UNOFFICIAL TRANSLATION

Although legally independent, many undertakings are – both in Luxembourg and abroad – subsidiary undertakings, parent undertakings or even undertakings that are both parent and subsidiary and whose operational and financial activities are economically dependent and form part of a wider group.

In this context, the legislator has provided that undertakings must make various disclosures in the notes to their annual accounts in order to inform external users of the fact that the undertaking belongs to a group and of the existence of consolidated accounts representing the financial position and results of the group of undertakings.

Given the variety of situations that exist in practice, a reminder of the information relating to the consolidated accounts as it must appear in the notes to the annual accounts – whether this is expressly required by accounting legislation or stems more broadly from accounting practices – seems appropriate.

In accordance with Luxembourg accounting legislation and practice, what information should be provided about the consolidated accounts in the notes to the annual accounts of undertakings?

Insofar as the answer to this question varies considerably depending on whether the undertaking is a subsidiary undertaking, a parent undertaking or even whether the undertaking is both a parent undertaking and a subsidiary undertaking, this Q&A suggests to deal with the subject as follows:

Article 65 paragraph (1) point 15° LRCS provides that the notes to the annual accounts of a subsidiary undertaking subject to the preparation of annual accounts pursuant to Chapter II of Title II LRCS must include the following information:

” 15° a) the name and registered office of the undertaking which draws up the consolidated accounts of the largest body of undertakings of which the undertaking forms part as a subsidiary undertaking;

(b) the name and registered office of the undertaking which draws up the consolidated accounts of the smallest body of undertakings included in the body of undertakings referred to in a) of which the undertaking forms part as a subsidiary undertaking;

c) the place where copies of the consolidated accounts referred to in a) and b) may be obtained unless they are unavailable”.

Purpose of the disclosure in the notes to the annual accounts (Art. 65 (1) 15° LRCS)

The disclosure required by article 65 (1) 15° LRCS is intended to provide the public with information on the connections between the subsidiary undertaking whose annual accounts are filed with the Trade and companies register (RCS) and the group or groups of undertakings of which it forms part as a subsidiary, as well as on the parent undertaking or undertakings controlling it, insofar as being part of a group and being controlled by a parent undertaking may have an influence on the subsidiary undertaking itself, from both an operational and a financial point of view.

Reminder of the terms of application

The disclosure in the notes to the annual accounts referred to in Article 65 (1) 15° LRCS is subject to the prior fulfilment of two conditions, namely:

(i) being a subsidiary undertaking

and

(ii) being included in the consolidated accounts of a group of undertakings

As a result, undertakings which are not subsidiary undertakings, for example because they are owned by one or more natural persons or because none of the undertakings owning them has control over them (e.g. undertakings with a fragmented shareholding structure), are not subject to the disclosure referred to in Article 65 (1) 15° LRCS.

Similarly, undertakings which are subsidiary undertakings but which are not included in the consolidated accounts of a parent undertaking (e.g. a small group exempted from drawing up consolidated accounts) are also exempted from disclosing in the notes to the annual accounts the information required by article 65 (1) 15° LRCS.

On the other hand, it should be noted that for undertakings which are subsidiaries included in the consolidated accounts of a group, the information referred to in article 65 (1) 15° LRCS must be disclosed whether or not the said consolidated accounts are accessible to the public. Article 65 (1) 15° c) LRCS provides that reference must be made to “the place where the consolidated accounts referred to in points a) and b) may be obtained, unless they are unavailable” (e.g. the consolidated accounts of a parent undertaking which is based in a third country and is not subject to the general publication requirement laid down in Directive 2013/34/EU). In this respect, the indication of the availability of the consolidated accounts – synonymous with public access to the said accounts – could, for example, take the form of a reference to the central register where the consolidated accounts can be obtained (e.g. Companies House in the United Kingdom, Central Balance Sheet Office in Belgium, Chamber of Commerce in the Netherlands, etc.), to the company’s or group’s website or even to the company’s registered office. The unavailability of consolidated accounts – synonymous with non-accessibility to the public – may be indicated and be accompanied – where appropriate – by a statement explaining the reasons for this unavailability (e.g. consolidated accounts drawn up exclusively for contractual purposes, consolidated accounts drawn up in application of a law or regulation which does not provide for a general publication obligation apart from communication to the general meeting of shareholders).

