UNOFFICIAL TRANSLATION

The law of 23 July 2016 on reserved alternative investment funds1 (hereinafter the “RAIF law”) introduced a new investment vehicle into Luxembourg law, better known by its acronym RAIF (in French FIAR2).

The RAIF is an alternative investment fund (AIF) within the meaning of the law of 12 July 20133 (hereinafter the “AIFM law”) which must necessarily be managed by an alternative investment fund manager (AIFM) and which may be organised in the form of a common investment fund (“fonds commun de placement” (FCP))4, an “investment company with variable capital” (SICAV)5 or any other legal form provided for by Luxembourg law, in particular one of the forms of commercial companies referred to in the amended law of 10 August 1915 on commercial companies (hereinafter the “law of 1915”)6.

By analogy with undertakings for collective investment (UCI)7, specialised investment funds (SIF)8 and investment companies in risk capital (SICAR)9, RAIFs can be set up with multiple sub-funds, each corresponding to a distinct part of the net assets of the reserved alternative investment fund. However, unlike UCI, SIF and SICAR, RAIF are not subject to supervision by a Luxembourg supervisory authority.

Given the many overlapping characteristics of RAIFs (e.g. regulatory status, legal form, sector-specific accounting provisions, absence of prudential supervision), determining the accounting regime applicable to these vehicles appears difficult and raises questions, particularly as regards the formalities for filing financial data with the Trade and companies register (RCS).

Following the entry into force of the RAIF law, a number of questions have arisen concerning the accounting obligations applicable to this new investment vehicle, including the following:

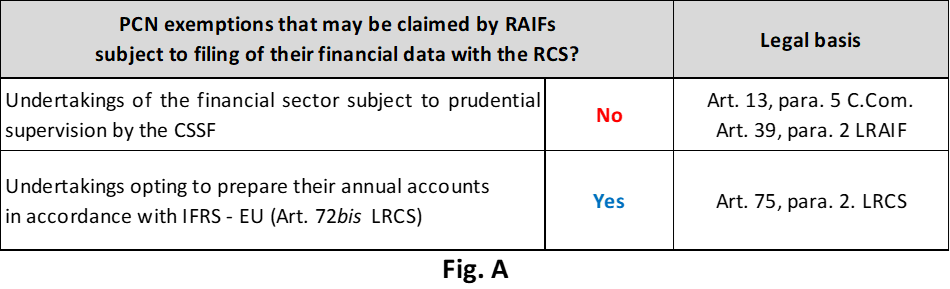

As Luxembourg accounting legislation currently stands, only undertakings required to file their financial data with the RCS are subject to the Standard chart of accounts (PCN). In practice, these are the companies referred to in article 8 C.Com. with the exception of those exempted from the PCN pursuant to article 13 C.Com. or pursuant to article 75 LRCS (IFRS – EU regime). Consequently, the RAIFs concerned by the PCN are those organised in the form of commercial companies with legal personality, such as:

It follows from the above that RAIFs organised in one of the forms currently exempt from filing financial data with the RCS are also exempt from the obligation to comply with the PCN.

With regard to RAIFs organised in one of the commercial forms subject to the filing of financial data with the RCS (see point 1.1.), it should be noted that they cannot – under any circumstances – claim the exemption applicable to undertakings of the financial sector subject to prudential supervision by the CSSF (e.g. SICAVs covered by the 2010 UCI law, SIFs covered by the 2007 law, SICARs covered by the 2004 law).

The RAIFs covered by the 2016 RAIF law are unique in that they are not subject to prudential supervision by the CSSF, as Article 39, para. 2 of the RAIF Law states that “[t]he offering document must contain a clearly visible statement on its cover page to the effect that the reserved alternative investment fund is not subject to supervision by a Luxembourg supervisory authority”.

In the same way as other companies subject to drawing up and filing their annual accounts with the RCS in accordance with Title II LRCS, RAIFs may avail themselves of the exemption provided for in Article 75, para. 2 LRCS relating to undertakings drawing up their annual accounts in accordance with IFRS as adopted by the European Union pursuant to the option provided for in Article 72bis LRCS (see Fig. A).

