteria set out in Article 35 LRCS.

Let us assume that undertaking B ceases to exceed two of the three criteria of Article 35 LRCS during financial years N and N+1, i.e. for two consecutive financial years. Would this failure to exceed the size criteria lead to a change of category and, if so, when would this recategorisation take effect (see Fig. 2.1 below)?

The wording of Article 36 LRCS establishes the principle of symmetry between the conditions and effects of the exceeding and the non-exceeding of the size criteria, with the two-year repetition criterion applying in both cases. Consequently, CNC is of the opinion that symmetrical reasoning should be applied by considering that the “non-exceeding” only takes effect during the financial year following the one in which the “non-exceeding” was established.

While it is clear that at the end of financial year N there will be no change of category in the absence of the repetition criterion (first “non-exceeding”), the question arises for financial year N+1. At the end of financial year N+1, the second consecutive “non-exceeding” is observed. However, by symmetry with the approach adopted in the case of the exceeding, the “non-exceeding” observed at the end of financial year N+1 will only produce its effects during financial year N+2.

Undertaking B will therefore remain a “medium-sized undertaking” during financial year N+1, with its annual accounts still prepared in accordance with the accounting provisions applicable to medium-sized undertakings and subject to a statutory audit by an approved statutory auditor / “réviseur d’entreprises agréé”. The change of category for undertaking B will take place during financial year N+2 when the undertaking will be classified as a “small undertaking” benefiting from the simplification measures specific to this category of undertakings, including the exemption from drawing up a management report and the exemption from statutory audit by an approved statutory auditor / “réviseur d’entreprises agréé” (see Fig. 2.2. below).

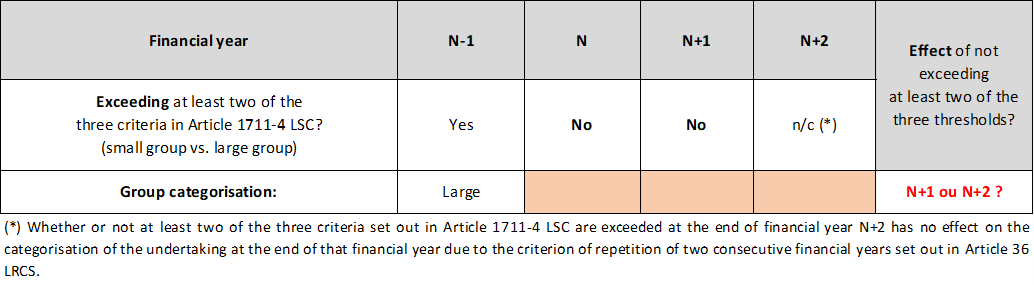

The third case describes situations identical to those described in case 1 and case 2, with the difference that it concerns a group in the context of the preparation of consolidated accounts and not an undertaking in the context of the preparation of annual accounts.

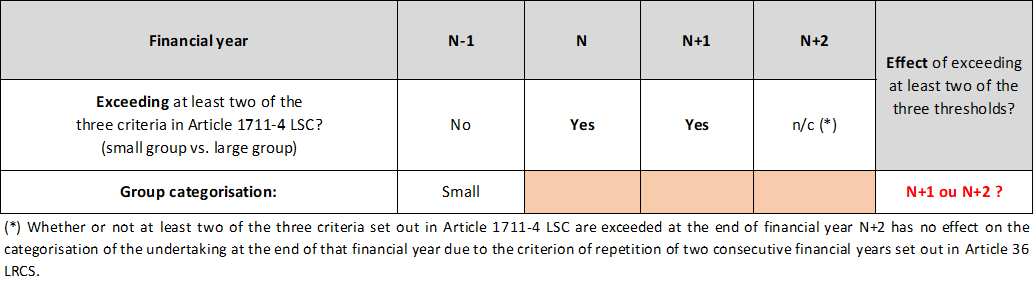

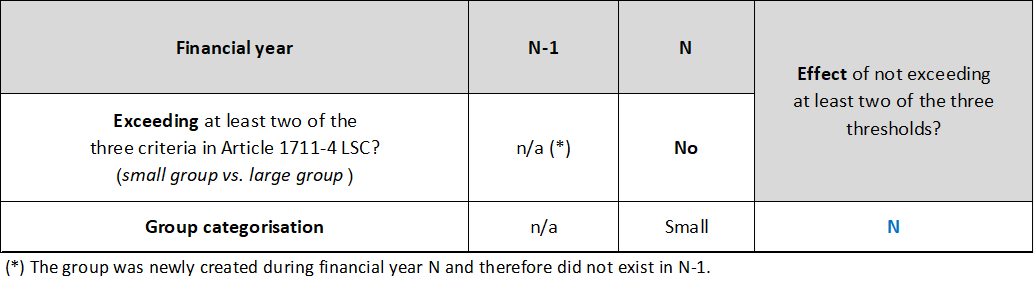

Let’s assume that a pre-existing group C is categorised as a “small group” at the end of financial year N-1 during which it did not exceed two of the three criteria of article 1711-4 LSC.