Practical applications

Draft bill of law 3154 on the preparation of consolidated accounts, which is the source of the current article 65 (1) 15° LRCS, provides useful information for a proper understanding of this article and of the various possible scenarios. In this respect, an extract from the preparatory work is given below, supplemented by explanatory diagrams.

Extracts from parliamentary document 3154-0, p. 621

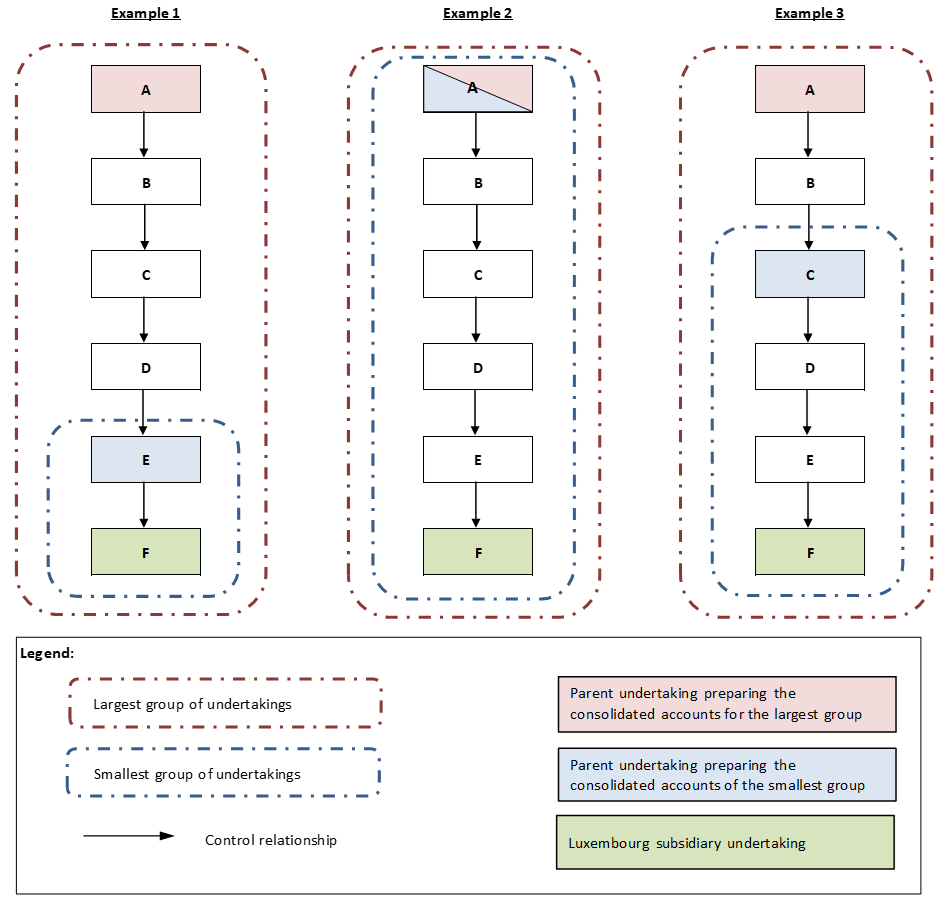

“For a better understanding, it should be remembered that a consolidated group may consist of a cascade of undertakings, each of which, at an intermediate stage in the chain, is simultaneously parent and subsidiary. This is the case in the following example: F is a subsidiary of E, E of D, D of C, C of B and B of A. In the case of F, a Luxembourg company governed by [Title II LRCS], the parent company of the smallest group is E and the parent company of the largest group is A. If A and E draw up consolidated accounts, it is their identity that F shall provide [A/N: example 1].

If the consolidated accounts are drawn up solely by A, the largest group and the smallest group will blend in and F will only have to provide the name and registered office of A [A/N: example 2]. Alternatively, if the consolidated accounts are drawn up not by E but by C, the parent company of the smallest group comprising F will be undertaking C [A/N: example 3].

