UNOFFICIAL TRANSLATION

The Accounting Directive 2013/34/EU1 introduced a maximum harmonisation regime applicable to small undertakings, the main objective of which is to reduce the administrative burden on them in relation to the preparation and publication of annual accounts. Considering the central role played by small and medium-sized enterprises (SMEs), the underlying idea is to ensure that “administrative burdens are proportionate to the benefits they bring (…) by focusing on measures that create growth and jobs“2.

In this context, undertakings categorized as “small undertakings” may present abridged notes to the annual accounts that do not include in particular details of the participations held.

While this simplification measure seems appropriate for small undertakings with an industrial or commercial activity, it is more problematic for undertakings that are also classified as “small undertakings” but whose activity is predominantly financial, i.e. mainly holding and/or financing holding companies.

Following the entry into force of the Law of 18 December 20153 transposing Directive 2013/34/EU, what are the conditions under which a Luxembourg undertaking may validly claim – on the basis of Articles 65 (1) 2° and 66 LRCS – the exemption from disclosure in the notes to the accounts of all or part of the details of the participations held?

This Q&A contains a reminder of the following points:

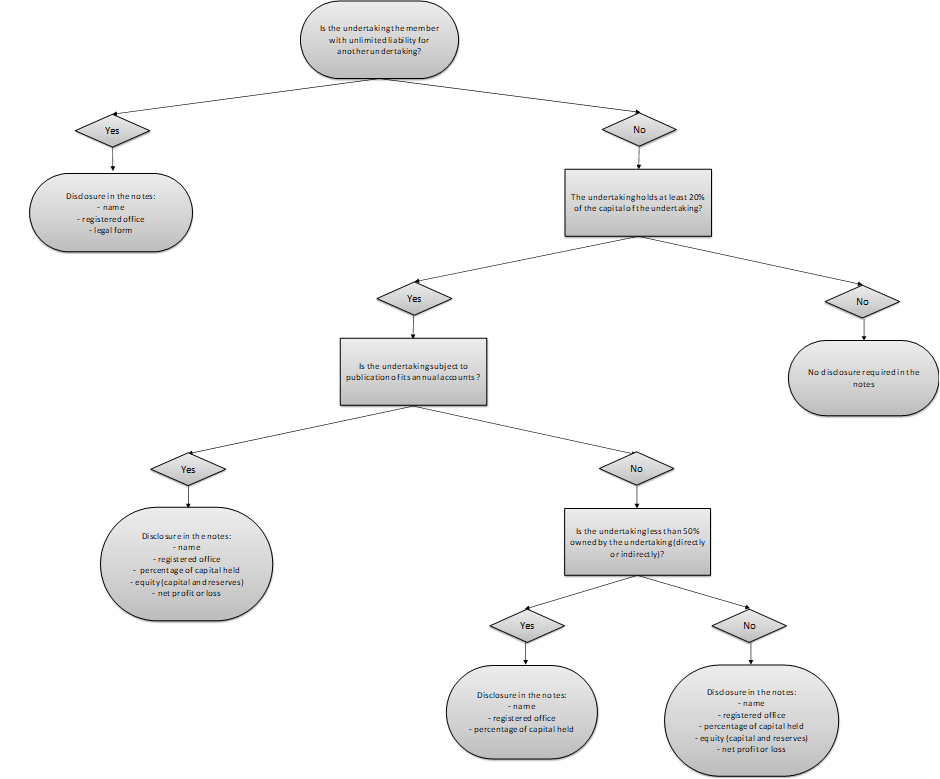

Article 65 (1) 2° LRCS provides that the notes to the annual accounts of undertakings subject to general accounting law (Title II LRCS) must include the following disclosure:

” 2° the name and registered office of each of the undertakings in which the undertaking, either itself or through a person acting in its own name but on the undertaking’s behalf, holds at least twenty per cent of the capital, showing the proportion of the capital held, as well as the amount of capital and reserves and the profit or loss for the latest financial year of the undertaking concerned for which the accounts have been approved. This information may be omitted where for the purposes of Article 26 paragraph (3) it is immaterial. The information concerning capital and reserves and the profit or loss may also be omitted where the undertaking concerned does not publish its balance sheet and less than fifty per cent of its capital is held, directly or indirectly, by the undertaking; the name, registered office and the legal form of each undertaking of which the undertaking is the member having unlimited liability. This information may be omitted when, for the purposes of Article 26 paragraph (3), it is immaterial.4”

An analysis of Article 65 (1) 2° LRCS shows that a distinction is made between participations held on the basis of the following two parameters in particular:

i) The limited or unlimited nature of the liability incurred by the undertaking holding the participation;

ii) The legal obligation for the undertaking to publish its annual accounts.