Let’s assume that Group C exceeds two of the three criteria set out in Article 1711-4 LSC during financial years N and N+1, i.e. for two consecutive financial years.

Would exceeding the size criteria lead to a change of category and, if so, when would this recategorisation take effect (see Fig. 3.1 below)?

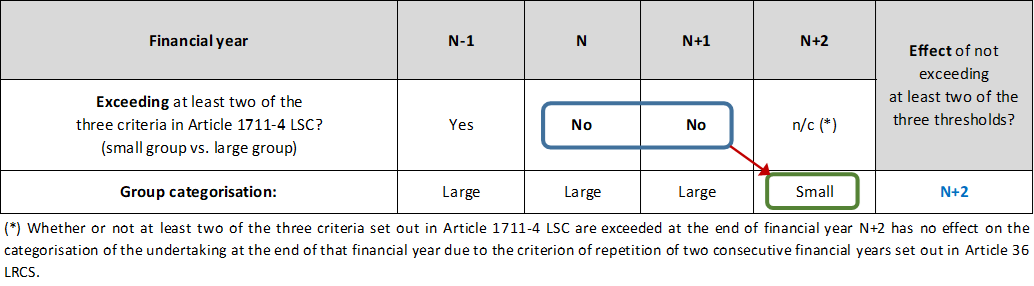

CNC notes that the accounting law applicable to consolidated accounts does not provide for a mechanism distinct from that applicable to annual accounts. Article 1711-4 LSC refers in paragraph 46 to article 36 LRCS, which establishes the principle of the two-year repetition criterion.

In view of the above, CNC is of the opinion that the reasoning should be symmetrical to that developed in the context of accounting law applicable to annual accounts.

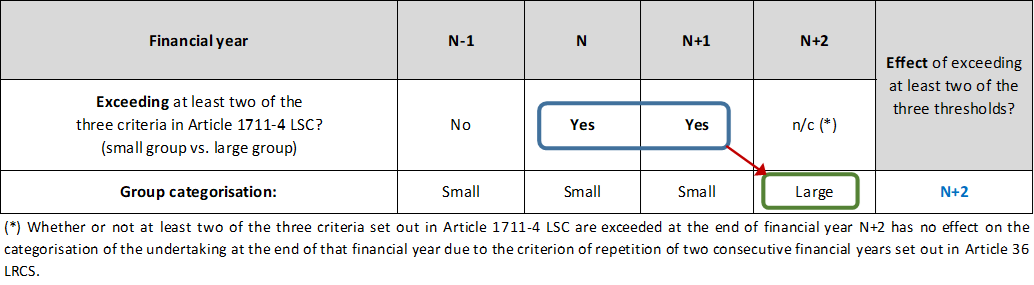

In application of this principle of symmetry, it should be considered that exceeding the criteria at the end of financial year N does not result in any change of category in the absence of a repetition criterion (first exceeding). Similarly, it should be concluded that the second exceeding at the end of financial year N+1 only has an effect in financial year N+2.

As a result, in the financial year in which the size criteria are exceeded for the second time (N+1), Group C will remain a “small group” and it is only in the financial year following the second exceeding (N+2) that Group C will be subject to the accounting regime applicable to “large groups” (see Fig. 3.2 below).

It should be noted that the “annual accounts vs consolidated accounts” symmetry also applies in the context of “exceeding vs non-exceeding”.

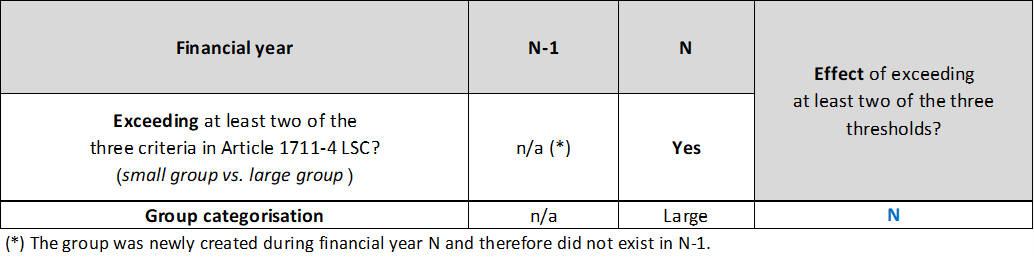

Thus, assuming that the pre-existing group C is categorised as a “large group” at the end of financial year N-1 during which it exceeded two of the three criteria of article 1711-4 LSC but that it ceased to exceed two of these three criteria during financial years N and N+1, i.e. for two consecutive financial years, what would be the impact of this failure to exceed the size criteria and, if applicable, when would the recategorisation take place (cf.: Fig. 3.3. below)?