Illustrative examples of notes to accounts2

For illustrative purposes, the following are examples of notes to the annual accounts drawn up in accordance with Article 65 (1) 15° LRCS.

Example 1 with the assumption that the consolidated accounts of A and E are available

“Undertaking F is included in the consolidated accounts drawn up by undertaking A, whose registered office is located at …………………. (specify address), which is the largest undertaking of which undertaking F is a subsidiary. The consolidated accounts drawn up by undertaking A can be obtained from the company’s website (www.address-URL-undertaking-A.com/stakeholders-relations).

Undertaking F is also included in the consolidated accounts drawn up by undertaking E, whose registered office is located at ……………………. (specify address), constituting the smallest group of which undertaking F forms part as a subsidiary undertaking. The consolidated accounts drawn up by undertaking E are available to the public at the company’s registered office. A copy of all or part of these consolidated accounts may be obtained free of charge on written request sent by post to the registered office of undertaking F.”

Example 2 assuming that A’s consolidated accounts are available

“Undertaking F is included in the consolidated accounts drawn up by undertaking A, whose registered office is located at ………………………….. (specify address), which constitutes both the largest and the smallest group of which undertaking F forms part as a subsidiary. The consolidated accounts drawn up by undertaking A can be obtained on the company’s website (www.address-URL-undertaking-A.com/stakeholders-relations).”

“Undertaking F is included in the consolidated accounts drawn up by undertaking A, whose registered office is located at …………………. (specify address) which constitutes the largest group of which undertaking F forms part as a subsidiary. The consolidated accounts drawn up by undertaking A are not publicly available, [applicable law does not provide for a general obligation to publish] / [the said consolidated accounts being drawn up exclusively for contractual purposes] (select as appropriate).

Undertaking F is also included in the consolidated accounts drawn up by undertaking C, whose registered office is located at ……………………. (specify address), constituting the smallest group of which undertaking F forms part as a subsidiary undertaking. The consolidated accounts drawn up by undertaking C are available to the public at the company’s registered office. A copy of all or part of these consolidated accounts may be obtained free of charge on written request sent by post to the registered office of undertaking F.”

Partial exemption for “small undertakings” (Art. 35 LRCS)

Pursuant to Article 66 LRCS, small undertakings referred to in Article 35 LRCS are authorised to draw up abridged notes to the accounts without the disclosure required by Article 65 (1) 15° a) LRCS.

As a result, small undertakings have the option of omitting the name of the undertaking drawing up the consolidated accounts of the largest group of undertakings to which the undertaking belongs as a subsidiary undertaking.

Taking examples 1, 2 and 3 above and assuming that undertaking F is a small undertaking within the meaning of Article 35 LRCS:

While the information to be provided pursuant to Article 65 (1) 15° LRCS is required for all subsidiary undertakings included in the consolidated accounts drawn up by a parent undertaking (subject to the arrangements provided for small undertakings referred to in Article 35 LRCS), subsidiary undertakings which are also parent undertakings and which wish to avail themselves of one of the so-called “sub-group” exemptions as provided for in Articles 314, 315 and 316 LSC are required to make an additional statement in the notes to their annual accounts. This is the disclosure required by Article 314 (2) c) LSC, which states that:

” c) the notes to the annual accounts of the exempted company must include:

aa) the name and registered office of the undertaking drawing up the consolidated accounts referred to in point (a);

bb) a reference to the exemption from the obligation to draw up consolidated accounts and a consolidated management report.”