In this context, article 65 (1) 2° LRCS requires that the undertaking holding the participating interests must generally provide the following information in the notes to its annual accounts:

Where an undertaking incurs unlimited liability as a result of its participation held in another undertaking, the notes to its annual accounts must provide the following information, regardless of the percentage of shareholding (e.g. < 20%):

This information must be provided for any participation held in which the company is the member with unlimited liability.

By way of illustration, this would be the case of a “société anonyme which is the general partner of a société en commandite simple even though its holding in the capital is less than 20%“5.

It may also be noted that this information relating to participations held for which the undertaking is indefinitely liable must be provided:

For undertakings other than those for which the undertaking incurs unlimited liability (see point 1.1.), the information required by article 65 (1) 2° LRCS applies only to undertakings in which at least 20% of the capital is held, either directly by the undertaking or through an agent.

In such cases, the following information must be provided in the appendix:

The amounts of shareholders’ equity (capital and reserves) and net profit or loss of the undertakings held are those relating to the latest financial year for which accounts have been approved by the competent body of the undertaking held.

For the undertakings referred to in point 1.2, i.e. undertakings in which the liability of the undertaking is limited (e.g. SA, SARL and their foreign equivalents) and in which at least 20% of the capital is held by the undertaking, an exemption from disclosure of the amount of equity and profit or loss is provided for in the following cases (two cumulative conditions):

and

In other words, for undertakings not subject to publication of annual accounts and in which the undertaking holds at least 20% but less than 50% of the capital and incurs only limited liability, only the following information will generally be required in the notes to the annual accounts of the company holding the participation pursuant to article 65 (1) 2° LRCS:

*

In summary, the information to be provided pursuant to Article 65 (1) 2° LRCS can be presented in the form of a decision tree (see Fig. 1 below).

For undertakings with a predominantly industrial or commercial activity, the general principle applicable can be presented as follows (points 2.1. and 2.2.).

In application of the measures to simplify and reduce the administrative burden for small undertakings and in accordance with Article 66, 1st sentence LRCS, “(t)he undertakings referred to in Article 35 shall be authorised to prepare abridged notes to their accounts without the information required in Article 65 paragraph (1) point 2° (…)”.

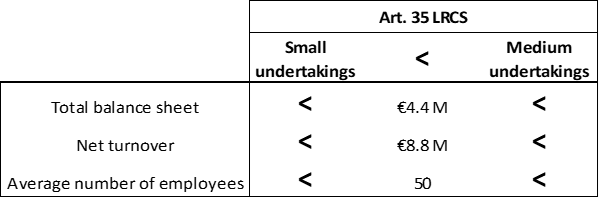

As a result, small undertakings – defined in Luxembourg as those which do not exceed two of the three criteria referred to in article 35 LRCS (see Fig. 2 below) for two consecutive financial years – are exempt from disclosing in the notes to their annual accounts the information required by article 65 (1) 2° LRCS concerning certain shareholdings held.

In practice, this exemption only applies to small undertakings whose main activity is industrial or commercial (see point 3).

The exemption from disclosure of details of participations held provided for in article 66 LRCS being reserved for small undertakings within the meaning of article 35 LRCS, it follows that medium-sized undertakings (those exceeding at least two out of the three criteria of article 35 LRCS for two consecutive financial years) and, all the more so,large undertakings (those exceeding at least two out of the three criteria of article 47 LRCS for two consecutive financial years) are – as a general rule – required to disclose the information listed in article 65 (1) 2° LRCS in the notes to their annual accounts.