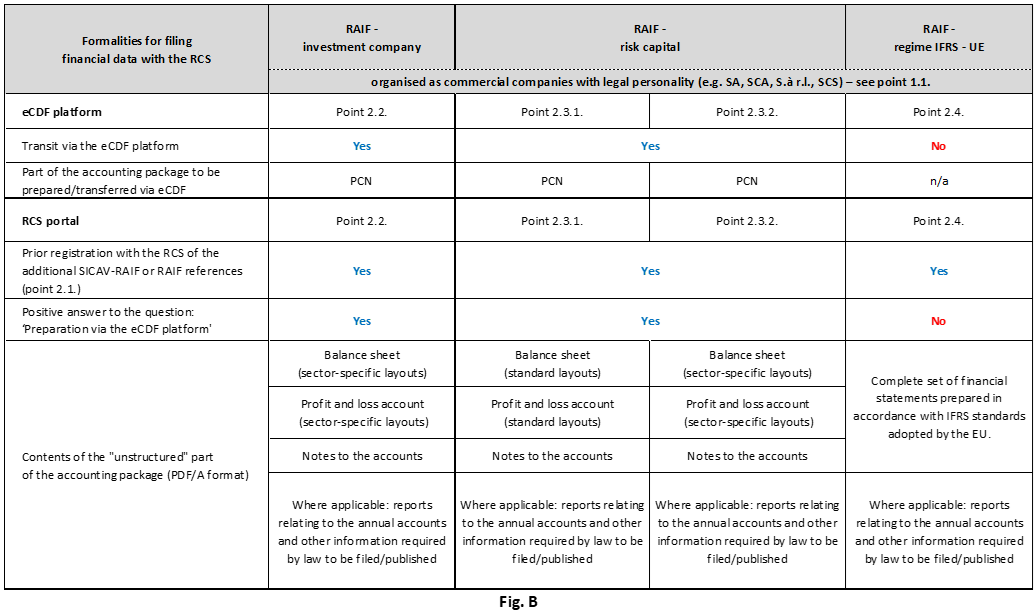

As the law currently stands, Luxembourg accounting legislation draws a distinction between, on the one hand, undertakings which are required to file their financial data in a structured format and which, for this purpose, have to pass through the electronic financial data platform (eCDF) prior to filing with the RCS and, on the other hand, undertakings which are required to file their financial data in the classic manner and which do not have to pass through the eCDF platform and which therefore file directly with the RCS11. To put it simply, the former are generally undertakings subject to the obligation to file the trial balance of their accounts in accordance with the PCN, while the latter are generally undertakings exempt from the PCN.

In this respect, it should be noted that the RAIF – because of its hybrid nature – is a special case. In order to clarify the filing formalities applicable to RAIFs that are required to file their financial data with the RCS, a distinction should be made between three different situations:

Beforehand, and considering that the RAIF is a special case with regard to the filing of financial data, it is important to stress the importance of identifying the RAIF beforehand by registering additional information with the RCS (see point 2.1.).

RAIFs subject to filing their financial data with the RCS and using the “LUX GAAP – FV12” or “LUX GAAP13” regimes have the particularity – compared with undertakings governed by general law – of being subject to the obligation to file the trial balance of accounts in accordance with the PCN without, however, being required to present their balance sheet and profit and loss account in accordance with the layouts set out in general law (art. 34, 35, 46 and 47 LRCS).

In view of the above, a financial data filing service specifically dedicated to RAIFs has been set up by the RCS administrator14. However, this service is only available to RAIFs that are identified as such, i.e. those that have requested that the following additional information be registered with the RCS:

Said entry in the RCS of additional information on the basis of Article 6 point 2° LRCS, is provided for by Article 1 of the Ministerial Regulation of 27 May 201615.

It should be noted that only RAIFs that have registered these additional details with the RCS have access to the data filing service dedicated to RAIFs and can therefore file financial data in accordance with the law.

“RAIF – investment companies” are defined – for the purposes of this Q&A – as RAIFs other than those referred to in Article 48 paragraph 1 of the RAIF Law (cf.: point 2.3.). The “RAIF – investment companies” are therefore those whose sole object is “the collective investment of their funds in securities with the aim of spreading investment risks and giving investors the benefit of the results of the management of their assets” (art. 1 para. 1 point b) LRAIF), which are liable to the subscription tax (art. 45 para. 1 LRAIF) and whose fiscal control is ensured by the “Administration de l’enregistrement, des domaines et de la TVA” (art. 47 LRAIF).

“RAIF – investment companies” which use the “LUX GAAP – FV” or “LUX GAAP” regimes for the preparation and filing of their annual accounts must:

It should be noted that, in application of the principle “lex specialis derogat legi generali“, “RAIF – Investment companies” which draw up their balance sheet and profit and loss account in accordance with the sector-specific layouts or schedules provided for in article 38 para. 4 of the RAIF law (see: annex 1) are exempt from the obligation to comply with the layouts of balance sheet and profit and loss account set out by general law (Articles 34, 35, 46 and 47 LRCS).

“RAIF – risk capital” are defined – for the purposes of this Q&A – as the RAIF referred to in Article 48 paragraph 1 of the RAIF Law. “RAIF – risk capital” are therefore those whose “exclusive object is the investment of their funds in assets representing risk capital (…) [which] are not required to spread investment risks” (art. 48 para. 1 lit. a) LRAIF) and which choose to place themselves under the regime of article 48 of the RAIF Law. The “Administration des contributions directes” is responsible for the tax control of “RAIF – risk capital” (art. 48 para. 1 lit. b) LRAIF).

Unlike “RAIF – investment companies”, “RAIF – risk capital” are not required to comply with the sector-specific balance sheet and profit and loss account layouts or schedules provided for in Article 38 para. 4 of the RAIF Law. In the absence of sector-specific layouts or schedule specifically defined by the RAIF law for “RAIF – risk capital”, CNC is of the opinion that they are free to draw up their balance sheet and profit and loss account in accordance with the layouts set out in general law (art. 34, 35, 46 and 47 LRCS).