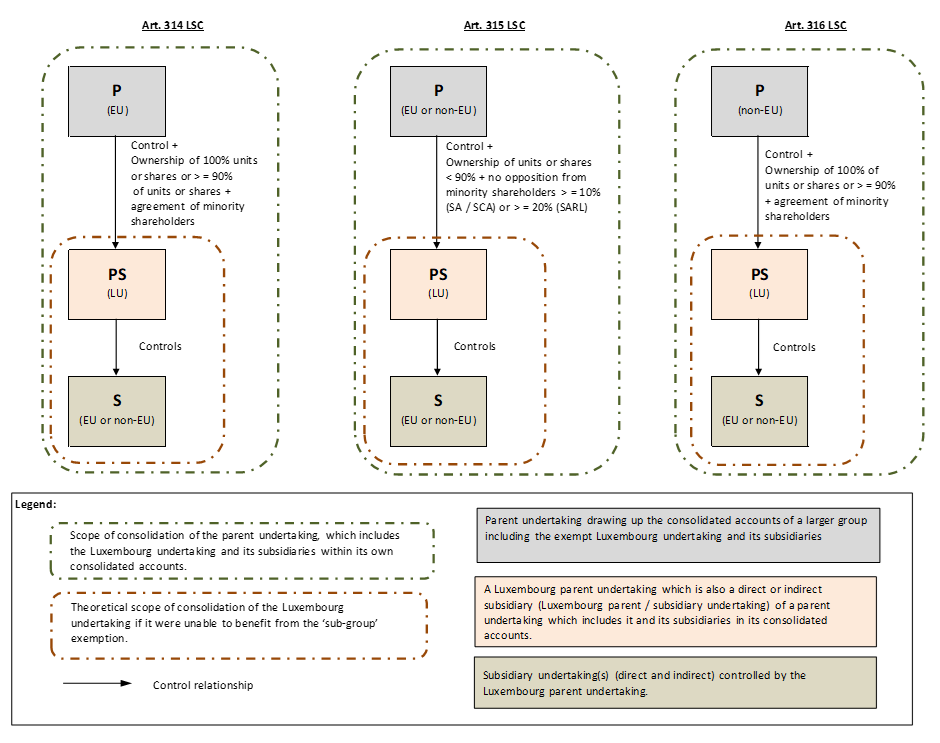

Brief reminder of the so-called “sub-group” exemptions (Art. 314, 315 and 316 LSC)

The following is a brief reminder of the so-called “sub-group” exemptions intended to facilitate understanding of the scope of the disclosure in the notes to the annual accounts required by Article 314 (2) c) LSC. This brief reminder can in no way replace an exhaustive reading of Articles 314, 315 and 316 LSC, which are subject to precise conditions in terms of both form and substance.

The so-called “sub-group” exemptions apply to Luxembourg parent undertakings which are at the same time subsidiary undertakings (hereafter “parent / subsidiary undertakings”) and which are included – themselves and their direct and indirect subsidiaries – in the consolidated accounts (or in financial statements drawn up in lieu of consolidated accounts in application of the “investment entity” exception provided for by the IFRS-EU regime3) of a larger group of undertakings drawn up by a parent undertaking which has direct or indirect control over them.

Subject to compliance with the conditions referred to, articles 314, 315 and 316 LSC have the effect of exempting the Luxembourg parent / subsidiary undertaking from the obligation to draw up and publish consolidated accounts by substituting for the said consolidated accounts those drawn up by a parent undertaking located upstream of the structure. In order to validly discharge the parent / subsidiary undertaking, the said consolidated accounts must be filed with the Luxembourg parent / subsidiary undertaking’s RCS file instead of the consolidated accounts that the latter would have had to draw up and publish if it had not been able to take advantage of the so-called “sub-group” exemption.

Articles 314, 315 and 316 LSC cover three distinct situations:

Purpose of the disclosure in the notes to the annual accounts (Art. 314 (2) c) LSC)

The disclosure required by Article 314 (2) c) LSC – which applies to the situations described in application of Articles 314, 315 and 316 LSC – is intended to provide the public with information as to the exemption from consolidation claimed by the Luxembourg parent / subsidiary undertaking and the identity of the parent undertaking drawing up the consolidated accounts, the filing of which with the RCS constitutes discharge for the exempt undertaking.

Illustrative examples of notes to the accounts4

For illustrative purposes, the following are examples of notes to the annual accounts drawn up in accordance with articles 314, 315 and 316 LSC.

The undertaking claims the so-called “EU sub-group exemption” (Art. 314 LSC)

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

On the basis of the criteria set out in article 314 of section XVI of the amended law of 10 August 1915, the company is exempt from the obligation to draw up and publish consolidated accounts and a consolidated management report for the financial year ending at …………………….. (the closing date of the current financial year). The undertaking and its subsidiaries are included in the consolidated accounts of the company ………………….. (identity of the consolidating parent undertaking) whose registered office is located at …………………. (registered office of the consolidating parent undertaking)“.

