UNOFFICIAL TRANSLATION

Luxembourg accounting law (DCL) applicable to undertakings has been amended several times in recent years1. Following these reforms, what is the current structure of Luxembourg accounting law?

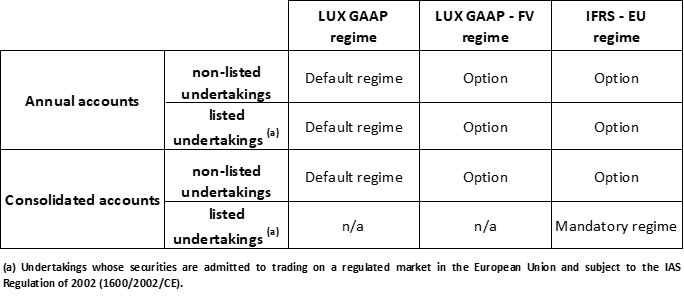

As the law currently stands, Luxembourg accounting law (DCL) applicable to undertakings2 refers broadly to three distinct regimes:

These are the provisions of Chapter II “Preparation of the annual accounts” of Title II of the LRCS3 with use of the valuation rules of Section 7, in particular the principles of prudence (art. 51 (1) c) LRCS) and measurement at historical cost (art. 52 LRCS).

This is the LUX GAAP regime (Cf. point 1.) to which are added the optional provisions set out in section 7bis “Fair value measurement rules” allowing measurement by reference to fair value instead of historical cost. These “LUX GAAP with fair value option” (LUX GAAP – FV) are the result of the convergence process of the accounting directives towards IFRS and are known to practitioners under various names such as “mixed LUX GAAP”, “LUX GAAP with IFRS option”, “LUX GAAP plus”, etc.

This is the optional regime provided for in Chapter IIbis “Preparation of annual accounts in accordance with international accounting standards” of Title II of LRCS, which allows Luxembourg undertakings, pursuant to article 72bis LRCS and article 341bis LSC4, to prepare their annual accounts and/or consolidated accounts in accordance with IFRS – EU.

In view of the above, the CNC’s Q&As will generally refer to these three distinct regimes under Luxembourg accounting law, with the result that the answers may differ significantly from one regime to another.

Disclaimer

This document – provided as a courtesy – is an unofficial translation of the French original document entitled “Droit comptable luxembourgeois des entreprises: trois régimes distincts”. In case of discrepancy in interpretation, the French version shall prevail.

The “questions and answers” published by the “Commission des normes comptables (CNC)” (Accounting Standards Board):

The administrative or management bodies of undertakings remain responsible under general law for any decision taken on the basis of this document.

1 See in particular:

– Law of 10 December 2010 on the introduction of international accounting standards for undertakings (parliamentary document 5976);

– Law of 30 July 2013 reforming the Accounting Standards Board and amending various provisions relating to the bookkeeping and annual accounts of undertakings and the consolidated accounts of certain types of undertakings (parliamentary document 6376).

2 This note refers to accounting law applicable to undertakings, i.e. general accounting law or ordinary accounting law as opposed to sector-specific accounting laws or special accounting laws which are not covered here (e.g. bank accounting law, insurance sector accounting law, etc.).

3 LRCS: Amended law of 19 December 2002 on the Trade and companies register and the bookkeeping and annual accounts of undertakings

4 LSC: Law of 10 August 1915 on commercial companies, as amended