However, Article 65 (1) 2° provides for an exception to the principle of mandatory disclosure in the notes to the accounts by medium-sized and large undertakings in cases where “This information may be omitted where for the purposes of Article 26 paragraph (3) it is immaterial”, i.e. the objective of a true and fair view.

It should be noted that this omission – where it is not material – may concern both information relating to undertakings in which the undertaking is the member with unlimited liability (name, registered office and legal form) and information relating to other undertakings (with limited liability) in which the undertaking holds at least 20% of the capital (name, registered office, percentage of capital held, amount of shareholders’ equity (capital and reserves), amount of net profit or loss).

By way of illustration, the case of an industrial SME whose main activities are carried out directly in the Grand Duchy of Luxembourg may be considered. If the latter were to hold a stake in the capital of one or more distribution companies based abroad, the relative importance of which would be minimal in relation to the assets and liabilities, financial position and profit or loss of the Luxembourg undertaking, then the provision in the notes to the annual accounts of the information referred to in Article 65 (1) 2° LRCS would not be required in the light of the true and fair view objective.

The general principle set out in point 2 is, however, subject to a major exception in the specific case of undertakings with a predominantly financial activity, mainly holding companies and/or financing holding companies.

The categorisation of undertakings into small, medium-sized and large undertakings on the basis of the three criteria of “balance sheet total”, “net turnover” and “average number of employees” means that undertakings subject to general accounting law which carry out predominantly financial activities – mainly holding companies and/or financing holding companies – are most of the time categorised as “small undertakings”.

This situation results from the fact that financial income – which represents the main source of income for these undertakings – does not constitute “turnover” within the meaning of Article 48 LRCS (Q&A CNC 17/0136). In this context and in the absence of turnover, the categorisation of these undertakings depends on whether or not the two remaining criteria are exceeded, i.e. the “balance sheet total” and the “average number of employees”. As a general rule, these undertakings exceed only one of these two criteria, namely the balance sheet total. As a result, these undertakings generally fall into the category of small undertakings benefiting from measures to simplify and reduce the administrative burden, including – in principle – exemption from the disclosure of information required under Article 65 (1) 2° LRCS.

However, insofar as the omission from the notes to the accounts of information relating to the participations held by such undertakings would be such as to call into question the true and fair view of their annual accounts and therefore their overall compliance with the law, the legislator introduced by the Law of 18 December 2015 a major exception within Article 66, 2nd sentence LRCS which provides that:

“However, in accordance with Article 26 paragraphs (4) and (5), the information required in Article 65 paragraph (1) point 2° may not be omitted where it is material for the purposes of the true and fair view referred to in Article 26 paragraph (3)“.

In practice, given that the participations held by these undertakings with a predominantly financial activity – mainly holding companies and/or financing holding companies – generally constitute, directly or indirectly, their main assets, their primary source of income and their principal activity, such undertakings cannot validly claim an exemption from the requirement to disclose the information referred to in article 65 (1) 2° LRCS in the notes to the annual accounts.

This is the effect of the derogating provision in Article 66, 2nd sentence LRCS, which “in the name of the true and fair view and of transparency (…) goes beyond the minimum requirements of the Directive, a provision which takes into account the specific conditions and needs of the local market“7.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Mention en annexe des comptes annuels des participations détenues (art. 65 (1) 2° LRCS) et exception au principe de dispense des petites entreprises (art. 66 LRCS)”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible in accordance with general law for any decisions taken based on this document.

1 Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC.

2 See: Recital (1) dir. 2013/34/EU.

3 Law of 18 December, 2015 amending, with a view to the transposition of Directive 2013/34/EU of the European Parliament and of the Council of 26 June, 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC: 1) the amended law of 10 August 1915 on commercial companies; 2) Title II of the amended law of 19 December 2002 on the trade and companies register as well as on the bookkeeping and annual accounts of undertakings; 3) Title II of Book I of the Commercial Code.

4 True and fair view objective

5 Parliamentary document 3781-0, Comments on Article 2, p. 6

6 Q&A CNC 17/013 Notion of turnover (Art. 48 LRCS): impact of the changes introduced by the law of 18 December 2015

7 Parliamentary document 6718-5 (17.11.2015), Amendments adopted by the Legal Commission, Chamber of Deputies, p.10