It should be noted that in order to validly rely on the exemption provided for in article 314 LSC, the undertaking must file the consolidated accounts of the consolidating parent company with the Trade and companies register (RCS).

In addition, where the consolidating parent undertaking holds 90% or more of the shares in the exempted company, the other shareholders or members of that company must have approved the exemption.

The undertaking claims an exemption known as the “EU sub-group exemption” (Art. 315 LSC)

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

On the basis of the criteria set out in article 315 of section XVI of the amended law of 10 August 1915, the company is exempt from the obligation to draw up and publish consolidated accounts and a consolidated management report for the financial year ending on …………………. (current year-end). The undertaking and its subsidiaries are included in the consolidated accounts of the company ………………….. (identity of the consolidating parent undertaking) whose registered office is located at …………………. (registered office of the consolidating parent undertaking)“.

It should be noted that in order to validly rely on the exemption provided for in article 315 of the LSC, the undertaking must, in particular, file the consolidated accounts of the consolidating parent company with the Trade and companies register (RCS).

In addition, in order to benefit from the exemption, the undertaking must ensure that the shareholders or members of the exempt undertaking who hold at least 10% of the subscribed capital if the undertaking is a SA or SCA and at least 20% if the undertaking is a SARL have not requested the preparation of consolidated accounts at least six months before the end of the financial year.

The undertaking claims the so-called “non-EU sub-group exemption” (Art. 316 LSC)

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

On the basis of the criteria set out in article 316 of section XVI of the amended law of 10 August 1915, the company is exempt from the obligation to draw up and publish consolidated accounts and a consolidated management report for the financial year ending on ……………………. (the closing date of the current financial year). The undertaking and its subsidiaries are included in the consolidated accounts of the company ………………….. (identity of the consolidating parent undertaking) whose registered office is located at …………………. (registered office of the consolidating parent undertaking)“.

It should be noted that in order to validly rely on the exemption provided for in Article 316 LSC, the undertaking must, in particular, ensure that the consolidated accounts of the consolidating parent are drawn up in accordance with the provisions of Directive 2013/34/EU or in an equivalent manner5 and file said consolidated accounts with the Trade and companies register (RCS).

In addition, in order to benefit from the exemption, the undertaking must ensure that the shareholders or members of the exempt undertaking who hold at least 10% of the subscribed capital if the undertaking is a SA or SCA and at least 20% if the undertaking is a SARL have not requested the preparation of consolidated accounts at least six months before the end of the financial year.

If Title II LRCS and Section XVI LSC explicitly require that:

and that

it should be noted that neither Title II LRCS nor Section XVI LSC explicitly require parent undertakings to provide information in the notes to their annual accounts in the following cases:

In this respect, the accounting practice of Luxembourg undertakings seems to have usefully filled the silence of the law by generally including in the notes to the annual accounts of parent undertakings not exempt under articles 314, 315 or 316 LSC information relating to the preparation or non-preparation of consolidated accounts by the latter.

Purpose of the disclosure in the notes to the annual accounts

In addition to ensuring that the annual accounts comply with strictly formal requirements, the disclosure in the notes to the annual accounts of the undertaking’s position with regard to its consolidation obligations helps to ensure that third parties and other external users are properly informed, by enabling the annual accounts to be clearly identified and the undertaking’s position and assumptions as regards consolidation to be easily understood.

Illustrative examples of notes to the accounts6

For illustrative purposes, examples of notes to the financial statements are provided below.

The parent undertaking prepares consolidated accounts for statutory purposes

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

Pursuant to section XVI of the amended law of 10 August 1915, the company also prepares consolidated accounts, which are filed with the Trade and companies register (RCS) and published in the manner prescribed by law.”

The parent undertaking claims the “small and medium-sized group” consolidation exemption (art. 313 LSC)

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

On the basis of the criteria set out in article 313 of section XVI of the amended law of 10 August 1915, the company is exempt from the obligation to draw up and publish consolidated accounts and a consolidated management report for the financial year ending …………………….. (the closing date of the current financial year).”