Alternatively, the CNC considers that “RAIF – risk capital” may voluntarily use the sector-specific balance sheet and loss account layouts or schedules as defined by article 38 para. 4 of the RAIF Law (see: annex 1).

In view of the above, “RAIF – risk capital” that use the “LUX GAAP – FV” or “LUX GAAP” regimes to draw up and file their annual accounts have two options: to use the balance sheet and profit and loss account layouts set out by general law (art. 34, 35, 46 and 47 LRCS) or to use the sector-specific balance sheet and profit and loss account layouts or schedules (art. 38 para. 4 LRAIF).

“RAIF – Risk capital” that use the layouts of balance sheet and profit and loss account set out in general law (Art. 34, 35, 46 and 47 LRCS) must:

“RAIF – risk capital” that use the balance sheet and profit and loss account layouts set out by sector-specific law (art. 38 para. 4 LRAIF) must:

It should be noted that, in application of the principle “lex specialis derogat legi generali“, “RAIF – risk capital” which draw up their balance sheet and profit and loss account in accordance with the sector-specific layouts provided for in Article 38 para. 4 of the RAIF Law are exempt from the obligation to comply with the standard layouts of balance sheet and profit and loss account (Articles 34, 35, 46 and 47 LRCS).

“RAIF – IFRS-EU regime” are defined – for the purposes of this Q&A – as “RAIF – investment company” and “RAIF – risk capital” using the “IFRS – EU regime” for the preparation and filing of their annual accounts instead of the “LUX GAAP – FV” and “LUX GAAP” regimes.

RAIF that use the IFRS – EU regime – regardless of whether they are a “RAIF – investment company” or a “RAIF – risk capital” – must:

In summary, the formalities for filing RAIFs financial data with the RCS can be summarised as follows, distinguishing between the preliminary part relating to transit via the eCDF platform and the part relating to filing on the RCS portal (see Fig. B).

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Fonds d’investissement alternatifs reservés (FIAR) : plan comptable normalisé (PCN) et formalisme de dépôt des données financières”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible in accordance with general law for any decisions taken based on this document.

1 Law of 23 July 2016 on reserved alternative investment funds, Mém. A – N°140 of 28 July 2016.

2 Fonds d’investissement alternatif réservé (FIAR).

3 Law of 12 July 2013 on alternative investment fund managers, Mém. A – N°119 of 15 July 2013.

4 Chapter 2 of the RAIF law.

5 Chapter 3 of the RAIF law.

6 Chapter 4 of the RAIF law.

7 Law of 17 December 2010 on undertakings for collective investment, Mém. A – N°239 of 24 December 2010.

8 Law of 13 February 2007 on specialised investment funds, Mém. A – N°13 of 13 February 2007.

9 Law of 15 June 2004 relating to the investment companies in risk capital (SICAR), Mém. A – N°95 of 22 June 2004.

10 By way of exception, SCSs are not subject to the PCN or to the filing of financial data if all their partners with unlimited liability (general partners or partners of the general partners) are not organised in one of the forms referred to in article 77, para. 2, points 2° and 3° LRCS and their turnover for the last financial year does not exceed 100,000 euros.

11 Grand Ducal Regulation of 14 December 2011 determining the procedure for filing the accounting package with the administrator of the Trade and companies register, the conditions for arithmetic and logical checks concerning the annual accounts.

12 The LUX GAAP – FV regime applicable to RAIFs stems from the application of article 57 LRCS as provided for in article 38 (4) LRAIF. Pursuant to Article 57 LRCS, RAIFs “(…) must value the securities in which they have invested their funds on the basis of their fair value (…)”.

13 Although the LUX GAAP – FV regime is the default accounting regime applicable to RAIFs, use of the LUX GAAP regime based on the principles of prudence (art. 51 (1) c) LRCS) and valuation / measurement at historical acquisition cost (art. 52 LRCS) is not excluded. Indeed, the reference in articles 26 (4) and 33 (1) of the RAIF law to the terms “unless otherwise provided in the articles of incorporation or partnership agreement [“RAIF – SICAV”] / in the constitutive documents [“RAIF – Other legal forms”] (…)” implies that – by way of derogation – a valuation / measurement of the assets of the RAIF on a basis other than fair value may be applied. As such an alternative valuation / measurement basis must remain in accordance with general accounting law in the absence of special provisions in sector-specific accounting law, it must be deduced that such an alternative valuation / measurement will generally be based on the cost model, less depreciation and value adjustments where applicable.

14 Luxembourg Business Registers (LBR): www.lbr.lu

15 Ministerial Regulation of 27 May 2016 laying down the criteria for the presentation and form of documents intended for publication in the Recueil électronique des sociétés et associations as amended by the Ministerial Regulation of 20 December 2017.

16 RAIF uses the structured format provided on the eCDF platform (Standard chart of accounts (PCN)).

17 RAIF uses the structured format provided on the eCDF platform (Standard chart of accounts (PCN)).

18 RAIF uses the structured format provided on the eCDF platform (Standard Chart of Accounts).