In application of the principle of symmetry set out in Article 36 of the LRCS, symmetrical reasoning should be applied, considering that the “non-exceeding” only takes effect during the financial year following that in which the “non-exceeding” for two consecutive financial years was observed.

As a result, no change of category will take place at the end of financial year N in the absence of the repetition criterion (first “non-exceeding”). At the end of financial year N+1, the second consecutive “non-exceeding” will then be observed, but by symmetry with the approach adopted in the event of an exceeding, the “non-exceeding” observed will not produce its effect until the following financial year, i.e. during financial year N+2.

Consequently, it follows from the above that Group C will remain a “large group” during financial year N+1 and that its recategorisation as a “small group” will only take place during financial year N+2 (see Fig. 3.4 below).

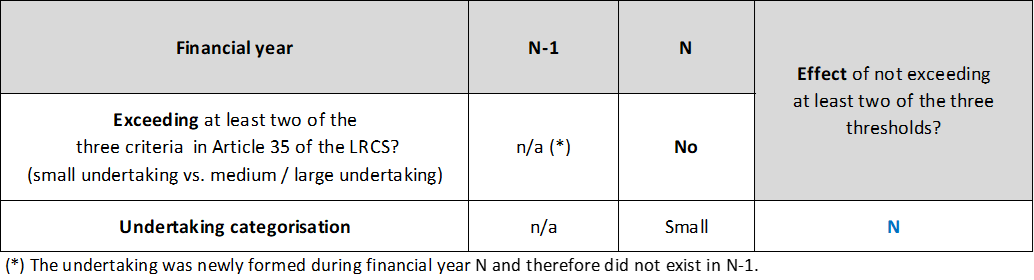

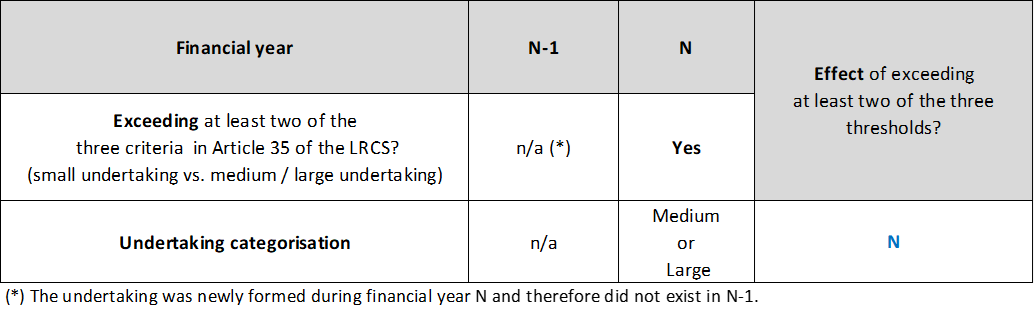

The fourth case describes the situation of a newly formed undertaking.

In such cases, the question arises as to the applicability of Article 36 LRCS, given that no repetition of the exceeding or non-exceeding the size criteria can be established in the absence of a previous financial year.

In such a situation, should it be concluded that the newly formed undertaking is automatically a “large undertaking”, the “small undertaking” and “medium-sized undertaking” accounting regimes being derogatory regimes in the current state of Luxembourg accounting law based on the former 4thDirective? Or, on the contrary, should it be considered that the newly formed undertaking is automatically a small undertaking insofar as, from a factual point of view, it has not exceeded the size criteria for two consecutive financial years (first financial year following formation)?

CNC considers that in the case of a newly formed undertaking, the repetition criterion referred to in Article 36 LRCS does not apply, as the undertaking does not have a history of at least two financial years. In such cases, CNC is of the opinion that it is the responsibility of the undertaking’s governing bodies at the time of its creation to make forecasts in good faith in order to determine whether or not the undertaking will exceed at least two of the three size criteria at the end of its first financial year.

If, on the basis of a good faith estimate, the newly formed undertaking D does not expect to exceed two of the three size criteria of Article 35 LRCS in its first financial year, CNC is of the opinion that it should be categorised as a small undertaking in financial year N (first financial year) (see Fig. 4.1.).

However, in the opposite situation where, on the basis of a good faith estimate, the newly formed undertaking D expects to exceed two of the three size criteria of article 35 LRCS from its first financial year, CNC is then of the opinion that it should then be categorised as a medium-sized or even large undertaking from financial year N (first financial year) (see Fig. 4.2.). In such a case, it would be advisable to appoint the approved statutory auditor / “réviseur d’entreprises agréé” in charge for the statutory audit of the annual accounts at the inaugural general meeting of shareholders or before the first closing of accounts, and to organise the preparation of annual accounts corresponding to the anticipated category regime (e.g.: medium-sized undertaking).