The parent undertaking claims the “venture capital / private equity” exclusions from the scope of consolidation referred to in Article 317 (3) c) LSC

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

Pursuant to article 317 (3) c) of the amended law of 10 August 1915 and CNC opinion 09/0027 (formerly CNC opinion 2-1 of 18 December 2009) known as the “private equity / venture capital opinion”, the company is an investment company in risk capital whose shares or units in subsidiary undertakings are held exclusively with a view to their subsequent sale. Consequently, the company does not prepare or publish consolidated accounts. In accordance with the terms of CNC opinion 09/002, the fair value of the shares or units held with a view to their disposal [is presented in the company’s balance sheet] / [is disclosed in the notes to the company’s annual accounts] (select as appropriate).”

The parent undertaking claims the exception to consolidation provided for in IFRS 10 § 31 for undertakings subject by law to Regulation 1606/2002/EC (IAS Regulation 2002) or exercising the voluntary option (art. 341bis LSC) for the IFRS – EU regime

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

In application of the exception to consolidation referred to in IFRS 10 § 31, the undertaking – which meets the definition of an “investment entity” within the meaning of IFRS 10 § 27 and which applies the IFRS – EU regime – does not consolidate its subsidiaries but measures and presents them at fair value through profit or loss in accordance with IFRS 9. In conformity with the Accounting Standards Board’s interpretative guidance Q&A CNC 15/0058, the said financial statements prepared in accordance with IFRS 10 (IFRS – EU regime) are filed with the Trade and companies register (RCS) for publication in place and stead of consolidated accounts prepared in accordance with the Accounting Directive 2013/34/EU”.

The parent undertaking owns only subsidiary undertakings which are not material both individually and collectively (art. 318(a) LSC) and is therefore exempt from the obligation to prepare and publish consolidated accounts

“In accordance with the legal requirements of Title II of the amended law of 19 December 2002, these annual accounts have been prepared on a non-consolidated basis for approval by the general meeting of [shareholders/unitholders/members] (select as appropriate).

Pursuant to article 318 point a) of section XVI of the amended law of 10 August 1915, the parent undertaking only holds subsidiary undertakings which are not material, both individually and collectively. Consequently, the company is exempt from the obligation to draw up and publish consolidated accounts and a consolidated management report for the financial year ending on ……………………. (the closing date of the current financial year).

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Notes to the annual accounts of parent and subsidiary undertakings: information relating to the consolidated accounts”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible under general law for any decision taken on the basis of this document.

1 Draft bill of law on the preparation of consolidated accounts – No. 3154, 1987 – 1988 ordinary session, comments on the articles, p. 62.

2 The wording of the notes included in the annual accounts is the responsibility of the undertaking’s administrative or management body, which determines them at its own discretion within the limits provided for by Luxembourg accounting laws and in accordance with that legislation.

3 Cf.: Q&A CNC 15/006 Subsidiaries of investment entities (IFRS 10 § 27) and continuation of consolidation exemptions of sub-groups (art. 314, 315 and 316 LSC)

4 The wording of the notes included in the annual accounts is the responsibility of the undertaking’s administrative or management body, which determines them at its own discretion within the limits provided for by Luxembourg accounting law and in accordance with that legislation.

5 For the concept of compliance and equivalence within the meaning of article 316 LSC, please refer to Q&A CNC 15/004 entitled “Exemption from the obligation to draw up consolidated accounts of sub-groups: concept of conformity and equivalence (Art. 1711-7 point 2° LSC)”.

6 The wording of the notes included in the annual accounts is the responsibility of the undertaking’s administrative or management body, which determines them at its own discretion within the limits provided for by Luxembourg accounting law and in accordance with that legislation.

7 CNC Opinion 09/002 (formerly CNC Opinion 2-1 of 18 December 2009) interpreting Article 317 (3) c) LSC in the specific case of investment companies in risk capital (venture capital / private equity)

8 Q&A CNC 15/005 Investment entities: compatibility of the exception from consolidation (IFRS 10 § 31) with the consolidation obligation (section XVI LSC)