UNOFFICIAL TRANSLATION

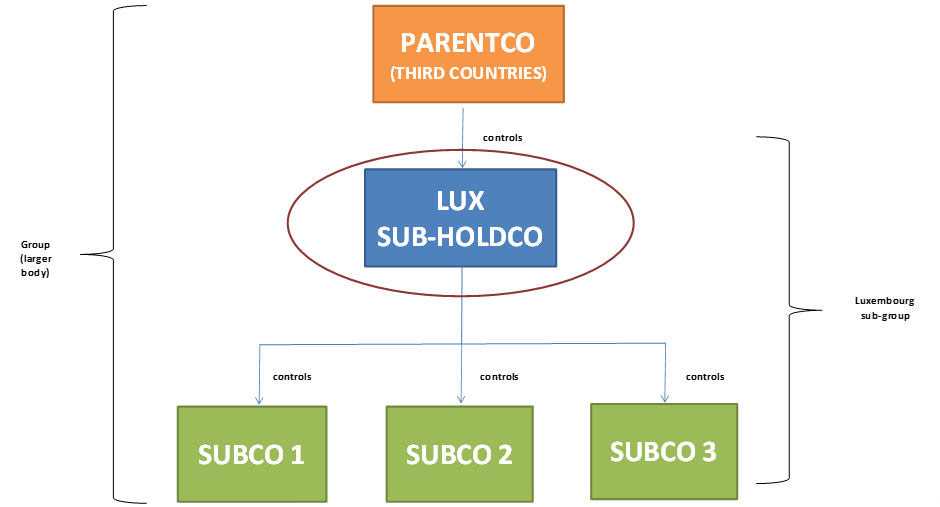

In order to benefit from the exemption from the obligation to draw up consolidated accounts provided for in article 1711-7 LSC, Luxembourg sub-groups that are consolidated within a larger group of undertakings must ensure – among other things – that the consolidated accounts and the consolidated management report of the larger group are drawn up in accordance with Title XVII LSC or in an equivalent manner.

This raises the question of how to interpret the concepts of “conformity” and “equivalence“.

Pursuant to article 1711-7, point 2° LSC and in order to benefit from the consolidation exemption of the Luxembourg sub-group, the consolidated accounts and the consolidated management report of the larger group of undertakings must be drawn up:

1. in accordance with Title XVII LSC (“conformity”);

2. or in an equivalent manner.

Without prejudice to the other cumulative conditions laid down in Article 1711-7 LSC as well as to other legal provisions (e.g. translation of the document) which the undertaking must satisfy in order to validly take advantage of the exemption, the concepts of “conformity” and “equivalence” within the meaning of Article 1711-7, point 2° LSC are examined below.

The consolidated accounts and the consolidated management report are prepared in accordance with Title XVII LSC when they have been prepared in accordance with one of the three regimes provided for under Luxembourg accounting law (DCL)1, namely:

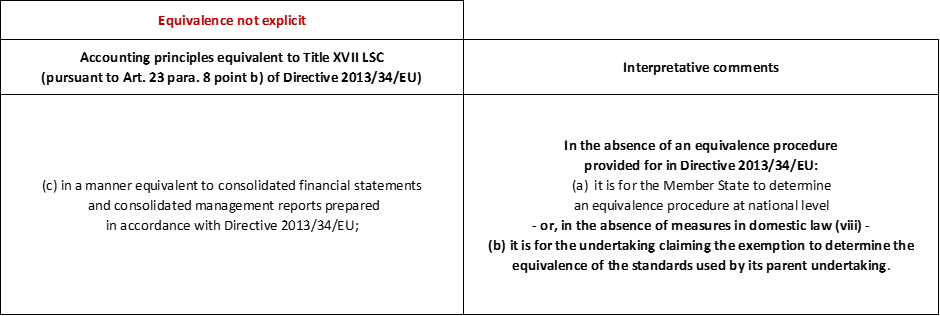

The consolidated accounts and the consolidated management report shall be drawn up in an equivalent manner to Title XVII LSC in the scenarios referred to in Article 23(8)(b) of the Accounting Directive 2013/34/EU, namely according to one of the assumptions referred to below:

In the absence of an explicit equivalence decision, it is up to the undertaking governed by Luxembourg law to determine the equivalence of the accounting principles used to draw up the consolidated accounts of the larger body within which it is included.

For information purposes, it should be noted that accounting standards resulting from national endorsement of IFRS can generally be considered equivalent within the meaning of Article 1711-7 LSC. By way of illustration, countries such as Australia (AASB standards), Hong Kong (HKFRS standards) and Turkey (TFRS standards)2 have adopted IFRS on a national basis. The same applies to the United Kingdom, which – since leaving the European Union – has endorsed IFRS via the UKEB at national level (United Kingdom Endorsement Board). However, as the national versions of IFRS are not applicable to all companies in these jurisdictions, it is the responsibility of the administrative or management body of the Luxembourg undertaking to ensure that the parent company’s consolidated accounts have been prepared in accordance with IFRS as adopted locally.

On the basis of the foregoing analysis, it must be concluded that the consolidated accounts of a larger body of undertakings which includes a Luxembourg parent undertaking and its subsidiary undertakings are:

The administrative or management bodies of undertakings remain responsible under general law for any decision taken on the basis of this document.

(i) International Financial Reporting Standards as published by the IASB (IFRS – IASB) are considered equivalent (European Commission decision no. 2008/961/EC of 12 December 2008).

(ii) Generally Accepted Accounting Principles in the United States of America (US GAAP) are considered to be equivalent. (European Commission decision no. 2008/961/EC of 12 December 2008).

(iii) Japanese Generally Accepted Accounting Principles (JP GAAP) are considered to be equivalent.(European Commission decision no. 2008/961/EC of 12 December 2008).

(iv) the Generally Accepted Accounting Principles of the People’s Republic of China (CH GAAP) are considered equivalent (European Commission implementing decision no. 2012/194/EU of 11 April 2012).

(v) Canadian generally accepted accounting principles (CA GAAP) are considered equivalent (European Commission implementing decision no. 2012/194/EU of 11 April 2012).

(vi) the Generally Accepted Accounting Principles of the Republic of Korea (KS GAAP) are considered equivalent (European Commission implementing decision no. 2012/194/EU of 11 April 2012).

(vii) the Generally Accepted Accounting Principles of the Republic of India (IN GAAP) are considered equivalent for financial years starting before 1 January 2015 (European Commission implementing decision no. 2012/194/EU of 11 April 2012).

(viii) in Luxembourg, it is up to – in the absence of national provisions determining the equivalence of foreign accounting principles – the undertaking claiming the exemption to determine the equivalence of the accounting standards used by its parent undertaking.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Exemption d’établissement des comptes consolidés de sous-groupes : notions de conformité et d’équivalence (Art. 1711-7, point 2° LSC)”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible under general law for any decision taken on the basis of this document.

1 See: Q&A CNC 14/001 “Luxembourg accounting law applicable to undertakings: three distincts regimes”.

2 For a brief overview of the accounting framework applicable in a given country, stakeholders are invited to refer – for information purposes – to the section entitled “Use of IFRS Accounting Standards by Jurisdiction” available on the IFRS Foundation website at the following URL address:

https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/#use-of-ifrs-accounting-standards-by-jurisdiction