It should be noted that the principle of the good faith estimate is essentially a practical expedient enabling the undertaking and its governing bodies to anticipate the consequences of exceeding or non-exceeding at least two of the three criteria at the end of its first financial year. In this context, it is important that this good faith estimate be periodically reviewed and reconciled with the actual figures, particularly in the event of a significant difference between the forecasts and the actual level of activity.

Finally, it should be noted that when the undertaking’s first financial year7 lasts less than twelve months or more, turnover should be annualised by multiplying them by a fraction, the numerator of which is 12 and the denominator of which is the number of months in the financial period in question.

The fifth case describes a situation identical to that described in case 4, with the difference that it concerns a new group for the preparation of consolidated accounts and not a new undertaking for the preparation of annual accounts.

For example, let us assume that a group E has just been created following the formation of a parent undertaking which, during its first financial year, acquired one or more pre-existing subsidiary undertakings over which it exercises control within the meaning of Article 1711-1 LSC.

Let us now imagine two situations, the first where group E does not exceed two of the three size criteria referred to in Article 1711-4 LSC at the end of its first financial year N and the second where group E exceeds two of the three size criteria from its first financial year (N).

In such cases, which category should apply to Group E at the end of its first financial year?

By analogy with the reasoning developed in point 4. concerning a newly formed undertaking, CNC is of the opinion that in presence of a new group, the repetition criterion referred to in Article 36 LRCS does not apply, as the group does not have a history of at least two financial years. In such a case, CNC considers that it is the responsibility of the parent undertaking’s governing bodies at the time of its creation to make good faith estimates in order to determine whether or not the new group will exceed at least two of the three size criteria at the end of its first financial year.

If, on the basis of a good faith estimate, the new group E does not exceed two of the three size criteria of Article 1711-4 LSC in its first financial year, CNC is of the opinion that it should be categorised as a small group in financial year N (first financial year) (see Fig. 5.1.).

However, in the opposite situation where, on the basis of a good faith estimate, the new group E would exceed two of the three size criteria of Article 1711-4 LSC from its first financial year, which will generally indicate a pre-existence of subsidiary undertakings prior to financial year N, CNC is of the opinion that group E should be categorised from financial year N (first financial year) in the category of large groups, subject – unless otherwise exempted – to the preparation, audit and publication of consolidated accounts from financial year N (cf. Fig. 5.2). In the same way, the parent undertaking’s bodies should organise themselves in advance of the first closing of accounts to enable consolidated accounts to be drawn up, audited by an approved statutory auditor / “réviseur d’entreprises agréé” and published within the time limits laid down by law.

It should be noted that, by symmetry with the analysis proposed in point 4, the principle of the good faith estimate essentially constitutes a practical expedient enabling the parent undertaking and its governing bodies to anticipate the consequences of exceeding or non-exceeding at least two of the three criteria at the end of the first financial year of the newly created group. In this context, it is important that this good faith estimate be periodically reviewed and reconciled with the actual figures, particularly in the event of a significant difference between the forecasts and the actual level of activity.

Finally, and similarly to the reasoning developed in point 4, it should be noted that when the group’s first financial year8 lasts less than twelve months or more, the consolidated turnover should be annualised by multiplying it by a fraction, the numerator of which is 12 and the denominator of which is the number of months included in the financial period in question.

*

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Catégorisation des entreprises : interprétation du critère de répétition visé à l’article 36 LRCS”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible in accordance with general law for any decisions taken based on this document.

1 Law of 4 May 1984 amending the law of 10 August 1915 on commercial companies (section XIII – Annual accounts). Mém. A – N°40 of 10 May 1984.

2 Fourth Council Directive of 25 July 1978 based on Article 54 (3) (g) of the Treaty on the annual accounts of certain types of companies (78/660/EEC).

3 With the exception of undertakings whose securities are admitted to trading on a regulated market in the European Union within the meaning of Article 1 point 31 of the Law of 30 May 2018 on markets

4 Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC.

5 Parliamentary document 2657-0, Draft law adapting the amended law of 10 August 1915 on commercial companies to Directive 78/660 of the Council of the European Communities of 25 July 1978, Comments on Article 216, p. 32.

6 Art. 1711-4 (4) LSC:

“Article 36 of the amended law of 19 December 2002 on the register of commerce and companies and the accounting and annual accounts of undertakings shall be applicable”.

7 N.B.: the same approach (annualising turnover) would also apply during the life of the undertaking, for example in the event of a change in the closing date resulting in a shorter financial year (lasting less than 12 months).

8 N.B.: the same approach (annualisation of consolidated turnover) would also apply during the existence of the Group, for example in the event of a change of financial year-end resulting in a shorter financial period (less than 12 months).